Assessing Ultragenyx Pharmaceutical (RARE) Valuation After UX111 FDA Review Acceptance And Growing GTX-102 Optimism

Ultragenyx Pharmaceutical, Inc. RARE | 0.00 |

Ultragenyx Pharmaceutical (RARE) is back in focus after the FDA accepted its resubmitted BLA for UX111, assigning a September 19, 2026 PDUFA date, alongside growing institutional interest in the GTX-102 program.

Even with the fresh regulatory progress on UX111 and growing attention on GTX-102, the stock’s momentum has been weak, with the share price down 17.34% over the past 30 days and the 1-year total shareholder return declining 41.71%.

If this kind of event driven biotech story interests you, it can be useful to compare it with other specialist healthcare opportunities using our screener for 39 healthcare AI stocks

So with Ultragenyx trading well below the latest US$52.05 fair value estimate and sentiment split around GTX-102 and UX111, is this a mispriced rare disease specialist, or is the market already reflecting the road ahead?

Most Popular Narrative: 58.5% Undervalued

Ultragenyx's most followed narrative puts fair value at about $52.05 per share, well above the last close at $21.59, and leans heavily on future gene therapy progress to justify that gap.

Ultragenyx's clinical pipeline is advancing with five Phase III programs (including UX143 and GTX-102), multiple BLA submissions expected in the coming quarters, and near-term Phase III data readouts (notably for UX143 in OI by year-end and GTX-102 in Angelman syndrome in 2026) serving as upcoming value inflection points that can diversify and significantly accelerate the company's revenue base.

Want to see how a loss making rare disease specialist ends up with a much higher fair value than its current price? The narrative leans on rapid top line expansion, a sharp swing in profitability and a rich future earnings multiple to bridge that gap. Curious which assumptions matter most to that $52.05 figure and how sensitive it is to setbacks or outperformance?

Result: Fair Value of $52.05 (UNDERVALUED)

However, that upside story still leans heavily on successful UX111 and DTX401 approvals, as well as on Ultragenyx containing losses and cash burn, which remain key pressure points.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View: Market Ratios Tell a Different Story

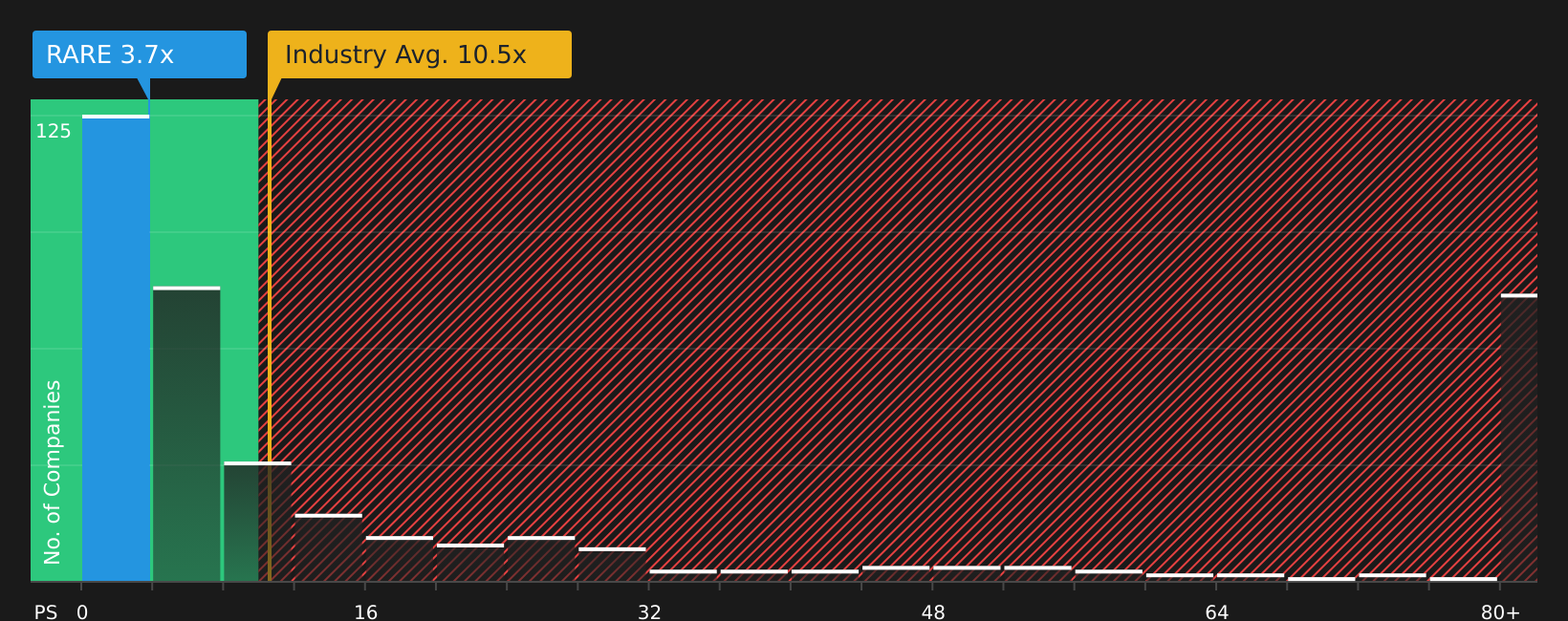

The narrative model flags Ultragenyx as heavily undervalued, yet the current P/S of 3.2x screens as expensive versus a fair ratio of 2.1x, even if it still sits well below biotech peers at 10.1x and 23.9x. Is this a margin of safety or a value trap in the making?

Next Steps

If this mix of optimism around approvals and concern over execution feels familiar, do not wait on others to decide the story for you. Instead, carefully weigh both 2 key rewards and 3 important warning signs

Looking for more investment ideas?

If Ultragenyx has caught your attention, do not stop there, broaden your watchlist with stocks that match different goals, from income to resilience and growth potential.

- Target steady income by reviewing companies in the 10 dividend fortresses that focus on higher yields with an emphasis on durability.

- Hunt for value by scanning the screener containing 21 high quality undiscovered gems where lesser known stocks with solid fundamentals might be flying under the radar.

- Prioritise resilience by checking out the 62 resilient stocks with low risk scores that highlights businesses with lower risk scores for a calmer portfolio foundation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.