Assessing W. P. Carey (WPC) Valuation After Dividend Recovery And Portfolio Reshaping

W. P. Carey Inc. WPC | 70.25 | +1.24% |

Dividend recovery and portfolio reshaping at W. P. Carey

W. P. Carey (WPC) is back in focus after cutting its dividend in late 2023, then raising it for eight straight quarters while cycling US$1.5b of dispositions into US$2.1b of new properties.

At a share price of US$69.25, W. P. Carey has seen a 6.77% year to date share price return and a 32.80% one year total shareholder return. This suggests that recent dividend progress and portfolio reshaping are feeding into gradually improving sentiment rather than a sudden re rating.

If W. P. Carey’s reset has you rethinking income and real estate exposure, this can be a useful moment to scan wider opportunities across aerospace and defense stocks as well.

With the dividend rebuilding, US$2.1b poured into new properties, and the share price sitting only slightly below one analyst target, the real question is whether W. P. Carey is still a mispriced opportunity or already reflecting future growth.

Most Popular Narrative: 0.8% Undervalued

The most followed narrative places W. P. Carey’s fair value at about $69.82, almost level with the last close at $69.25 and framing today’s price as finely balanced.

Sustained demand for distribution and logistics space, driven by continued e commerce expansion and supply chain investments, is fueling strong investment in industrial and warehouse assets. This is reflected in W.P. Carey's pivot to close to 100% industrial in new investments and a pipeline predominantly industrial supporting future revenue and NOI growth.

Curious what kind of revenue path and margin profile have to line up for that fair value to work, and how much profit growth is baked in? The full narrative spells out a detailed growth and earnings path you might want to benchmark against your own expectations.

Result: Fair Value of $69.82 (UNDERVALUED)

However, that picture still depends on tenant health and the continued success of recycling non core assets. Either factor could pressure rents, funding and the overall fair value story.

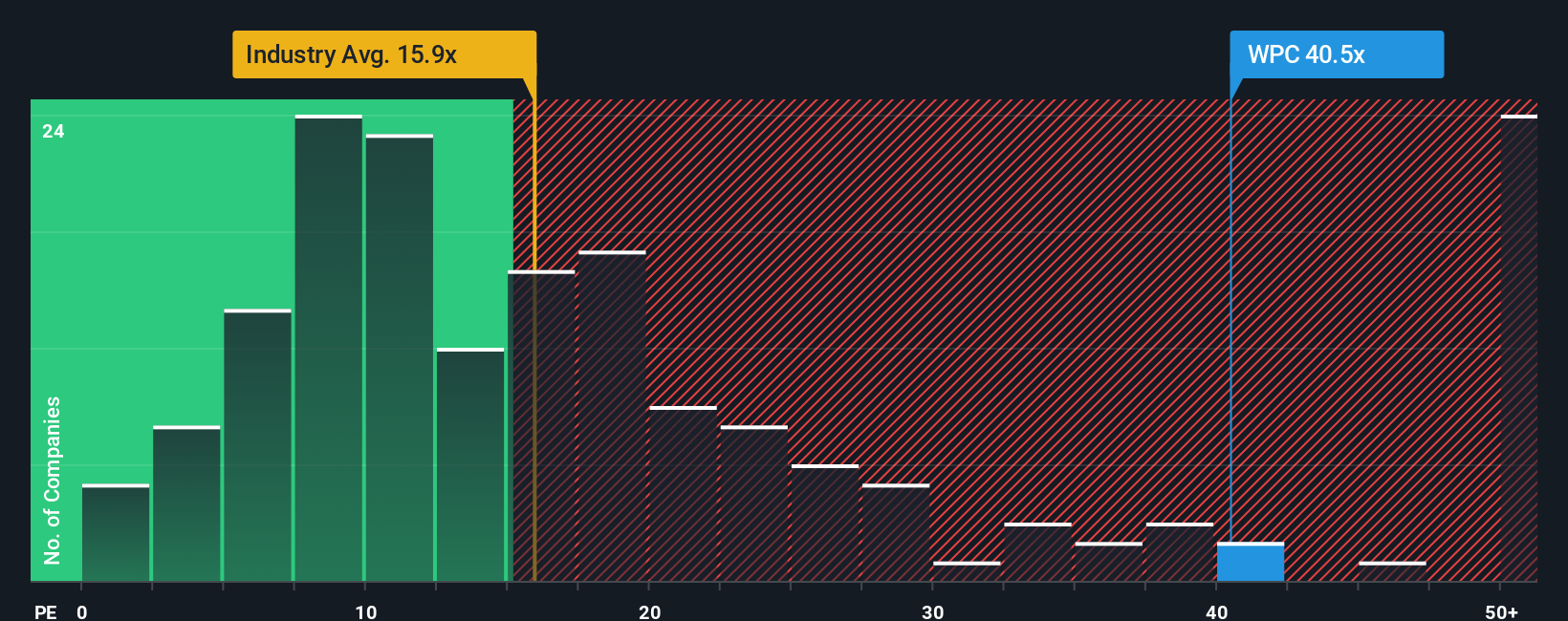

Another View: Rich P/E Signals A Different Story

While the fair value narrative points to only 0.8% undervaluation, the P/E picture is much less forgiving. W. P. Carey trades on a 41.6x P/E, compared with 15.9x for the global REIT industry, 29.4x for peers, and a fair ratio estimate of 38.8x.

That gap suggests investors are already paying up for W. P. Carey’s income profile and growth outlook, with limited room if expectations are not met. The question for you is whether that premium feels like justified confidence or valuation risk that edges past your comfort zone.

Build Your Own W. P. Carey Narrative

If you see the numbers differently and would rather weigh the data yourself, you can build your own view in just a few minutes with Do it your way.

A great starting point for your W. P. Carey research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Ready to scout more investment ideas?

If W. P. Carey has sharpened your thinking, do not stop here. Use the Simply Wall St Screener to pressure test new companies against the same standards.

- Spot potential bargains by scanning these 867 undervalued stocks based on cash flows that may offer more attractive prices based on their cash flow profiles.

- Back future focused themes by checking out these 25 AI penny stocks that are tied to artificial intelligence and related technologies.

- Boost your income focus by reviewing these 13 dividend stocks with yields > 3% that currently offer yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.