Assessing Webull (BULL) Valuation After The Launch Of Vega AI Investment Assistant

Bull Run Corp BULL | 4.82 | +1.69% |

Webull (BULL) is drawing fresh attention after its Australian subsidiary launched Vega AI, an AI-powered investment assistant that offers real-time market analysis, 24/7 decision support, and streamlined financial report summaries for local users.

Vega AI arrives at a time when Webull’s short term momentum has been mixed, with a 7-day share price return of 8.49% and a 30-day share price return of a 17.76% decline, while the 1-year total shareholder return of a 27.45% decline and 3-year total shareholder return of a 17.84% decline suggest sentiment has cooled compared to earlier years.

If this kind of AI-focused product launch has your attention, it could be a good moment to see which other platforms are pushing the boundaries in trading technology through high growth tech and AI stocks.

With Webull posting mixed recent returns, a loss of US$524.7 million on US$514.8 million of revenue, and a value score of 2, is the current price a potential entry point, or is the market already assuming stronger growth ahead?

Most Popular Narrative: 48.9% Undervalued

With Webull closing at US$8.43 against a narrative fair value of US$16.50, the current gap is wide and worth understanding before you judge the price.

Ongoing expansion into new international markets, including recent launches in Canada, Latin America, and Europe, is rapidly diversifying Webull's customer base and driving growth in assets under management (AUM), which supports future revenue and top-line performance.

The launch and acceleration of subscription-based offerings such as Webull Premium and paid analytics products are already exceeding targets, combining higher daily trading activity and increased average revenue per user (ARPU) to influence net margins and recurring revenue stability.

Curious how revenue trends, expected earnings shifts, and a higher future P/E all come together to support that fair value? The narrative focuses on top line expansion, changing margins, and a valuation multiple more typical of higher growth capital markets names. Want to see exactly how those moving parts translate into the US$16.50 figure and what it assumes about 2028 profitability?

Result: Fair Value of US$16.50 (UNDERVALUED)

However, if retail trading activity cools or regulators tighten rules around international and crypto products, the growth story behind that fair value could look very different.

Another View On Valuation

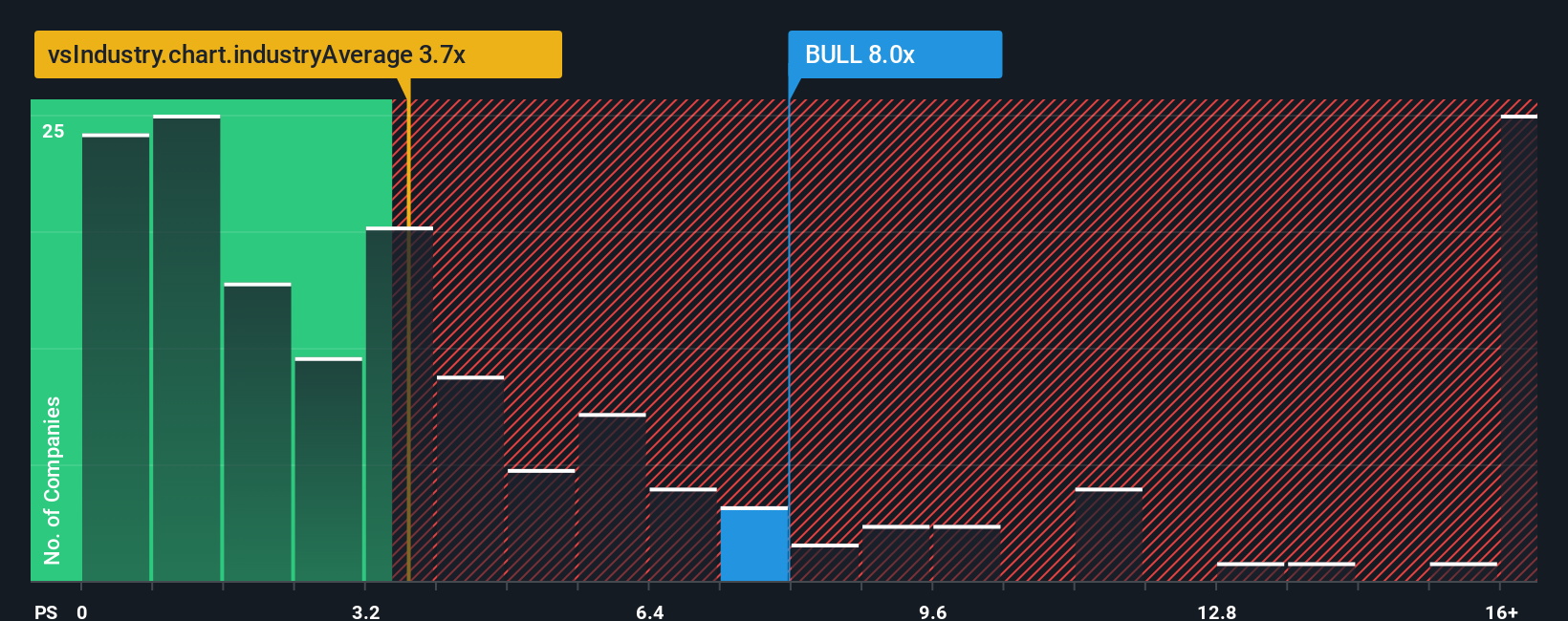

The narrative fair value of US$16.50 paints Webull as undervalued, but the current P/S ratio of 8.2x tells a tougher story. It sits well above the US Capital Markets industry average of 4.2x and a fair ratio of 4.6x, which suggests meaningful valuation risk if sentiment cools.

Put simply, the share price already bakes in much higher sales expectations than both peers and the fair ratio imply. If revenue growth or market enthusiasm slows, that gap could close quickly. The key question is whether you think Webull can grow into this richer pricing.

Build Your Own Webull Narrative

If parts of this story do not line up with your view, or you prefer to rely on your own data work, you can build a customized thesis in just a few minutes with Do it your way.

A great starting point for your Webull research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Webull has sharpened your thinking, do not stop here. Broaden your watchlist with focused screens that surface specific types of opportunities in minutes.

- Target potential value gaps by scanning these 876 undervalued stocks based on cash flows that may be pricing in lower expectations than their cash flows suggest.

- Explore machine learning trends by zeroing in on these 28 AI penny stocks shaping tools, infrastructure, and services tied to AI adoption.

- Identify income ideas by assessing these 11 dividend stocks with yields > 3% offering yields above 3% that could appeal if steady cash returns matter to you.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.