Assessing Watsco (WSO) Valuation After Giverny Capital’s New Portfolio Position

Watsco, Inc. WSO | 370.31 | -1.49% |

Why Giverny Capital’s Move Put Watsco (WSO) Back on Investors’ Radar

Giverny Capital Asset Management’s decision to initiate a 3.5% portfolio position in Watsco (WSO) has drawn fresh attention to the HVAC distributor’s stock, particularly given the firm’s focus on long term compounders.

The investment firm highlighted Watsco’s role as the largest distributor of HVAC systems in the U.S., as well as its ties with major brands such as Carrier, Rheem, and Daikin, as key reasons for adding the company to its fourth quarter 2025 letter.

That renewed interest has come during a strong run in the shares, with a 4.99% 1 day share price return, 16.16% 30 day share price return and 18.02% year to date share price return, even though the 1 year total shareholder return is an 11.02% loss and the 3 year and 5 year total shareholder returns of 50.58% and 87.28% point to momentum that has built over a longer period.

If you are weighing what else could benefit from similar long term themes, it might be worth casting a wider net across fast growing stocks with high insider ownership.

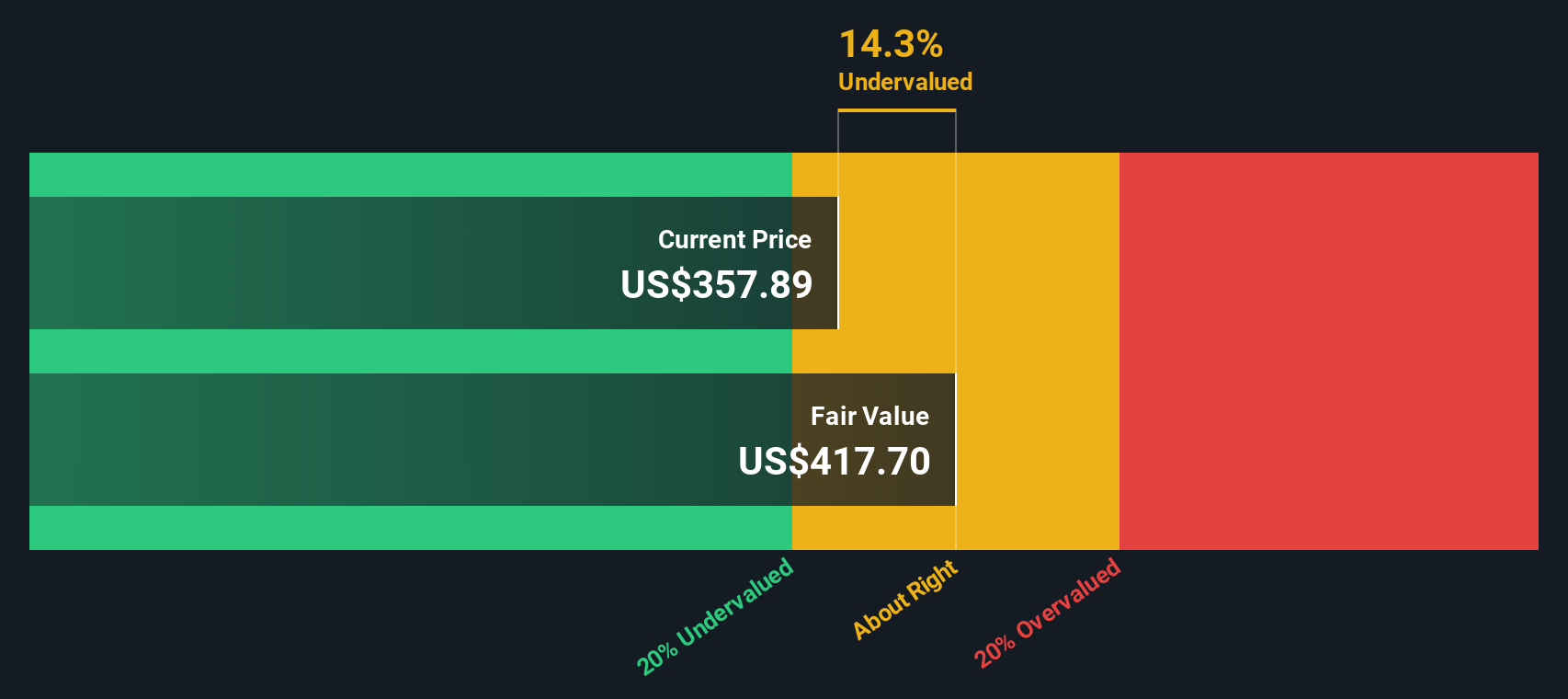

With Watsco trading at US$409.92, sitting above an average analyst price target of US$391.55 but at an estimated 20% discount to intrinsic value, you have to ask: is this a fresh entry point, or is future growth already priced in?

Most Popular Narrative: 0.8% Overvalued

Watsco’s widely followed narrative puts fair value at about $406.60, almost in line with the last close at $409.92, and uses a detailed earnings roadmap to get there.

The analysts have a consensus price target of $468.636 for Watsco based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $550.0, and the most bearish reporting a price target of just $368.0.

Curious how modest revenue assumptions, higher margin expectations, and a richer future earnings multiple all fit together? The narrative spells out a specific profit path and a tighter valuation band that the headline targets alone do not show.

Result: Fair Value of $406.60 (OVERVALUED)

However, tougher HVAC conditions in key Southern markets, along with the possibility of an earnings miss over the next two quarters, could quickly challenge this fair value story.

Another View: Cash Flows Point in a Different Direction

While the narrative prices Watsco at roughly $406.60 and labels the shares as slightly overvalued, the SWS DCF model arrives at a fair value of $514.83, which is about 20.4% above the current $409.92 share price. That gap raises a simple question: are earnings headlines masking a longer term cash flow story?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Watsco for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 865 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Watsco Narrative

If you are not fully aligned with this view or simply like to test the numbers yourself, you can build a custom thesis for Watsco in just a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Watsco.

Looking for more investment ideas?

If Watsco helps sharpen your thinking, do not stop here. The screener can quickly surface other angles you might regret overlooking later.

- Target dependable income by scanning these 11 dividend stocks with yields > 3% that might suit investors who want regular cash returns alongside potential capital gains.

- Spot early trends in automation and machine learning by filtering for these 30 AI penny stocks that could be shaping the future of software and infrastructure.

- Hunt for potential mispricings with these 865 undervalued stocks based on cash flows that line up with your own view on cash flows and long term business quality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.