Assessing Winmark (WINA) Valuation After Strong Multi Year Shareholder Returns

Winmark Corporation WINA | 430.43 | -0.61% |

Why Winmark Stock Is Drawing Attention Now

Winmark (WINA) has been getting a closer look from investors after its recent share performance, with the stock last closing at $452.94. That move is prompting fresh questions about what current fundamentals may imply for valuation.

The recent move to a share price of $452.94 sits on top of a 30 day share price return of 8.89% and a year to date share price return of 12.79%, while the 1 year total shareholder return of 19.46% and 5 year total shareholder return of 208.62% point to momentum that has been strong over both shorter and longer horizons.

If Winmark’s performance has you looking beyond a single stock, this could be a good moment to broaden your watchlist with fast growing stocks with high insider ownership.

With the shares at $452.94 after multi year returns that have been very strong, some investors may wonder whether Winmark still trades below what it is worth or whether the market is already pricing in future growth.

Price-to-Earnings of 39.1x: Is It Justified?

At a last close of $452.94, Winmark is trading on a P/E of 39.1x, which screens as expensive against both its industry and peer benchmarks.

The P/E multiple links the current share price to earnings per share, so a higher figure usually implies the market is paying up for current profits and what it expects those profits to do over time. For a franchisor and resale focused retailer like Winmark, that kind of premium often reflects views on the resilience of its franchise model, the stability of its cash generation, and the trajectory of underlying earnings growth.

Here, the market is assigning Winmark a 39.1x P/E, which is almost double the US Specialty Retail average of 20.5x and far above the peer average of 11.2x. That spread is also wide compared to an estimated fair P/E of 12.6x, indicating the current valuation is well ahead of the level our fair ratio work suggests the market could move toward if expectations were to cool.

Result: Price-to-Earnings of 39.1x (OVERVALUED)

However, that premium P/E could be vulnerable if annual revenue growth of 4.6% and net income growth of 7.9% slow or if franchise-focused resale demand softens.

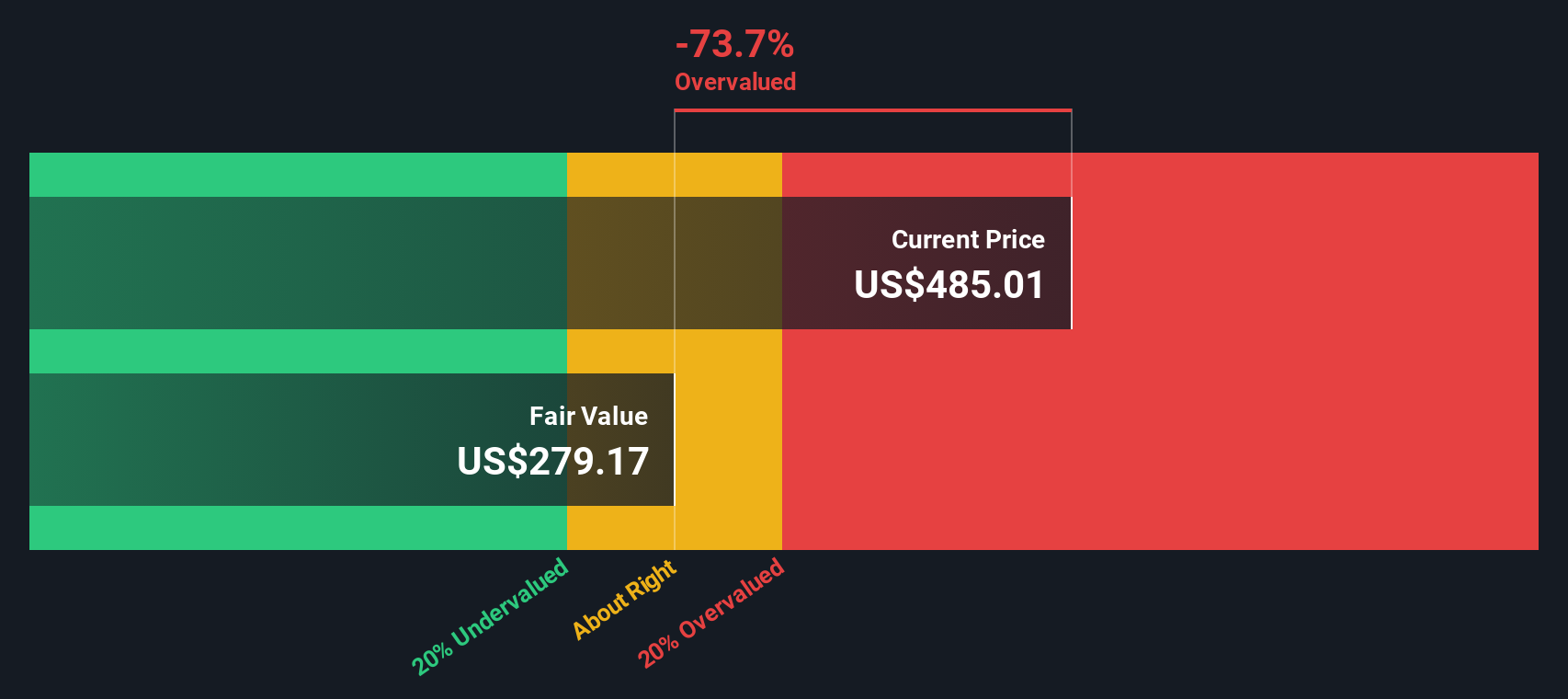

Another View Using Our DCF Model

Our DCF model points in the same direction as the P/E check, with an estimated future cash flow value of $294.98 versus the current $452.94 share price. That gap suggests the market is paying a steep premium, so the key question is what expectations are reflected in that difference.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Winmark for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 864 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Winmark Narrative

If this view does not line up with your own or you prefer to work from the raw numbers yourself, you can review the data and build a custom story in just a few minutes, then Do it your way.

A great starting point for your Winmark research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Searching for your next investment idea?

If you stop with one stock, you risk missing other opportunities that fit your style, so use the screener to line up your next round of ideas.

- Spot potential value setups by scanning these 864 undervalued stocks based on cash flows that currently trade below what their cash flows may imply.

- Tap into long term themes in healthcare by reviewing these 109 healthcare AI stocks that link medical data with AI driven solutions.

- Expand your watchlist into digital assets by checking out these 18 cryptocurrency and blockchain stocks tied to blockchain, payments, and infrastructure plays.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.