Assessing Willis Lease Finance (WLFC) Valuation After Strong Multi Year Shareholder Returns

Willis Lease Finance Corporation WLFC | 175.89 | +0.15% |

Why Willis Lease Finance Has Caught Investor Attention

Willis Lease Finance (WLFC) has attracted investor attention after its share price moved sharply in recent months, with gains over the past month and the past three months prompting closer scrutiny of the business.

At a latest share price of $200.18, Willis Lease Finance has shown strong momentum, with a 30 day share price return of 34.61% and a 90 day share price return of 66.29%, while its 5 year total shareholder return is a little over 5x. Overall, the stock has combined sharp recent share price gains with a very large multi year total shareholder return, which suggests investors have been reassessing both its growth prospects and risk profile over time.

If this kind of move has you looking beyond a single name, it could be a good moment to widen your search with our 22 top founder-led companies.

With WLFC now at $200.18 and trading above the latest analyst price target of $160, the obvious question is whether recent strength has pushed the stock ahead of itself or if the market is only starting to price in future growth.

Most Popular Narrative: 3% Overvalued

At $200.18, the most followed narrative puts Willis Lease Finance’s fair value slightly lower at $195.26, so you are looking at a modest premium that rests on specific assumptions about future earnings and valuation multiples.

The acquisition of nearly $1 billion in engines and aircraft, with a substantial portion being future technology assets like LEAP and GTF engines, positions the company for growth with more valuable and in-demand assets, potentially driving higher revenue and margins.

The expansion and modernization of the portfolio to 53% future technology assets as of the end of the year should lead to greater lease revenues, as these newer engines are anticipated to be more desirable in the market.

Want to see what kind of revenue path and profit margins have to line up with that asset mix to justify today’s valuation premium, and what future earnings multiple this narrative is leaning on to make the numbers work? The full story connects those moving parts in a way the headline price alone does not.

Result: Fair Value of $195.26 (OVERVALUED)

However, higher interest costs or unexpected maintenance issues on complex LEAP and GTF engines could quickly challenge the earnings and valuation assumptions behind this story.

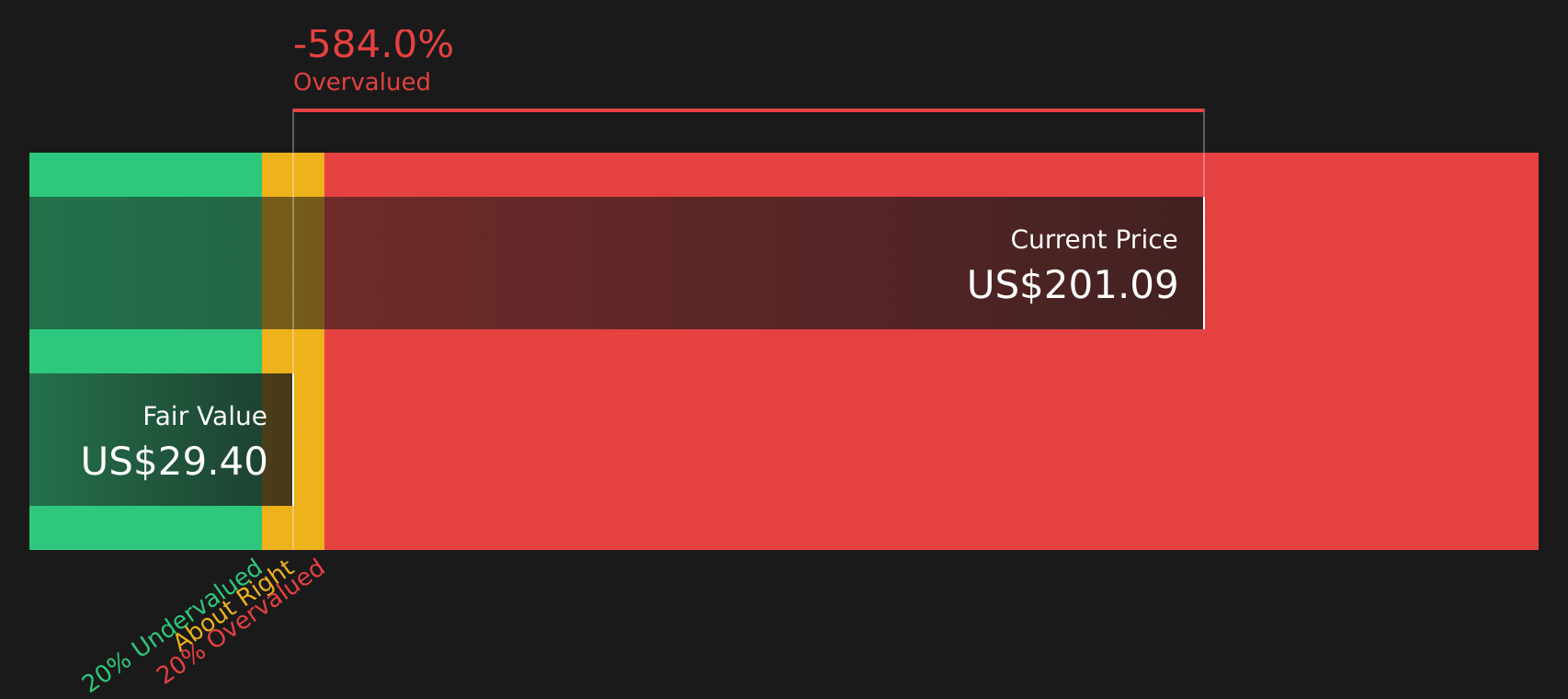

Another Way To Look At Valuation

While the narrative model suggests Willis Lease Finance is around 3% overvalued at $195.26 versus the $200.18 share price, the SWS DCF model is far more cautious, with a future cash flow value of $29.89. When one model points to a mild premium and another to a steep one, which set of assumptions do you trust more?

Build Your Own Willis Lease Finance Narrative

If you look at those inputs and reach a different conclusion, or simply prefer to test your own assumptions, you can build a custom view in minutes by starting with Do it your way.

A great starting point for your Willis Lease Finance research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are serious about levelling up your portfolio, do not stop at one stock. Use these focused screens to spot opportunities others might overlook.

- Target value opportunities backed by solid fundamentals through our 53 high quality undervalued stocks and see which companies currently stand out on both quality and price.

- Prioritise resilience by checking companies that score well on balance sheet strength using our solid balance sheet and fundamentals stocks screener (45 results) so you are not caught off guard in tougher periods.

- Hunt for underfollowed names with strong fundamentals using our screener containing 24 high quality undiscovered gems before they land on everyone else’s radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.