Assessing Winnebago Industries (WGO) Valuation After High‑Profile Florida RV SuperShow Launches

Winnebago Industries, Inc. WGO | 30.36 | +0.50% |

Winnebago Industries (WGO) is in focus after using the Florida RV SuperShow to showcase new RV lineups, including the Sunflyer Class C, Thrive lightweight trailer, and Grand Design RV’s Foundation 42GD destination trailer.

That product push comes as momentum in Winnebago Industries’ share price has been building, with a 56.64% 90 day share price return and a 9.28% 30 day share price return. However, the 5 year total shareholder return of 20.20% shows a weaker longer term picture.

If the Florida RV SuperShow has you thinking more broadly about the auto and recreational vehicle space, it could be a good time to scan auto manufacturers for other ideas on your radar.

With Winnebago shares up 56.64% over 90 days but showing a weaker 5 year total return of 20.20%, and trading only about 2% below the US$48.75 analyst target, is there real upside left, or is the market already banking on future growth?

Most Popular Narrative: 1.3% Undervalued

With Winnebago Industries last closing at US$47.79 against a narrative fair value of about US$48.42, the valuation gap is tight but still meaningful for anyone tracking how earnings and margins could reshape the story.

The analysts have a consensus price target of $38.083 for Winnebago Industries based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $75.0, and the most bearish reporting a price target of just $26.0.

Want to see what turns a wide spread of analyst targets into a fair value near US$48? Revenue growth, margin rebuild, and a future earnings multiple all play central roles, and the exact mix may surprise you.

The most followed narrative arrives at a fair value of roughly US$48.42 per share using a 12.19% discount rate, which sits just above the current US$47.79 share price and implies a small valuation gap. That view rests on specific assumptions for Winnebago Industries’ future revenue growth, profit margins, earnings power by around 2028, and the P/E multiple that could be applied to those earnings, all brought back to today’s terms using that discount rate.

Those assumptions include expectations for multi year revenue growth, a shift from current profitability levels to healthier margins, earnings reaching into the hundreds of millions of US dollars, and a future P/E that sits below the current figure cited for the broader US Auto industry. The narrative also factors in a modest reduction in share count each year, which supports earnings per share, and then aggregates these cash flows and terminal expectations into the US$48.42 fair value estimate.

Result: Fair Value of $48.42 (UNDERVALUED)

However, softer retail demand and pressure on premium RV pricing could still weigh on revenue and margins, particularly if dealers maintain leaner inventories for an extended period.

Another Angle: Multiples Send A Different Signal

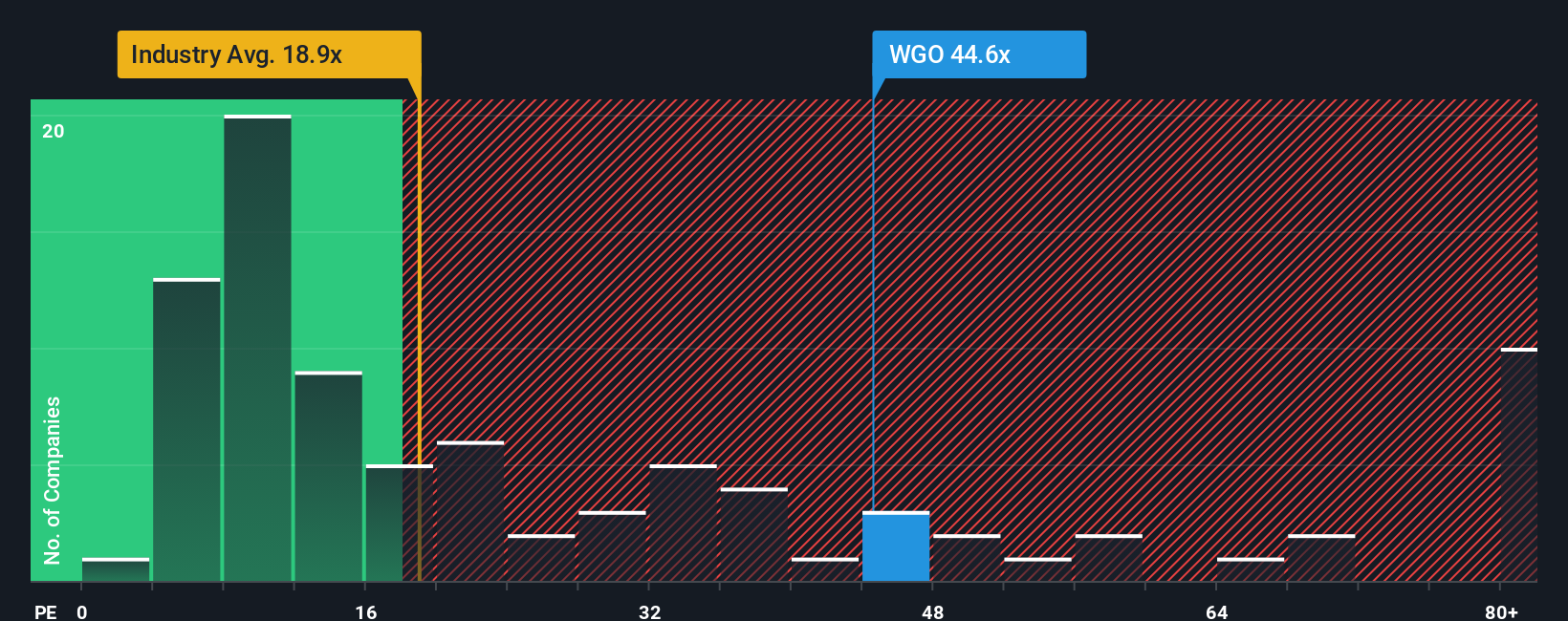

The narrative fair value suggests Winnebago Industries is about 1.3% undervalued, but the market is pricing the shares very differently when you look at earnings. At a P/E of 37.1x versus a fair ratio of 24.3x, the stock also sits well above both the peer average of 15.6x and the global auto industry at 18.5x. That sort of gap points to meaningful valuation risk if sentiment or earnings expectations shift, so you need to ask yourself which story you trust more: the narrative model or the earnings multiple on the screen today.

Build Your Own Winnebago Industries Narrative

If you look at these numbers and come to a different conclusion, or simply prefer to test your own assumptions, you can build a custom story in just a few minutes with Do it your way.

A great starting point for your Winnebago Industries research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at one stock. Use the tools at your fingertips so you are not leaving opportunities on the table.

- Target potential mispricings by scanning these 873 undervalued stocks based on cash flows that could offer a price tag below what their cash flows might justify.

- Ride emerging tech trends by checking out these 24 AI penny stocks that are tied to real business models rather than just hype.

- Strengthen your income stream by reviewing these 12 dividend stocks with yields > 3% that already show yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.