Assessing uniQure (QURE) Valuation After New Securities Fraud Lawsuit On AMT-130 Disclosures

uniQure N.V. QURE | 17.42 | +1.93% |

Why the new lawsuit matters for uniQure stock

A fresh securities fraud class action against uniQure (NasdaqGS:QURE) is putting a spotlight on how the company previously described AMT-130’s pivotal Huntington’s disease data and its interactions with the FDA.

The complaint challenges earlier messaging around biomarker results, comparisons with the ENROLL HD dataset, and the timeline for a potential Biologics License Application, which together influence how investors assess uniQure’s regulatory and commercial path.

The new lawsuit comes after a busy few days for uniQure, which also shared fresh AMT-191 data and presented at the WORLDSymposium. Over the same period, the share price has declined, with a 5.14% 1-day and 11.12% 7-day share price return. The 1-year total shareholder return of 87.77% contrasts with a weaker 3-year total shareholder return of 20.07% and a 5-year total shareholder return of a 32.50% loss, indicating that long-term holders have experienced a mixed journey as recent momentum has faded.

If legal risk around AMT-130 has you reassessing gene therapy exposure, it could be worth widening your watchlist, using 27 healthcare AI stocks as a starting point for new ideas.

With uniQure trading at US$24.71 and sitting at a very large discount to the consensus price target, yet carrying fresh legal and clinical uncertainties, is the stock being overly punished, or is the market already pricing in potential future developments?

Most Popular Narrative: 55% Undervalued

At a last close of $24.71 versus a widely followed fair value estimate of about $54.42, the current price sits well below that narrative anchor and puts a lot of weight on how you view uniQure’s Huntington’s and broader gene therapy pipeline.

The potential accelerated approval for AMT-130 in treating Huntington's disease could significantly boost future revenues as it would be one of the first disease-modifying treatments available for this condition. Expansion of the clinical pipeline with new studies in refractory temporal lobe epilepsy, Fabry disease, and SOD1-ALS could lead to additional revenue streams if these treatments are successful and commercialized.

Want to see what kind of revenue curve and profit profile would need to sit behind a fair value more than double today’s price? The most followed narrative leans on rapid top line expansion, a marked shift in margins, and a future earnings multiple more often associated with mature industry leaders rather than loss making developers. Curious which specific assumptions have to line up for that story to hold?

Result: Fair Value of $54.42 (UNDERVALUED)

However, that story depends heavily on AMT-130’s regulatory outcome, as well as resolving revenue and manufacturing uncertainties that, if they break the wrong way, could quickly reset expectations.

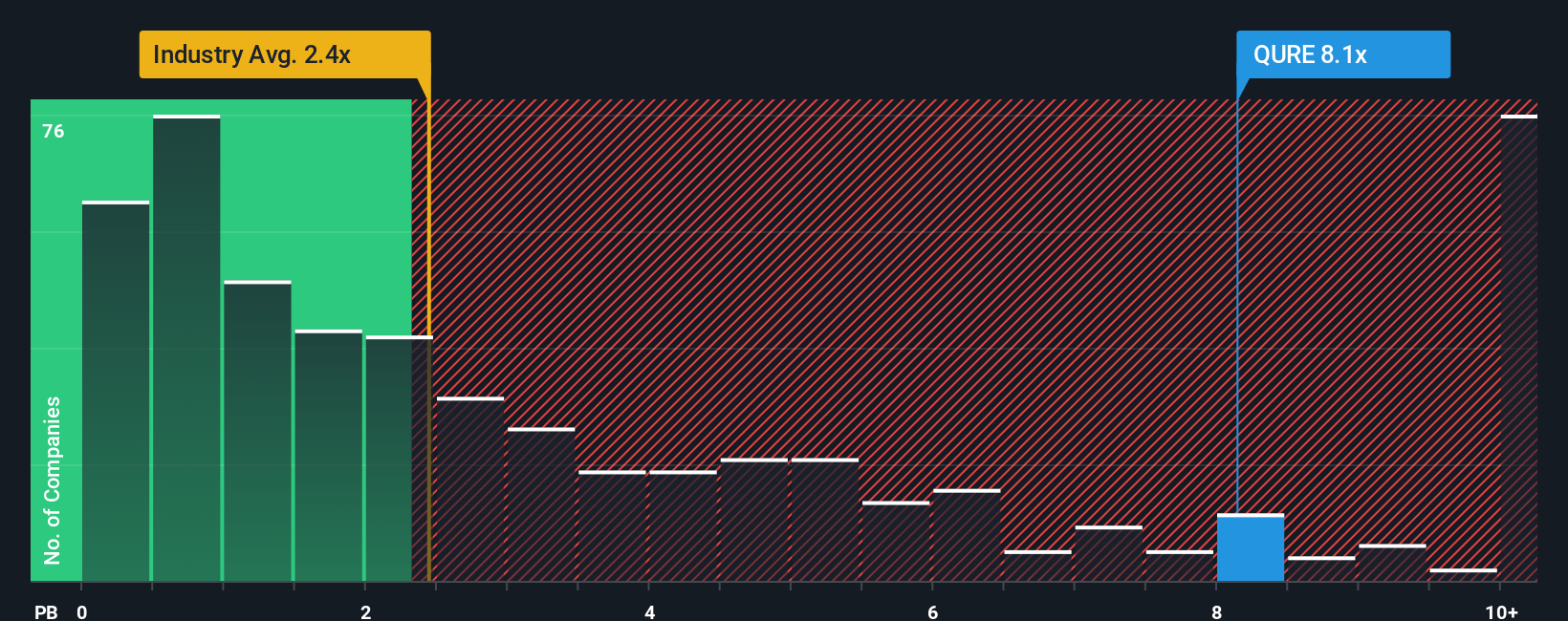

Another View: What the P/B Ratio Is Saying

The fair value narrative leans heavily on future earnings, but today the market is also signaling something through the P/B ratio. uniQure trades at about 6.7x book value versus 2.8x for the wider US biotech group and roughly 12.8x across closer peers.

That gap suggests investors are paying more than the sector average for each dollar of net assets, yet less than the peer set, which can cut both ways. If sentiment cools, there is room for the P/B to drift toward the industry level. If the story firms up, it could instead move closer to peers.

Build Your Own uniQure Narrative

If you are not fully aligned with this view or prefer to work through the numbers yourself, you can build a tailored thesis in just a few minutes, starting with Do it your way.

A great starting point for your uniQure research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If this story has sharpened your focus, do not stop here. The next idea on your radar could be identified before the market pays closer attention.

- Target reliable income by reviewing 14 dividend fortresses to help anchor your portfolio with higher yielding names.

- Hunt for mispriced opportunities through 51 high quality undervalued stocks that combine quality fundamentals with more modest expectations.

- Prioritise capital preservation by scanning 83 resilient stocks with low risk scores designed to highlight companies with fewer red flags.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.