Assessing Vertiv Holdings Co (VRT) Valuation As AI Data Center Demand And Analyst Optimism Build

VERTIV HOLDINGS LLC VRT | 309.92 | -0.19% |

Vertiv Holdings Co (VRT) is back in focus after strong AI driven data center demand, rising organic orders, higher R&D plans around liquid cooling, and recent earnings optimism and analyst upgrades.

The latest move to a US$195.58 share price, with a 1 day share price return of 10% and a 30 day share price return of 14.01%, sits alongside a 1 year total shareholder return of 61.36% and a very large 3 year total shareholder return. This suggests momentum has been building around Vertiv’s AI driven data center story and recent earnings optimism.

If Vertiv’s AI infrastructure surge has your attention, this could be a good moment to widen your research and check out 33 AI infrastructure stocks as potential peers riding similar data center demand.

Vertiv now trades around US$195.58, close to analyst price targets and reflecting strong AI data center enthusiasm. The real question is whether this is an overhyped story or a genuine opportunity the market has not fully priced in.

Most Popular Narrative: 1% Undervalued

Vertiv’s most followed narrative pegs fair value around $198.45, only slightly above the current $195.58 price. That framing presents the current AI data center enthusiasm as almost fully reflected, but not entirely.

Operational and supply chain challenges, including costs tied to tariff transitions and rapid scaling, are expected by management to be largely resolved by the end of 2025. This is described as supporting management's long-term operating margin targets (25% by 2029) and stronger future earnings growth as scale benefits are fully realized.

Curious what kind of revenue path and margin lift need to line up for that fair value close to $200? The narrative leans on strong earnings compounding, richer profitability, and a premium future earnings multiple. Want to see how those pieces fit together across the next few years? Read the full story and judge whether the assumptions feel realistic for you.

Result: Fair Value of $198.45 (ABOUT RIGHT)

However, you still need to weigh risks such as ongoing supply chain and EMEA execution issues, as well as the possibility of large cloud customers shifting more power and cooling in house.

Another Angle: Rich Earnings Multiple Sets a High Bar

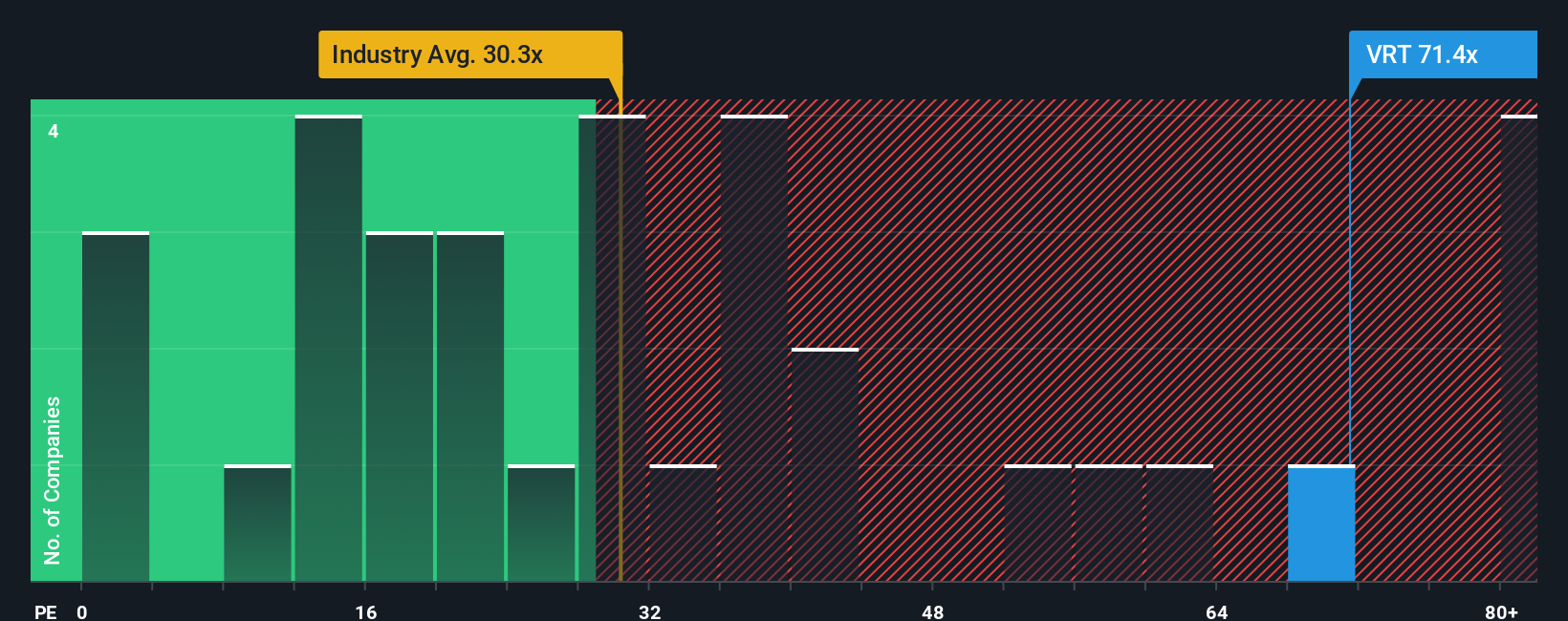

While the most followed narrative calls Vertiv roughly fairly valued around $198.45, the current P/E of 72.3x tells a different story. That is much higher than the US Electrical industry at 35.8x, the peer average at 39.3x, and even the fair ratio of 55.7x, which suggests the market could move toward a lower multiple over time. For you, the tension is simple: are you comfortable paying a premium that already bakes in a lot of good news, or do you prefer waiting for the valuation gap to narrow.

Build Your Own Vertiv Holdings Co Narrative

If you look at these assumptions and want to stress test them yourself, you can build your own view on Vertiv using our tools and Do it your way in just a few minutes.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Vertiv Holdings Co.

Ready to hunt for your next idea?

If Vertiv sparked your interest, do not stop there. Use the Simply Wall Street Screener to spot other opportunities that could suit your approach.

- Target value focused opportunities by scanning our list of 53 high quality undervalued stocks that pair quality fundamentals with prices that may look appealing.

- Prioritize resilience and sleep a little easier by reviewing 86 resilient stocks with low risk scores that score well on our risk checks.

- Get ahead of the crowd by checking our screener containing 24 high quality undiscovered gems that have strong fundamentals yet receive relatively little attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.