Assessing Whether Acadia Healthcare Company (ACHC) Is Overvalued Or Undervalued After Its Recent Share Price Rebound

Acadia Healthcare Company, Inc. ACHC | 0.00 |

Event driven snapshot of Acadia Healthcare Company (ACHC)

Acadia Healthcare Company (ACHC) shares have been volatile recently, with a 9% decline over the past week offset by gains of about 5% over the month and roughly 86% in the past 3 months.

At a share price of $25.27, Acadia Healthcare Company's recent share price return shows sharp short term swings but strong recent momentum, with a 5.47% 30 day gain and 86.49% 90 day gain. This contrasts with a more modest 6.18% one year total shareholder return and weak three year and five year total shareholder returns.

If this kind of rebound has you looking beyond a single stock, it can be worth scanning for other opportunities using a focused screener for 35 healthcare AI stocks.

With the stock at $25.27, an intrinsic discount of about 71% and a modest 12% gap to the average analyst price target, investors now face a key question: is this a genuine mispricing or is future growth already in the price?

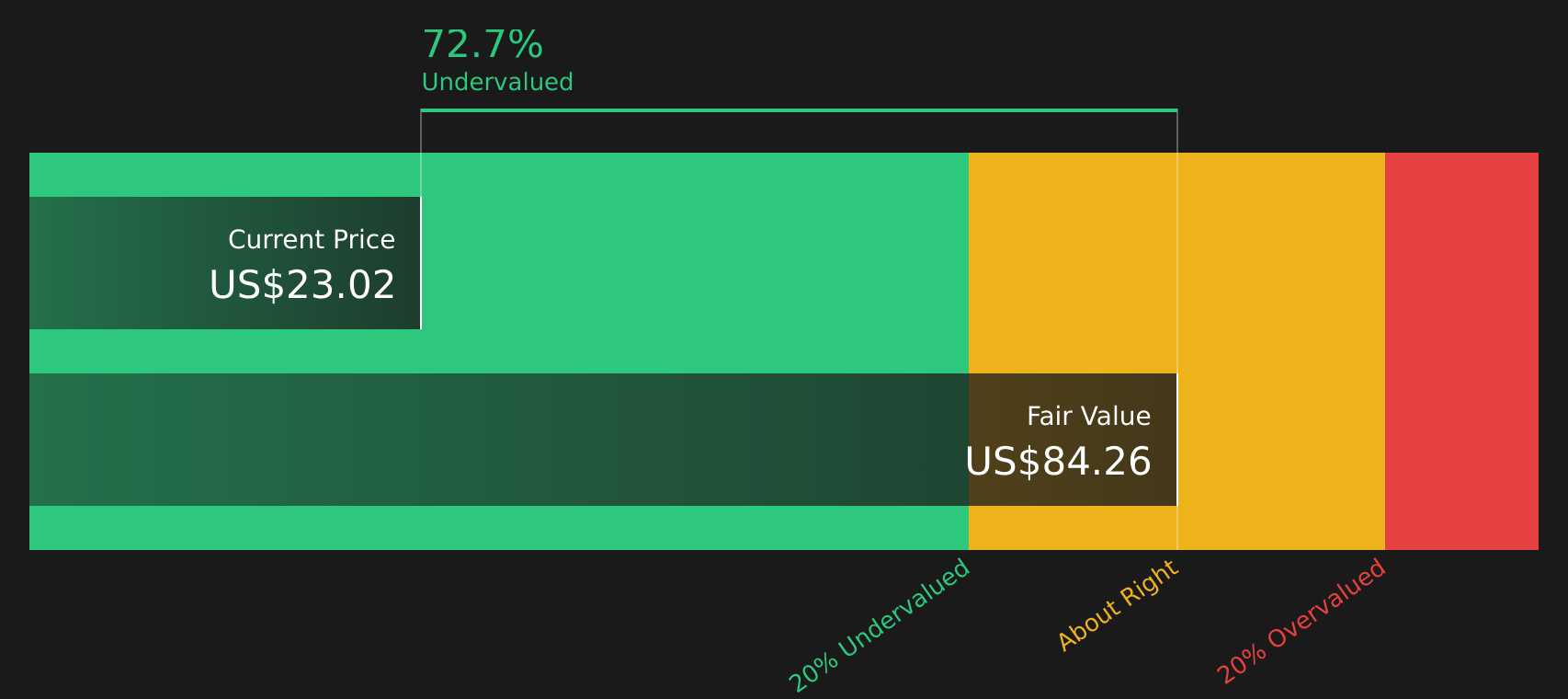

Most Popular Narrative: 111.6% Overvalued

According to the most followed narrative, Acadia Healthcare Company's fair value sits at $11.94, well below the last close of $25.27. This frames the recent rebound in a very different light.

This is not a high-growth technology story. It is a capacity-and-execution story in a market where demand is persistent and under-supplied. If Acadia continues to expand responsibly while maintaining care quality, its relevance is likely to increase rather than fade.

To understand what drives that valuation gap, the narrative focuses on expectations for future profitability, measured revenue growth and margins that would need to support a much richer cash flow profile.

Result: Fair Value of $11.94 (OVERVALUED)

However, the narrative could be challenged if Acadia struggles to convert revenue into consistent profits, given its recent net income loss, or if regulatory and reimbursement pressures squeeze margins further.

Another angle on valuation

The most followed narrative pegs fair value at $11.94, yet our DCF model points the other way, with an estimated future cash flow value of $88.62 per share, suggesting the stock is trading well below that level. When two methods disagree this sharply, which set of assumptions would you trust?

Next Steps

Conflicted by the mix of risks and rewards in this story? Use the full set of data, including the 3 key rewards and 1 important warning sign in the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop with a single stock, you could miss other opportunities that fit your style, so consider widening your search with focused screens built from the same data.

- Spot potential overreactions in smaller companies by scanning 22 elite penny stocks with strong financials that pair low share prices with stronger financial profiles.

- Target quality at a sensible price by reviewing 51 high quality undervalued stocks built around solid cash flows and balance sheets.

- Prioritize staying power by checking 72 resilient stocks with low risk scores that surface companies with more resilient risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.