Assessing Voyager Technologies (VOYG) Valuation After Space Crystal Patent And ISS Experiment Plans

Voyager Technologies VOYG | 0.00 |

Voyager Technologies (VOYG) is back on investor radars after securing a patent for manufacturing high purity optical crystals in space, and it is planning an International Space Station experiment in spring 2026 to validate the process.

The patent news has arrived alongside strong near term momentum, with a 1 month share price return of 53.96% and year to date share price return of 27.36% at a last close of $35.38. This suggests investors are reacting to perceived growth potential in space based manufacturing and recent NASA program work.

If this kind of space and defense story interests you, it could be worth scanning other aerospace and defense stocks that might also be benefiting from demand tied to communications and orbital infrastructure.

With the stock up sharply in the past month and trading at a discount to an average analyst price target of US$42.17, the key question is whether Voyager is still mispriced or if the market already recognizes its future growth story.

Price-to-Sales of 13.4x: Is it justified?

Voyager Technologies currently trades on a P/S of 13.4x, which stands well above both its Aerospace & Defense peers and Simply Wall St’s estimated fair P/S level.

The P/S ratio compares the company’s market value to its revenue and is a common way to look at high growth or loss making businesses where earnings are not yet positive. For Voyager, this means investors are paying a relatively high amount for each dollar of revenue, despite the company reporting a net loss of US$100.55m on revenue of US$157.48m.

Analysts expect Voyager’s revenue to grow 40.2% per year, which is faster than both the broader US market at 10.5% and the 20% high growth marker stated in the data. Even so, the current 13.4x P/S is described as expensive compared to the US Aerospace & Defense industry average of 3.8x, the peer average of 3x, and the estimated Fair P/S Ratio of 4.6x. This 4.6x level is one the market could potentially gravitate towards over time if expectations change.

Result: Price-to-Sales of 13.4x (OVERVALUED)

However, you also have to weigh execution risk around its space manufacturing plans, as well as the ongoing net loss of US$100.55m on revenue of US$157.48m.

Another way to look at value

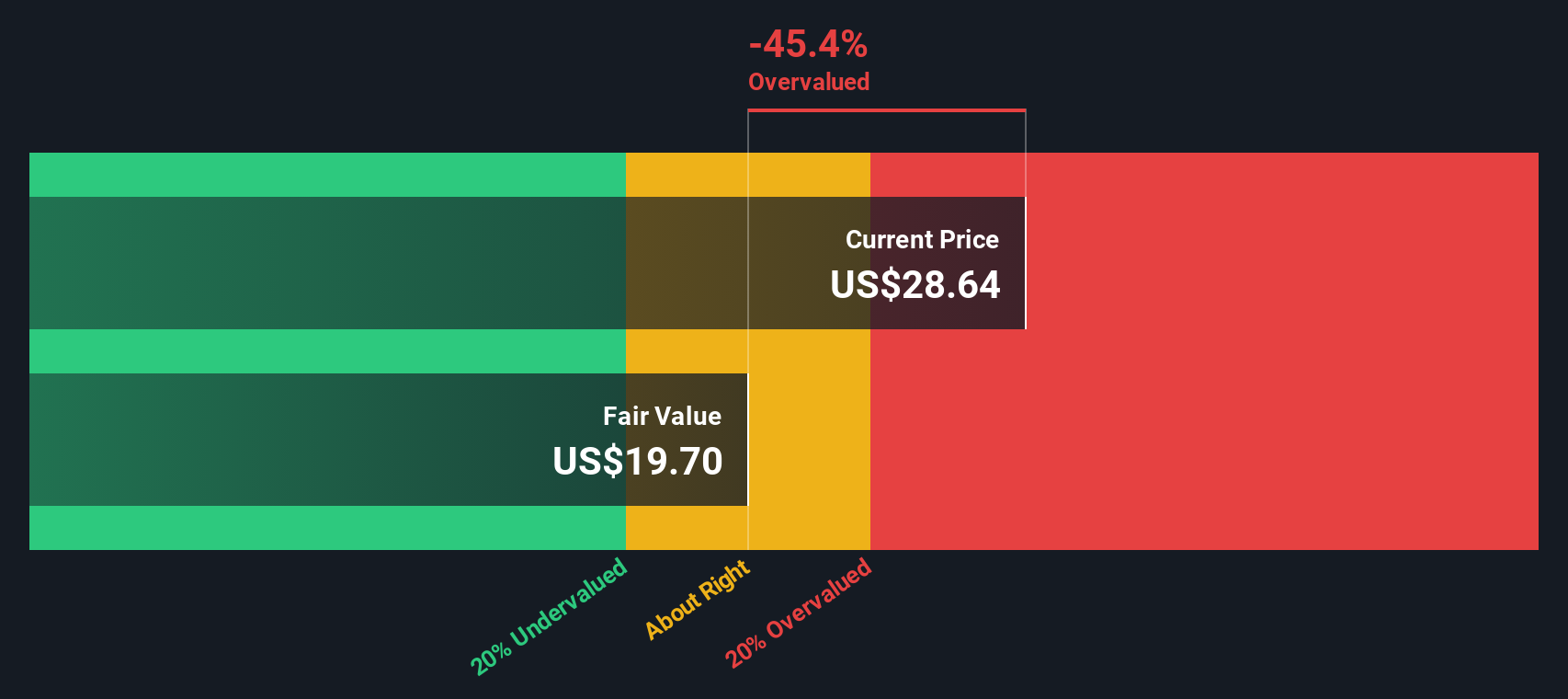

Our DCF model offers a very different perspective, with Voyager trading at a 91.9% discount to an estimated fair value of US$439.06 per share. That indicates a very large gap compared with the rich 13.4x P/S, so which signal do you think deserves more weight?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Voyager Technologies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 863 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Voyager Technologies Narrative

If you see the numbers differently or prefer to test your own assumptions, you can build a custom view in just a few minutes, starting with Do it your way.

A great starting point for your Voyager Technologies research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Voyager has grabbed your attention, do not stop here, use the Simply Wall St Screener to uncover other focused ideas that might fit your portfolio.

- Target potential value gaps by checking out these 863 undervalued stocks based on cash flows that screen for companies priced below their estimated cash flow worth.

- Back the next wave of automation and data driven tools by reviewing these 24 AI penny stocks shaping the growth of artificial intelligence across sectors.

- Add an income angle to your watchlist by filtering for these 12 dividend stocks with yields > 3% that combine higher yields with listed dividend paying histories.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.