Assessing Zeta Global Holdings (ZETA) Valuation As Revenue Grows But Losses Persist

Zeta Global ZETA | 15.79 | +0.38% |

Why Zeta Global Holdings (ZETA) is on investors’ radar

Zeta Global Holdings (ZETA) has drawn attention recently as investors weigh its share price of US$20.45 against its current fundamentals. These include annual revenue of US$1.22b and a reported net loss of US$22.81 million.

Recent trading has been choppy, with a 2.20% 1 day share price return and an 8.25% 7 day share price decline. However, a 30 day share price return of 11.63% and a 90 day gain of 9.42% suggest that momentum has been positive overall. The 3 year total shareholder return of about 13x also hints at how sentiment around growth potential and risk has shifted over time.

If you are tracking how software and data focused names are moving, this could be a good moment to broaden your watchlist with high growth tech and AI stocks.

With Zeta generating US$1.22b in revenue but still reporting a net loss of US$22.81m, and trading at US$20.45 with an indicated intrinsic discount, you have to ask whether this is a mispriced growth story or whether the market is already baking in what comes next.

Price-to-Sales of 4.1x: Is it justified?

On a P/S of 4.1x and a last close of US$20.45, Zeta Global Holdings screens as undervalued compared with peers, its industry, and an estimated fair ratio.

The P/S ratio compares the company’s market value to its revenue and is often used for software and other loss making names where earnings are not yet a stable guide. For Zeta, this lens matters because the business is still reporting a net loss of US$22.81m on revenue of US$1.22b, so investors are effectively paying for current sales and the potential that those sales eventually translate into profit.

On this measure, Zeta is described as good value versus similar companies, with its 4.1x P/S well below a peer average of 12.5x and below the US Software industry average of 4.5x. It is also below an estimated fair P/S ratio of 5.6x. This suggests there may be scope for the valuation multiple to move closer to that fair level if the company’s growth and profitability story develops as expected.

Result: Price-to-Sales of 4.1x (UNDERVALUED)

However, you still need to consider that Zeta is loss making and highly data dependent. As a result, any setback in profitability or data access could quickly challenge this valuation story.

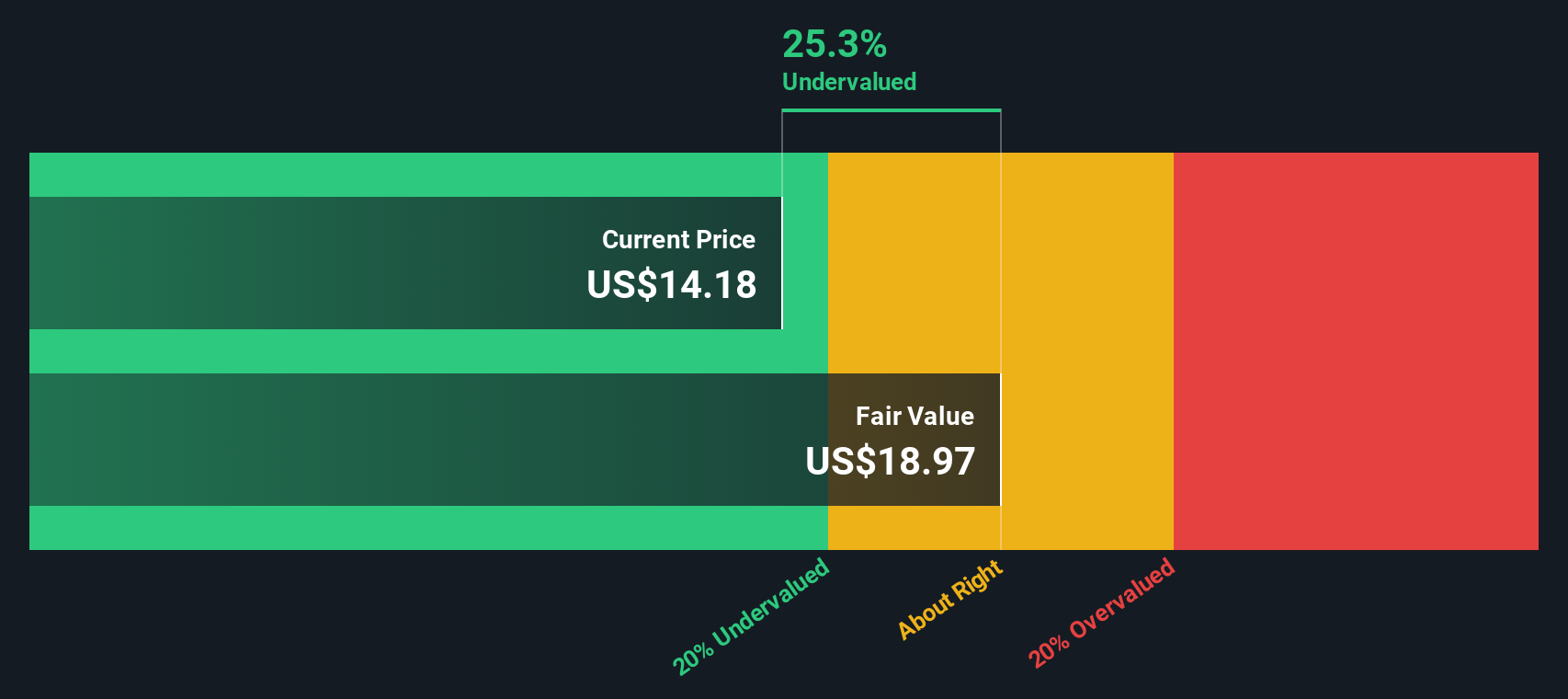

Another way to look at value

The SWS DCF model also points to Zeta Global Holdings being undervalued, with a future cash flow value of US$26.18 compared with the current share price of US$20.45. That gap suggests investors are either cautious about those future cash flows or waiting for clearer proof of profitability.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Zeta Global Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 883 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Zeta Global Holdings Narrative

If you see the numbers differently or simply prefer to test your own view, you can build a complete Zeta Global Holdings narrative in just a few minutes with Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Zeta Global Holdings.

Looking for more investment ideas?

If Zeta has caught your attention, do not stop there; broaden your opportunity set by checking other ideas on the Simply Wall St Screener before the market moves on.

- Spot potential value opportunities early by scanning these 883 undervalued stocks based on cash flows that may not yet be on everyone’s radar.

- Target fast moving themes by reviewing these 24 AI penny stocks positioned around artificial intelligence and related technology trends.

- Lock in income focused ideas by filtering for these 13 dividend stocks with yields > 3% that align with your yield expectations.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.