Assessing WeRide (WRD) Valuation After Strong Q3 2025 And Expanded Uber Robotaxi Rollout

WeRide Inc. Sponsored ADR WRD | 7.81 | -1.01% |

WeRide (WRD) is back in focus after a very strong Q3 2025 update on its autonomous mobility platform and a new plan with Uber to roll out 1,200 robotaxis across key Middle Eastern cities.

Despite the strong Q3 2025 update and the expanded Uber robotaxi plan, recent trading has been choppy. The 30 day share price return shows a decline of 25.73%, and the year to date share price return shows a decline of 21.62%, while the 1 year total shareholder return shows a decline of 53.8%, underlining how sentiment had previously cooled and is now being reassessed.

If WeRide’s robotaxi news has caught your attention, it could be a good moment to scan other autonomous and AI transportation names through our screener of 28 robotics and automation stocks.

So, with WeRide’s shares down sharply over the past year despite a very strong Q3 2025 update and a large Uber robotaxi rollout on the way, are you seeing a genuine mispricing here, or is the market already baking in future growth?

Most Popular Narrative: 51.6% Undervalued

WeRide’s most followed narrative pegs fair value at $15.22 versus a last close of $7.36, setting up a wide gap that hinges on aggressive growth and margin assumptions.

The dual deployment of L4 robotaxis and L2+ WePilot 3.0 ADAS in mass production vehicles from Chery EXEED and GAC allows data and software to be reused across product lines. This can spread R&D spending over a larger revenue base and potentially support higher group level margins.

Want to see what kind of revenue ramp and margin shift would need to sit behind that fair value? The narrative leans on fast top line expansion and a future earnings multiple usually seen in high growth segments. Curious which assumptions have to line up for that to work? The full narrative breaks down the exact growth, margin and valuation bridge behind that $15.22 figure.

Result: Fair Value of $15.22 (UNDERVALUED)

However, the whole setup still leans heavily on fresh permits and rider adoption. As a result, any slower regulatory approvals or weaker utilization could quickly challenge that upside story.

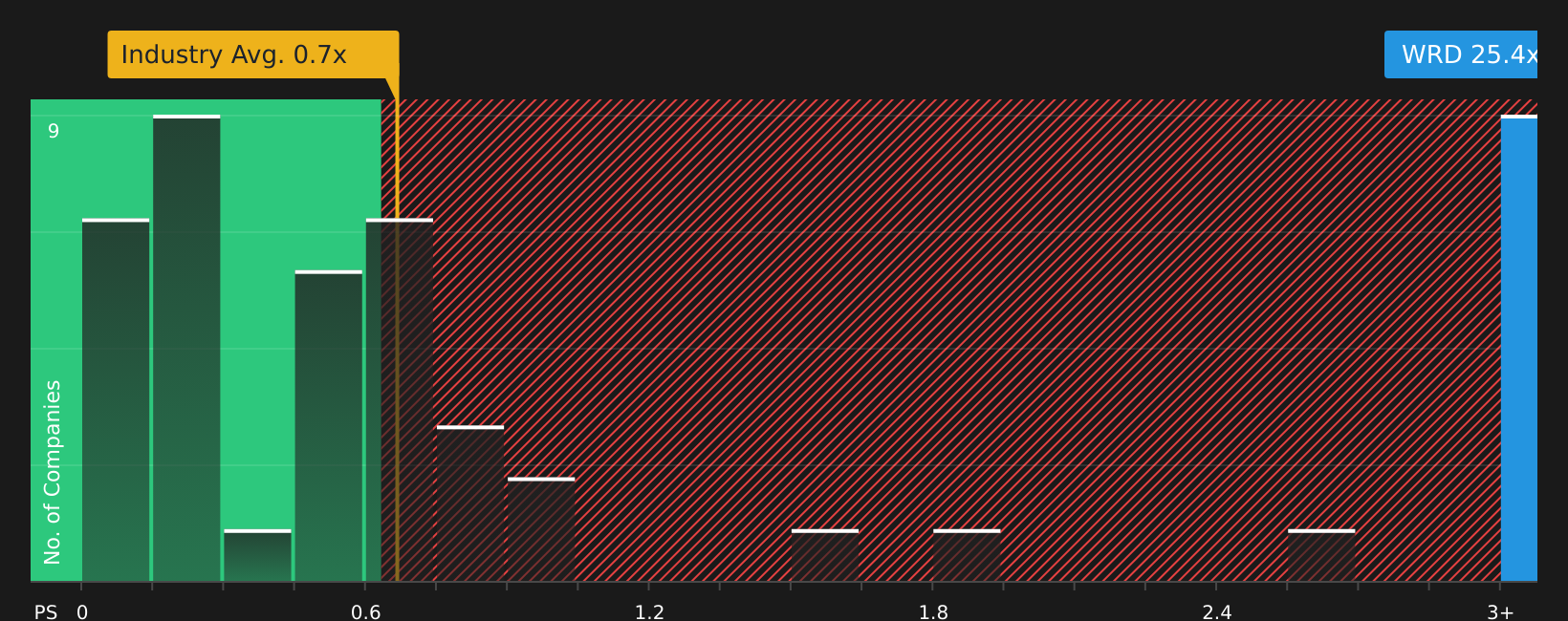

Another View: Price To Sales Flashes Caution

While the narrative and analyst target suggest upside, the current P/S ratio of 34.2x is far above both the US Auto Components industry average of 0.8x and WeRide’s own fair ratio of 8.4x. That rich gap points to meaningful valuation risk if expectations reset. Which signal do you think carries more weight?

Build Your Own WeRide Narrative

If you look at the numbers and reach a different conclusion, or prefer to test your own assumptions directly, you can build a custom WeRide view in a few minutes: Do it your way.

A great starting point for your WeRide research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If WeRide has you rethinking your watchlist, this is the moment to scout a few more angles, before the next wave of stories sets the tone.

- Target potential value plays first and see which names in our list of 53 high quality undervalued stocks line up with your return expectations and risk comfort.

- Prioritize resilience and stress test your portfolio by checking companies in our 86 resilient stocks with low risk scores that score well on business stability and risk metrics.

- Hunt for less crowded opportunities and scan our screener containing 25 high quality undiscovered gems that combine strong fundamentals with relatively limited market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.