Assessing W. R. Berkley (WRB) Valuation After Recent Share Price Softness

W. R. Berkley Corporation WRB | 0.00 |

How W. R. Berkley shares have moved and what investors are watching

W. R. Berkley (WRB) has seen a mix of outcomes for investors recently, with a small 1 day decline, a slightly weaker week, a modest gain over the past month, and softer performance over the past 3 months and year.

At a last close of $66.95 and a market value of about $26.2b, the stock reflects a business with annual revenue of $14.9b and net income of $1.9b, alongside a relatively low value score of 2.

Recent price action suggests momentum has softened, with the share price trading slightly lower year to date, while the very strong 3 year and 5 year total shareholder returns highlight how longer term holders have been rewarded.

If you are comparing W. R. Berkley with other opportunities in financials and beyond, this can be a good moment to widen your lens and check out 18 top founder-led companies

With W. R. Berkley trading close to analyst targets yet showing a very large intrinsic discount estimate, the key question is whether this signals genuine undervaluation or whether the market is already pricing in future growth.

Most Popular Narrative: 2% Undervalued

The most followed narrative sees W. R. Berkley’s fair value at $68.33, only slightly above the recent $66.95 close, and links that gap to earnings resilience and disciplined underwriting.

Prudent capital management, shown by a growing investment portfolio benefitting from higher new money yields and conservative reserving, is increasing investment income and book value per share, laying a foundation for higher long-term earnings and the potential for resumed share buybacks.

Curious what justifies paying close to today’s price for only modest growth? The narrative leans heavily on margins, earnings quality, and a richer valuation multiple.

Result: Fair Value of $68.33 (UNDERVALUED)

However, this depends on pricing and loss trends staying in check, while softer commercial and reinsurance pricing or rising claims costs could quickly challenge the margin story.

Another View on Valuation

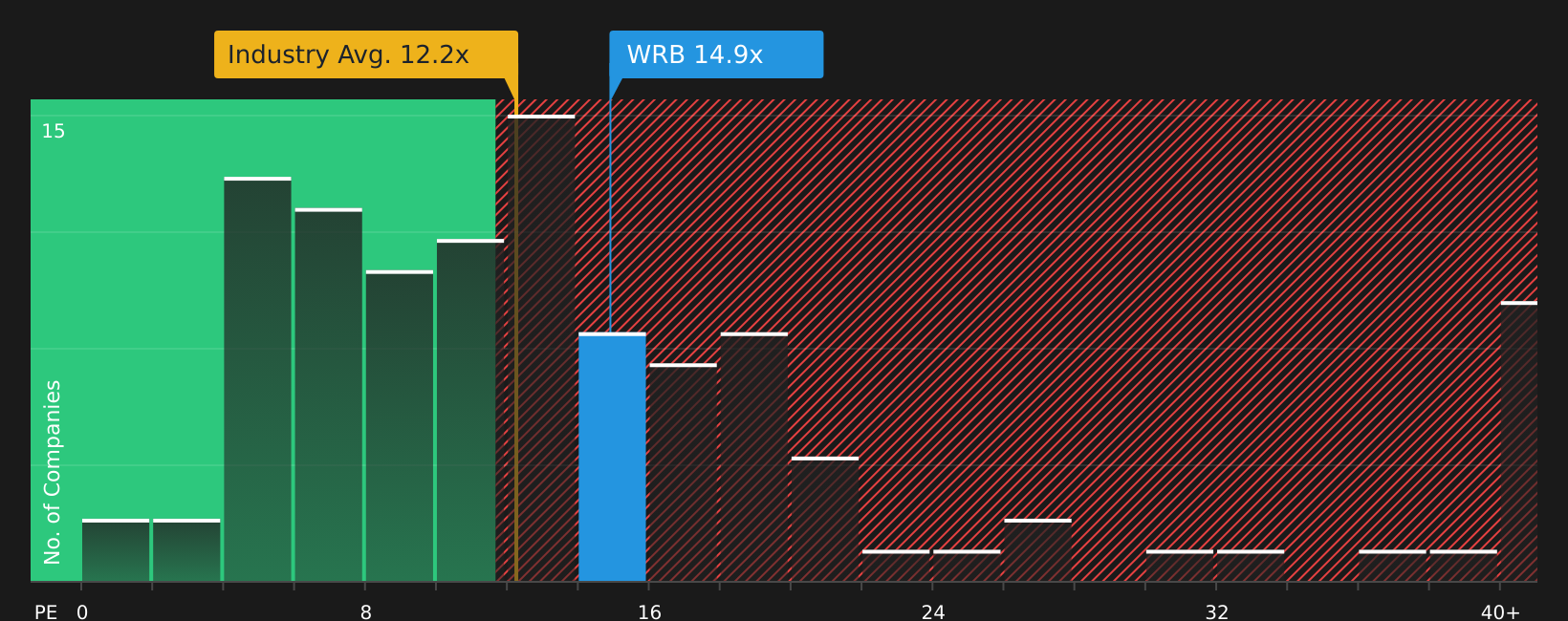

While the narrative frames W. R. Berkley as slightly undervalued, the P/E picture is less generous. The shares trade on a 13.9x P/E, compared with 11.6x for the US Insurance industry, 11.1x for peers, and a fair ratio of 11.4x. This points to some valuation risk if sentiment cools.

For readers who lean on earnings multiples rather than cash flow models, this gap raises a simple question: is the quality story strong enough to keep the P/E premium in place if growth expectations stay modest or soften further?

Next Steps

Given all of this, if you are somewhere between cautious and optimistic, it may make sense to act now and test the narrative against the numbers yourself with 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop with just one company, you risk missing other opportunities that better fit your goals, risk comfort, and income needs across different parts of your portfolio.

- Target potential value opportunities by scanning 53 high quality undervalued stocks, which combine solid fundamentals with prices that may sit below their estimated worth.

- Strengthen your passive income plans by reviewing 12 dividend fortresses, which focus on higher yielding companies with an emphasis on payout durability.

- Prioritize capital protection by checking 73 resilient stocks with low risk scores, which emphasize resilient balance sheets and lower overall risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.