Assessing Warner Music Group (WMG) Valuation As Optimistic Analyst Calls Highlight Streaming And Live Music Growth

Warner Music Group WMG | 26.11 | +1.36% |

Analyst optimism puts Warner Music Group (WMG) in focus

Recent positive views from Morgan Stanley and Wolfe Research on Warner Music Group (NasdaqGS:WMG), focused on streaming payment expectations and the music and live entertainment sectors, have drawn fresh attention to the stock.

At a share price of US$31.01, Warner Music Group has seen an 11.59% 1 month share price return, while its 1 year total shareholder return of 7.48% and 5 year total shareholder return of 1.74% suggest momentum has been modest rather than runaway as investors reassess growth potential and risks around streaming and live entertainment.

If the renewed interest in music and live events has your attention, it could be a useful time to widen your watchlist with fast growing stocks with high insider ownership.

So, with analysts upbeat, shares trading at US$31.01, and the stock sitting at roughly an 18% discount to one estimate of intrinsic value, is Warner Music Group quietly undervalued or already pricing in the next leg of growth?

Most Popular Narrative: 17.9% Undervalued

With Warner Music Group closing at US$31.01 against a narrative fair value of US$37.78, the gap reflects a detailed long term cash flow story.

Ongoing cost reduction initiatives (strategic reorganization, automation, and tech investments) are projected to unlock $300 million in annualized savings by 2027, improving operational efficiency and contributing to margin expansion of 150 to 200 basis points in fiscal 2026. Aggressive catalog acquisitions fueled by the Bain Capital joint venture provide Warner with additional revenue and market share via enhanced M&A capacity while also leveraging its existing global distribution infrastructure for higher catalog monetization, thus supporting sustained earnings growth.

Curious how moderate revenue growth assumptions support a higher earnings base and a lower future P/E than many peers? The full narrative walks through the margin rebuild, cash flow ramp and valuation math that underpin this fair value call.

Result: Fair Value of $37.78 (UNDERVALUED)

However, there are still clear pressure points, including weaker recent operating and free cash flow, as well as the execution risk around the US$1.2b Bain Capital catalog venture.

Another View: Rich Earnings Multiple Keeps Expectations High

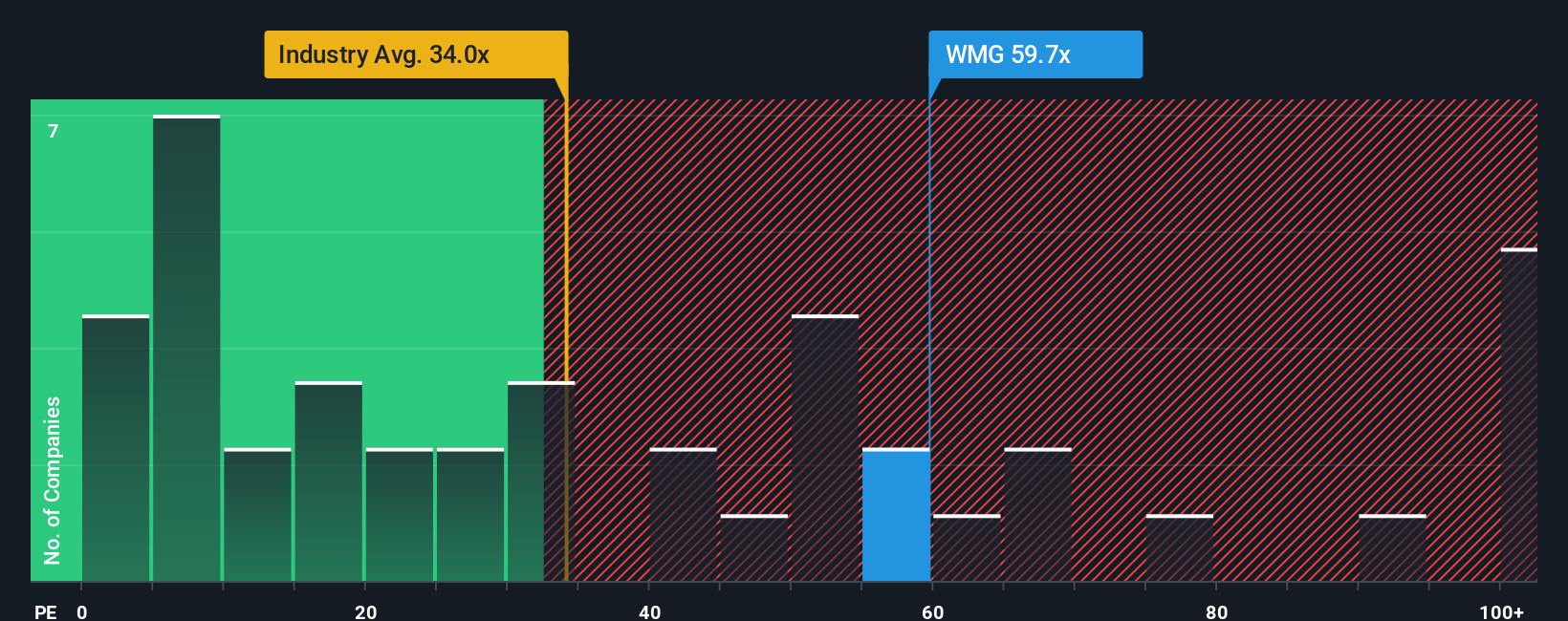

That 17.9% discount to fair value tells one story, but the P/E ratio tells another. Warner Music Group trades on a 44.9x P/E, above the US Entertainment industry at 19.4x and above a fair ratio of 29.5x, even though it is below peers at 92.8x.

Put simply, the market is already paying a premium for Warner Music Group's earnings. The gap to the 29.5x fair ratio suggests limited room for disappointment if forecasts or margins fall short. Does that premium feel justified to you, or does it tilt the balance toward valuation risk?

Build Your Own Warner Music Group Narrative

If you see the numbers differently or prefer to weigh the data on your own terms, you can build a custom view in minutes with Do it your way.

A great starting point for your Warner Music Group research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Warner Music Group has sharpened your thinking, do not stop here. The next strong idea often comes from comparing very different opportunities side by side.

- Spot potential value by scanning these 883 undervalued stocks based on cash flows that align with your return and risk expectations.

- Tap into future facing themes by reviewing these 28 AI penny stocks shaping the use of artificial intelligence across sectors.

- Add income focused names to your watchlist by assessing these 12 dividend stocks with yields > 3% that could complement a growth heavy portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.