Assessing Waystar Holding (WAY) Valuation After Strong Q3, Raised Guidance And AI Integration Progress

Waystar Holding Corp. WAY | 0.00 |

Waystar Holding (WAY) just announced a share repurchase program of up to US$200 million, following board authorization of a new buyback plan on May 19, 2026. The announcement has put fresh attention on the stock.

Waystar's share price has rebounded with a 3.90% 1 day share price return and 9.15% 7 day share price return, but that comes after the share price fell 37.62% year to date and total shareholder return declined 49.33% over the past year. This points to improving short term momentum after a difficult stretch.

If this buyback has you rethinking healthcare technology, it can help to compare it with other AI driven healthcare platforms using our focused stock screener, starting with 34 healthcare AI stocks

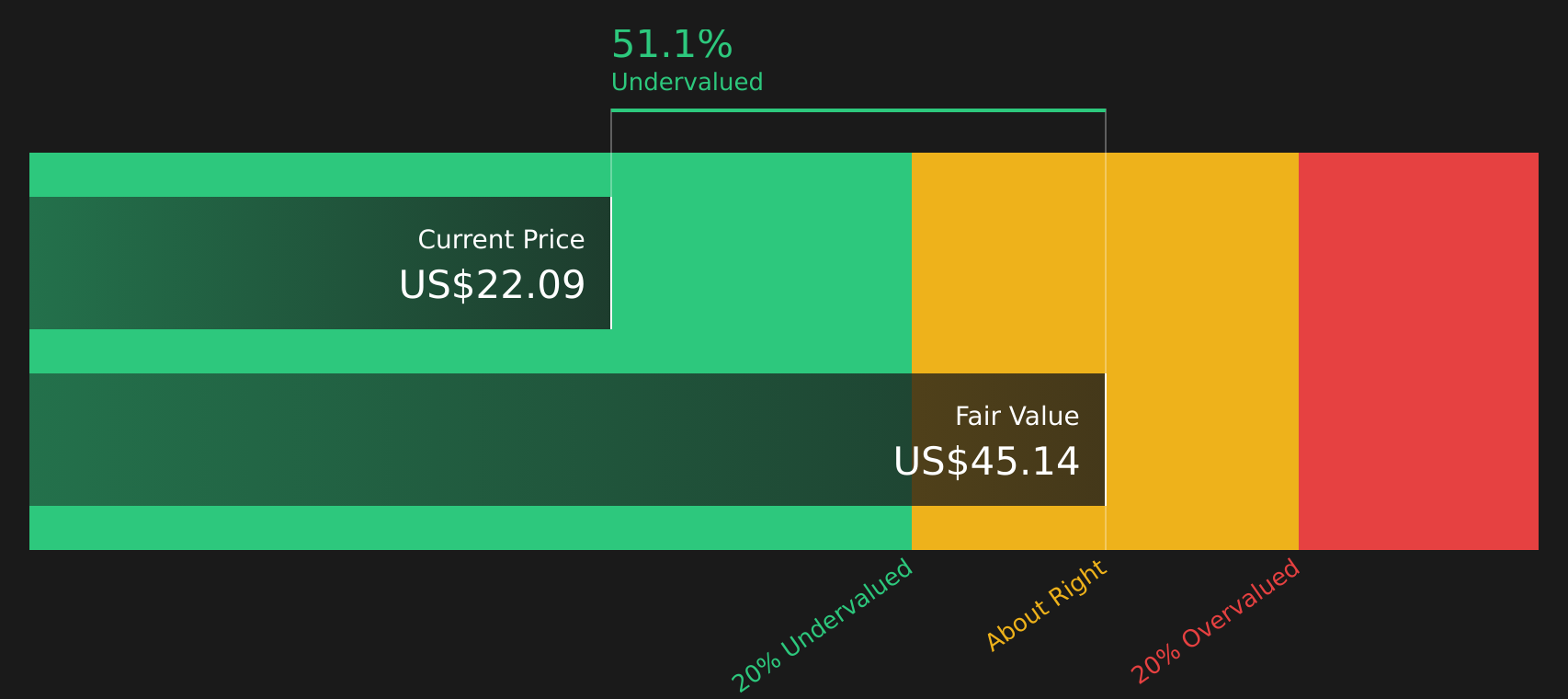

With the stock still down sharply this year, trading around US$19.57 and below analyst price targets, the big question is whether buybacks and AI driven growth make Waystar undervalued or if the market is already pricing in what comes next.

Most Popular Narrative: 42.9% Undervalued

At a last close of $19.57 against a narrative fair value of about $34.26, the current price sits well below what this widely followed view implies.

The acquisition of Iodine Software, a leading provider of AI-powered clinical intelligence, will expand Waystar's total addressable market by over 15%, accelerate its product roadmap, and immediately boost gross margins and adjusted EBITDA margins, setting up compounding, long-term revenue and earnings growth.

Want to see how this story ties together accelerating earnings, rising margins, and a richer profit multiple over time? The underlying model leans on sustained revenue growth and expanding profitability to support that higher fair value target, with analysts split on just how far those earnings could go.

Result: Fair Value of $34.26 (UNDERVALUED)

However, this hinges on execution. Higher post acquisition leverage and potential pricing pressure from larger healthcare clients are both capable of quickly weakening the bullish earnings story.

Another Angle On Valuation

Our DCF model points to a fair value of $47.53 per share, compared with the current price around $19.57. That is a large gap, and it treats Waystar as significantly undervalued. The key consideration is whether you are comfortable with the long term cash flow assumptions behind it.

Next Steps

If the mix of buybacks, AI potential, and valuation gaps seems compelling or questionable, it is worth checking the numbers yourself and not waiting too long to do it. To see exactly what is driving current optimism, take a closer look at the 3 key rewards.

Looking for more investment ideas?

If you stop with just one stock, you might miss opportunities that suit your goals better, so use screeners to pressure test fresh, data driven ideas.

- Jump on potential mispricings by scanning for companies that stand out on quality and value using the 49 high quality undervalued stocks.

- Strengthen your focus on resilience by filtering for companies with healthy financial footing through the solid balance sheet and fundamentals stocks screener (46 results).

- Spot less followed opportunities by using a curated screener containing 21 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.