Assessing Webull (BULL) Valuation After Recent Share Price Rebound And Ongoing Growth Expectations

Bull Run Corp BULL | 0.00 |

Recent performance context for Webull stock

Webull (BULL) has drawn investor attention after a recent 3.4% single day gain, with a share price of $6.10 and mixed short term returns over the past week and month.

The recent 1 day share price gain sits against a tougher backdrop, with the 30 day share price return down 16.8% and the 1 year total shareholder return down 41.5%. This suggests that recent momentum is still rebuilding from a weaker longer term trend.

If this kind of rebound has you thinking more broadly about opportunities, it could be worth scanning 21 top founder-led companies

With Webull trading at $6.10, a value score of 3, and the stock at a sizable discount to the average analyst price target, the key question is whether this signals an undervalued platform or if markets are already pricing in future growth.

Most Popular Narrative: 49.2% Undervalued

With Webull last closing at $6.10 and the most followed narrative pointing to a fair value of $12.00, the gap between price and expectations is wide enough to pay attention to how that view is built.

The successful launch and acceleration of subscription-based offerings such as Webull Premium and paid analytics products are already exceeding targets, combining higher daily trading activity and increased average revenue per user (ARPU) to boost net margins and recurring revenue stability.

Curious what kind of revenue path and margin shift could justify almost doubling the current share price, the narrative leans on rapid top line expansion and a future profit multiple more often associated with mature high growth platforms. Want to see which specific growth and profitability assumptions sit behind that $12.00 fair value and how they stack up against today’s losses?

Result: Fair Value of $12.00 (UNDERVALUED)

However, that upside story also runs into real friction if retail trading activity cools or if tighter global rules slow Webull’s crypto and international expansion.

Another angle on Webull’s valuation

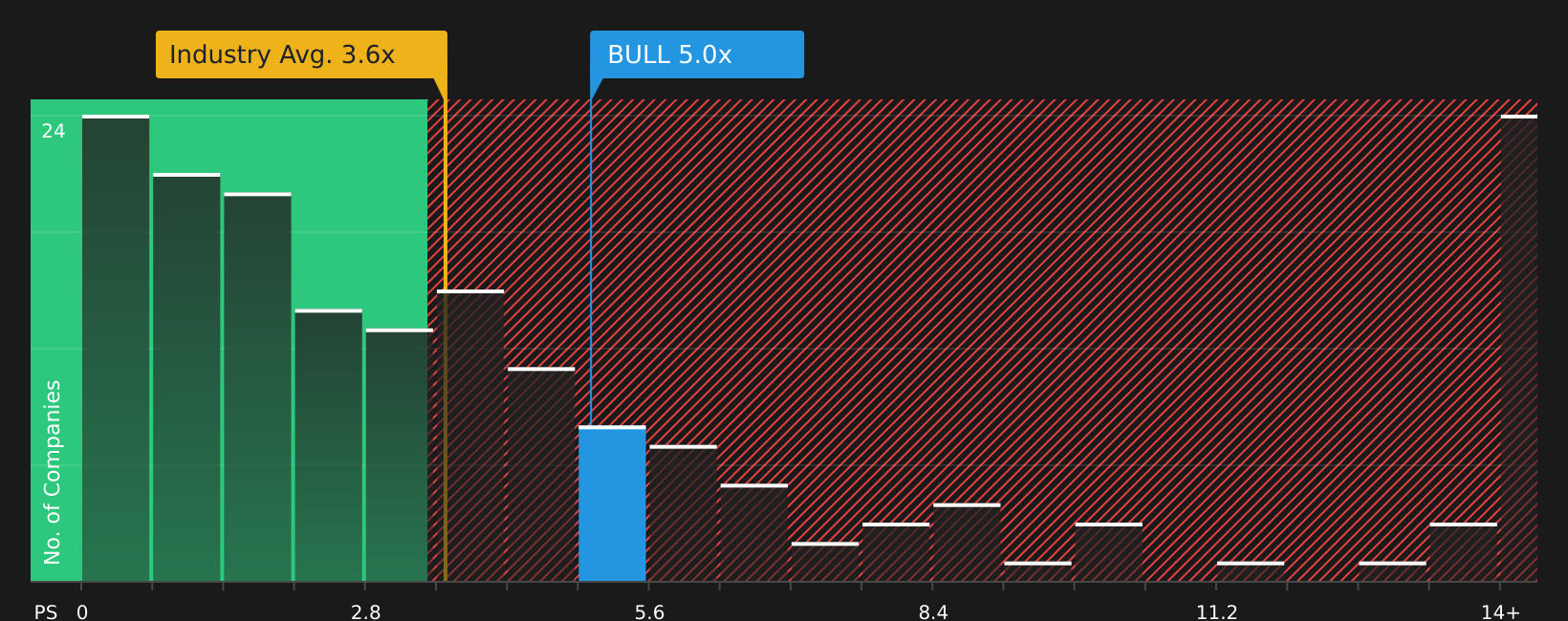

Analysts and the most popular narrative point to Webull being undervalued at $6.10 versus a $12.00 fair value, but the P/S ratio tells a tighter story. At 5.5x sales, the stock trades well above the US Capital Markets average of 3.7x and the 3x fair ratio, which implies less margin for error if growth or margins fall short.

That gap between the current P/S, peers, and the fair ratio suggests investors are already paying up for future execution risk. The question becomes: how much optimism are you really comfortable baking into today’s price, and what would make you change your mind?

Next Steps

With a mix of clear risks and real upside potential running through this story, it may be helpful to move quickly and review the underlying numbers yourself so you are comfortable with your own stance. To see what stands out on both sides, take a closer look at the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If Webull has you thinking more seriously about where your money could work harder, now is the moment to widen the net and compare a few targeted stock ideas.

- Target potential upside with companies that currently look cheap on quality metrics by running through the 47 high quality undervalued stocks.

- Protect your capital by focusing on businesses that pair sturdy finances with sensible debt levels using the 65 resilient stocks with low risk scores.

- Get ahead of the crowd by reviewing the screener containing 22 high quality undiscovered gems before others start paying attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.