Assessing Wells Fargo (WFC) Valuation After Fed Curbs Lift And Growth Outlook Improves

Wells Fargo WFC | 0.00 |

The recent removal of Federal Reserve enforcement actions on Wells Fargo (WFC), combined with CEO optimism around second quarter results, has refocused attention on how the bank’s growth plans might influence the stock.

At a share price of US$79.44, Wells Fargo has seen a 1-day share price return of 2.94% and a 7-day share price return of 2.48%, even as its 30-day and year to date share price returns are down. Longer term total shareholder returns of 7.31% over 1 year and more than doubling over 3 years point to momentum that has cooled recently as investors weigh the impact of the lifted Fed actions, fresh fixed income offerings, and mixed quarterly results.

If this kind of reset in expectations has you thinking about what else could be interesting in financials and beyond, it can be useful to widen the lens with 20 top founder-led companies

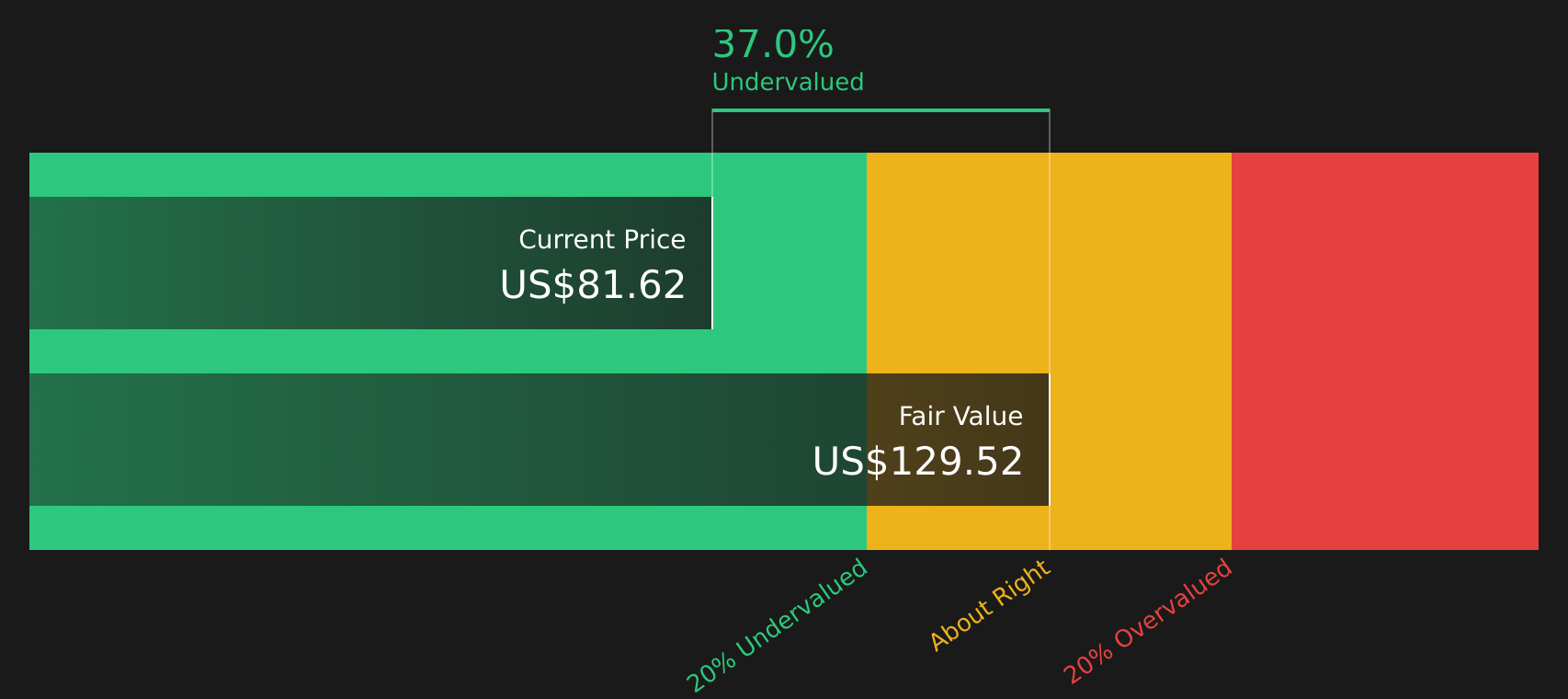

So with Wells Fargo trading at US$79.44, recent underperformance this year, and a reported intrinsic discount and analyst targets above the current price, is the stock offering a genuine opportunity, or are markets already pricing in future growth?

Most Popular Narrative: 18% Undervalued

With Wells Fargo at $79.44 against a narrative fair value of $96.63, the current setup hinges on how the bank executes its growth plans under a higher 8.65% discount rate.

The removal of the asset cap and resolution of multiple regulatory orders unlocks Wells Fargo's ability to aggressively grow its balance sheet, including deposits, loans, and trading assets, after years of constraint, likely resulting in higher revenue and earnings growth over the coming quarters and years.

Want to see what this growth playbook actually assumes? Revenue, profits, and future valuation multiples are all wired into this fair value. The key details are available inside the full narrative.

Result: Fair Value of $96.63 (UNDERVALUED)

However, this hinges on Wells Fargo keeping up with fast moving digital rivals and managing ongoing regulatory and compliance demands, which could keep costs higher for longer.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View: Earnings Multiple Sends A Mixed Signal

Our DCF model points to a fair value of $129.59, which sits well above the $79.44 share price and reinforces the 38.7% implied discount. That sounds appealing, but it also raises a question: is the model too optimistic about future cash flows for a bank growing at mid single digit rates?

Next Steps

Seeing both optimism and caution in the story so far and want to pressure test it with your own lens and move quickly from headline to detail? Take a closer look at the 4 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Wells Fargo has sharpened your focus, do not stop here. Broaden your watchlist with a few targeted stock ideas built from clear, data driven filters.

- Target potential value opportunities by scanning 46 high quality undervalued stocks to identify companies with quality fundamentals that trade below their assessed worth.

- Strengthen your income stream by reviewing 11 dividend fortresses and spot stocks offering higher yields with the backing of detailed payout checks.

- Dial down risk without giving up opportunity through 63 resilient stocks with low risk scores focusing on businesses with more resilient financial profiles and lower risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.