Assessing Waste Management (WM) Valuation After Earnings Miss And Insider Stock Sales

Waste Management, Inc. WM | 224.93 | -0.95% |

Waste Management (WM) is back on investors radar after its fourth quarter 2025 earnings missed forecasts on both earnings per share and revenue, while multiple senior executives reported sizable stock sales.

The recent earnings miss and cluster of insider sales sit against a backdrop of firm share price momentum, with a 30 day share price return of 6.32% and a 5 year total shareholder return of 131.51% pointing to gains that have built over time rather than fading.

If this mix of steady returns and fresh headlines has you thinking about where else capital could work, it may be worth scanning 24 power grid technology and infrastructure stocks as another way to spot potential opportunities tied to essential infrastructure.

With WM trading at US$235.22, sitting about 7% below the average analyst price target and at a roughly 21% discount to one intrinsic value estimate, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 6.5% Undervalued

Against WM's last close at $235.22, the most followed valuation narrative points to a fair value of $251.64, implying a modest gap the market has not closed.

The analysts have a consensus price target of $257.3 for Waste Management based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $277.0, and the most bearish reporting a price target of just $198.0.

Curious what supports a fair value above today's price? This narrative is based on assumptions of steady revenue expansion, firmer margins, and a richer earnings multiple than the sector. The exact mix of growth, profitability, and discount rate assumptions is where the story gets interesting.

Result: Fair Value of $251.64 (UNDERVALUED)

However, those assumptions could be knocked off course if the Stericycle integration falls short of the expected synergies or if regulatory shifts push up recycling and renewable energy costs.

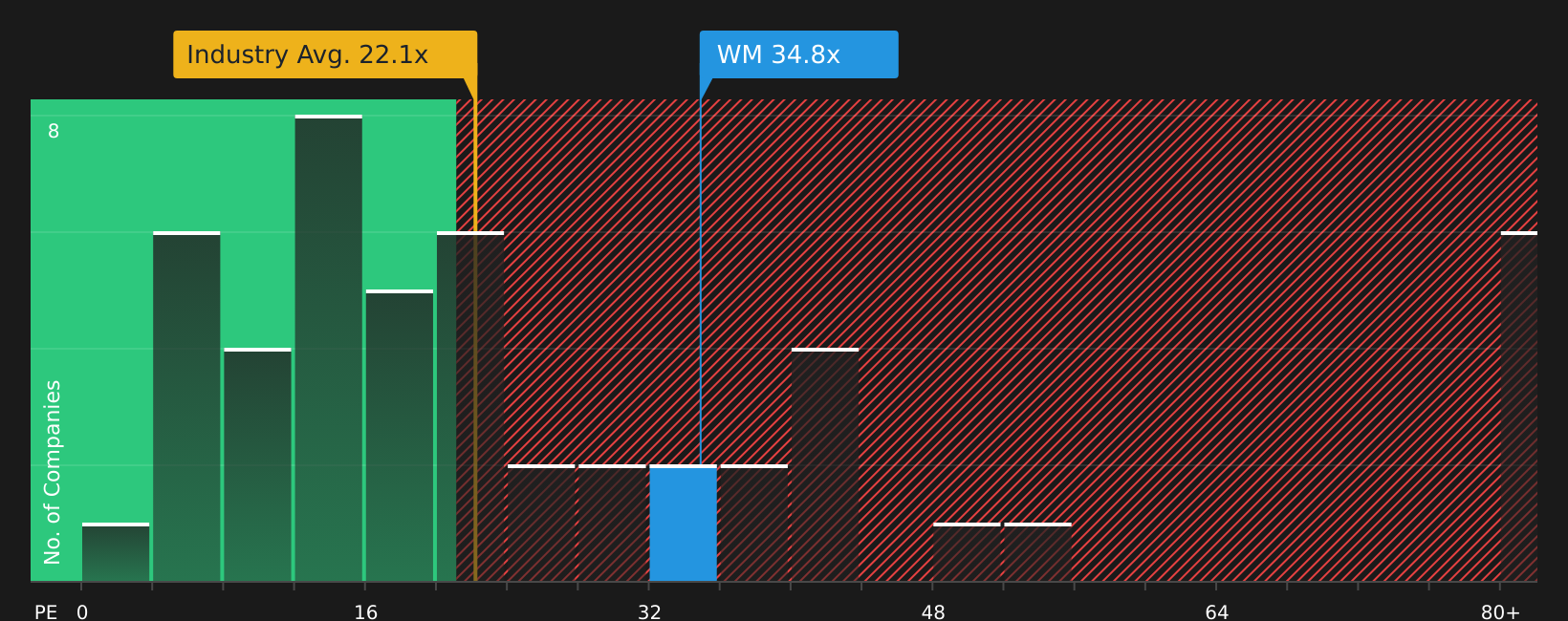

Another Angle: Earnings Multiple Sends A Caution Signal

While the fair value narrative suggests WM is 6.5% undervalued at $251.64 versus the current $235.22, the P/E picture is less comfortable. WM trades on 35x earnings, above the US Commercial Services industry at 25.1x and above its own 33x fair ratio estimate, even though it remains below the 37.5x peer average.

In plain terms, you are paying more than the wider industry but slightly less than similar peers. At the same time, the fair ratio suggests the market could move closer to 33x. Investors may wish to consider whether that premium aligns with WM's growth and dividend profile or whether it reduces the margin for error.

Next Steps

If this combination of optimism and uncertainty around WM has you thinking more carefully about the risk versus reward balance, move quickly to review the full picture in 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If WM has sharpened your focus on quality, do not stop here. Use the Simply Wall Street Screener to compare other options before your next move.

- Spot potential mispriced opportunities early by checking our list of screener containing 24 high quality undiscovered gems that stand out on fundamentals before they hit the mainstream.

- Prioritise resilience by reviewing 80 resilient stocks with low risk scores, highlighting companies with risk scores that may better fit a steadier portfolio core.

- Strengthen your income stream with 13 dividend fortresses, built around companies offering higher yields with an emphasis on durability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.