Assessing Whether Tesla (TSLA) Still Looks Undervalued After Recent Share Price Pullback

Tesla Motors, Inc. TSLA | 0.00 |

Recent performance snapshot

Tesla (TSLA) has seen mixed share performance recently, with the stock down about 4.8% over the past day and 1.4% over the past week, while showing gains over the past month and the past 3 months.

At a share price of US$422.24, Tesla’s recent pullback over the past week comes after a stronger 30 day share price return of 7.73%, while its 1 year total shareholder return of 20.65% and 3 year total shareholder return of 134.40% point to momentum that has built over a longer horizon.

If you are looking beyond Tesla for ideas in related areas of the market, it may be worth scanning 30 robotics and automation stocks as another way to find automation focused opportunities.

With Tesla trading at US$422.24, slightly above the average analyst price target and its internal intrinsic estimate, the key question is whether today’s price still leaves room for upside or if the market is already pricing in future growth.

Most Popular Narrative: 28.2% Undervalued

Based on the most widely followed narrative, Tesla’s fair value of $588.18 sits well above the recent share price of $422.24, which frames the stock as materially discounted according to that view.

If Tesla executes on these high-growth, high-margin opportunities, it could reach a multi-trillion-dollar valuation by 2035, making today’s sentiment-driven sell-off an attractive buying opportunity.

Curious what sits behind that bold valuation gap? The narrative leans heavily on rapid revenue expansion, higher long term profit margins, and a premium future earnings multiple more often associated with mature tech platforms than auto manufacturers.

Result: Fair Value of $588.18 (UNDERVALUED)

However, this upbeat “physical AI” story still faces real tests, especially around full FSD and robotaxi approvals, as well as the huge capital commitments needed to scale Optimus.

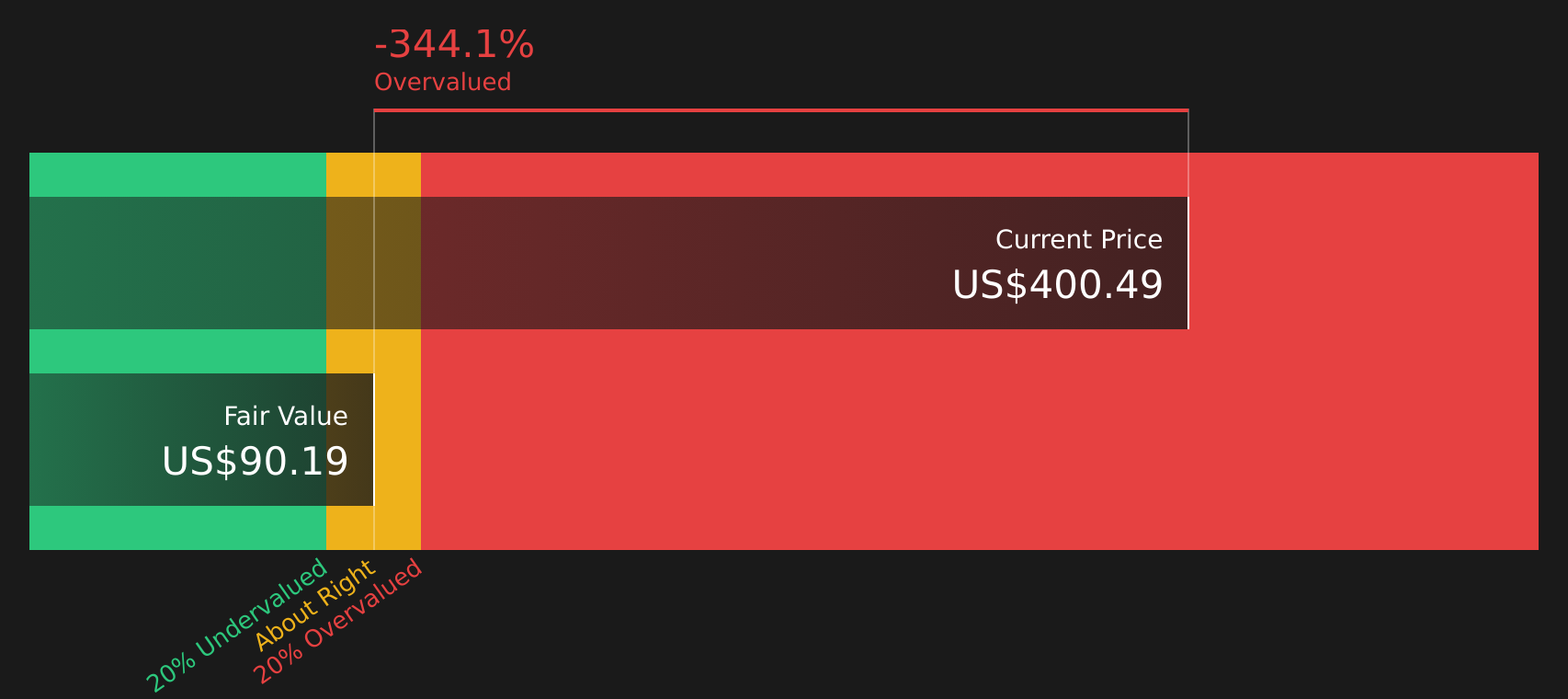

Another way to look at value

The community narrative leans on long term growth assumptions, but Simply Wall St’s own DCF model paints a different picture. With Tesla at $422.24 trading above an estimated future cash flow value of $141.87, this framework flags the stock as expensive and leaves investors to judge which story feels more realistic.

For anyone who wants to see how that cash flow view is built from the ground up, Look into how the SWS DCF model arrives at its fair value.

Next Steps

The mixed views in this article show there is both concern and optimism around Tesla, so it is worth checking the underlying numbers and forming your own stance with 1 key reward and 2 important warning signs

Looking for more investment ideas?

If Tesla is only one piece of your watchlist, you may want to broaden your scope with a few focused stock ideas that could help sharpen your overall portfolio.

- Target potential mispricings by reviewing 50 high quality undervalued stocks that combine solid fundamentals with room for the market to reassess them.

- Strengthen your income stream by scanning 12 dividend fortresses that aim to pair higher yields with more resilient business models.

- Prioritize resilience by checking out 66 resilient stocks with low risk scores that show steadier risk profiles and may help balance more volatile positions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.