Assessing WEX (WEX) Valuation After Health E Commerce Benefits Integration And Board Changes

WEX Inc. WEX | 154.69 | +2.88% |

WEX (WEX) is in focus after Health-E Commerce agreed to integrate its FSA Store and HSA Store directly into the WEX benefits portal, aiming to simplify how FSA and HSA users shop and pay for eligible healthcare expenses.

For context, WEX shares trade at US$157.69, with a 30 day share price return of 5.11% and a year to date share price return of 6.27%. The 1 year total shareholder return of 14.20% and 5 year total shareholder return of 21.84% point to weaker longer term outcomes, so recent product news and board refresh efforts may be coming as momentum is rebuilding from a soft base.

If this kind of benefits focused partnership has caught your attention, it could be a good moment to see what else is happening across high growth tech and AI stocks.

With WEX trading at US$157.69 after a 1 year total shareholder return decline of 14.20% and a 5 year total shareholder return decline of 21.84%, plus an intrinsic discount flag, you have to ask: is there mispricing here, or is the market already baking in whatever growth comes next?

Most Popular Narrative: 10.9% Undervalued

Compared with WEX's last close at US$157.69, the most followed narrative points to a fair value of about US$176.89, framing the stock as undervalued on its own long term cash generation potential under a 9.23% discount rate.

The recent signing of a long-term agreement with BP, including both new card sales and the future conversion of BP's existing commercial fleet portfolio, will expand WEX's reach across core fueling segments and is expected to add 0.5% to 1% to company revenue in the first full year post-conversion, catalyzing revenue acceleration in 2026 and beyond, as digital and card-based payments adoption grows across fleet operations.

Curious how a modest lift in revenue, thicker profit margins, and a lower future P/E come together into that higher fair value line? The full narrative spells out the earnings path, the assumed margin reset, and the valuation multiple needed to bridge from today's price to that US$176.89 outcome.

Result: Fair Value of $176.89 (UNDERVALUED)

However, this hinges on WEX keeping fuel card revenues relevant as fleets shift toward EVs and on holding its ground against rising fintech and large platform competition.

Another Angle: Multiples Paint a Tougher Picture

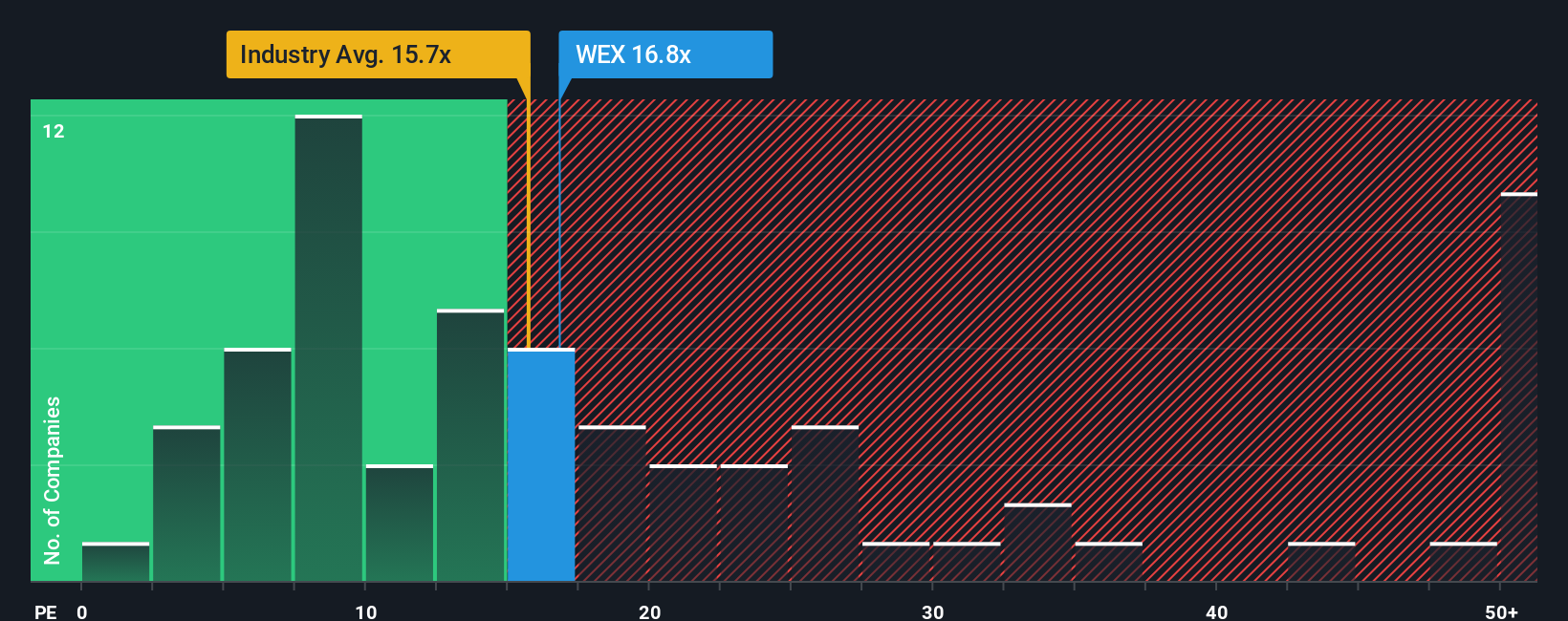

So far, the popular narrative leans on long term cash flows and a fair value near US$176.89. Yet on simple earnings multiples, WEX looks expensive. Its P/E of 19.1x sits above both the US Diversified Financial industry at 14.7x and peers at 15.8x, and even above a fair ratio of 17.9x that the market could move toward. That gap suggests less margin for error if growth or margins do not play out as expected, so which story do you think the market will listen to over time?

Build Your Own WEX Narrative

If you read this and think the assumptions miss something, or simply prefer to weigh the numbers yourself, you can build a custom view with Do it your way in just a few minutes.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding WEX.

Looking for more investment ideas?

If WEX has sparked your interest, do not stop here, the next great idea for your portfolio could be one smart screener away.

- Spot early stage potential by reviewing these 3531 penny stocks with strong financials that already show solid financial underpinnings instead of just hype.

- Position yourself in the AI trend by checking out these 24 AI penny stocks that align with your risk level and time horizon.

- Prioritise value by scanning these 865 undervalued stocks based on cash flows where market prices and underlying cash flows may be out of sync.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.