Astera Labs (ALAB) Valuation After Earnings Beat Guidance Lift And Margin Jitters

Astera Labs ALAB | 117.14 | +10.17% |

Why Astera Labs Stock Sold Off After Strong Q4

Astera Labs (ALAB) reported stronger than expected fourth quarter results and issued upbeat guidance tied to AI connectivity demand, yet the stock dropped as investors focused on margins and a chief financial officer transition.

The company posted fourth quarter sales of US$270.58 million versus US$141.10 million a year earlier, with net income of US$44.98 million compared with US$24.71 million. Basic earnings per share from continuing operations were US$0.27, and diluted earnings per share were US$0.25, up from US$0.15 and US$0.14 respectively in the prior year period.

For 2025 as a whole, Astera Labs reported sales of US$852.53 million versus US$396.29 million a year earlier. Net income was US$219.13 million, compared with a net loss of US$83.42 million. Basic earnings per share from continuing operations were US$1.32, versus a basic loss per share of US$0.64, while diluted earnings per share from continuing operations were US$1.22, versus a diluted loss per share of US$0.64.

Management also issued guidance for the first quarter of 2026, calling for revenue between US$286 million and US$297 million, and GAAP diluted earnings per share of roughly US$0.36 to US$0.38 on about 184 million weighted average diluted shares outstanding. That outlook reflected the company’s expectations for continued demand in cloud and AI infrastructure connectivity.

Yet despite the earnings beat and guidance, Astera Labs shares fell about 20% as investors weighed concerns around potential gross margin pressure. Commentary highlighted a product mix shift, including a higher contribution from Taurus modules, and the impact of a new warrant arrangement with Amazon that is tied to future product purchases that could reach US$6.5 billion.

The Amazon agreement points to meaningful revenue potential if volume thresholds are met. However, it also raised questions for some investors about future profitability levels. At the same time, a sharp move in the share price after results suggests expectations were already high, making the stock more sensitive to any perceived pressure on margins.

Astera Labs management has emphasized growing AI infrastructure demand and adoption of its connectivity chips by large customers, including Nvidia, AMD, Amazon and Google. The company’s products sit in the data center plumbing that links accelerators, CPUs, memory and storage, an area many investors view as closely tied to hyperscaler spending on AI.

Even so, the immediate reaction after earnings underlined how closely the market is watching the balance between growth, profitability and customer concentration. Concerns around margin trends, contract structures and the mix between modules and other offerings all fed into the pullback, despite the strong top line and earnings figures reported for 2025.

Astera Labs shares have been volatile around these announcements, with a 7-day share price return of a 23.86% decline and a 30-day share price return of a 28.95% decline. However, a 1-year total shareholder return of 47.21% suggests longer term momentum has still been positive.

If this kind of AI infrastructure story has your attention, it can be useful to see what else is out there in the theme. Take a look at our screen of 34 AI infrastructure stocks for other names linked to data center build outs.

With the stock down sharply over the past month but still showing a 47.21% 1 year total return and trading at a discount to the average analyst price target, you have to ask: is this a reset that leaves upside on the table, or is the market already baking in years of future growth?

Most Popular Narrative: 35.1% Undervalued

Astera Labs' most followed narrative sets a fair value of about $199.15 per share, well above the recent $129.32 close. That puts a spotlight on the assumptions behind that gap.

Expansion across multiple high-growth connectivity standards (PCIe, Ethernet, CXL, and UALink) alongside deepening partnerships with leading industry players (NVIDIA, AMD, Microsoft, SAP, Alchip) positions Astera Labs to leverage the ongoing digital transformation and migration to advanced data center architectures, reducing customer concentration risk while driving higher gross margins from increased product mix and attach rates.

Want to see what kind of revenue build, margin profile and earnings power that product and customer roadmap is mapping to? The narrative leans on aggressive top line expansion, fatter profit margins and a rich future earnings multiple that is usually reserved for market leaders. Curious how those pieces fit together to justify a fair value well above where the stock trades today?

Result: Fair Value of $199.15 (UNDERVALUED)

However, that upside case still leans heavily on hyperscaler AI capex and on open standards like UALink gaining traction, both of which could break the story if they disappoint.

Another Take: Rich P/E Signals Very Different Story

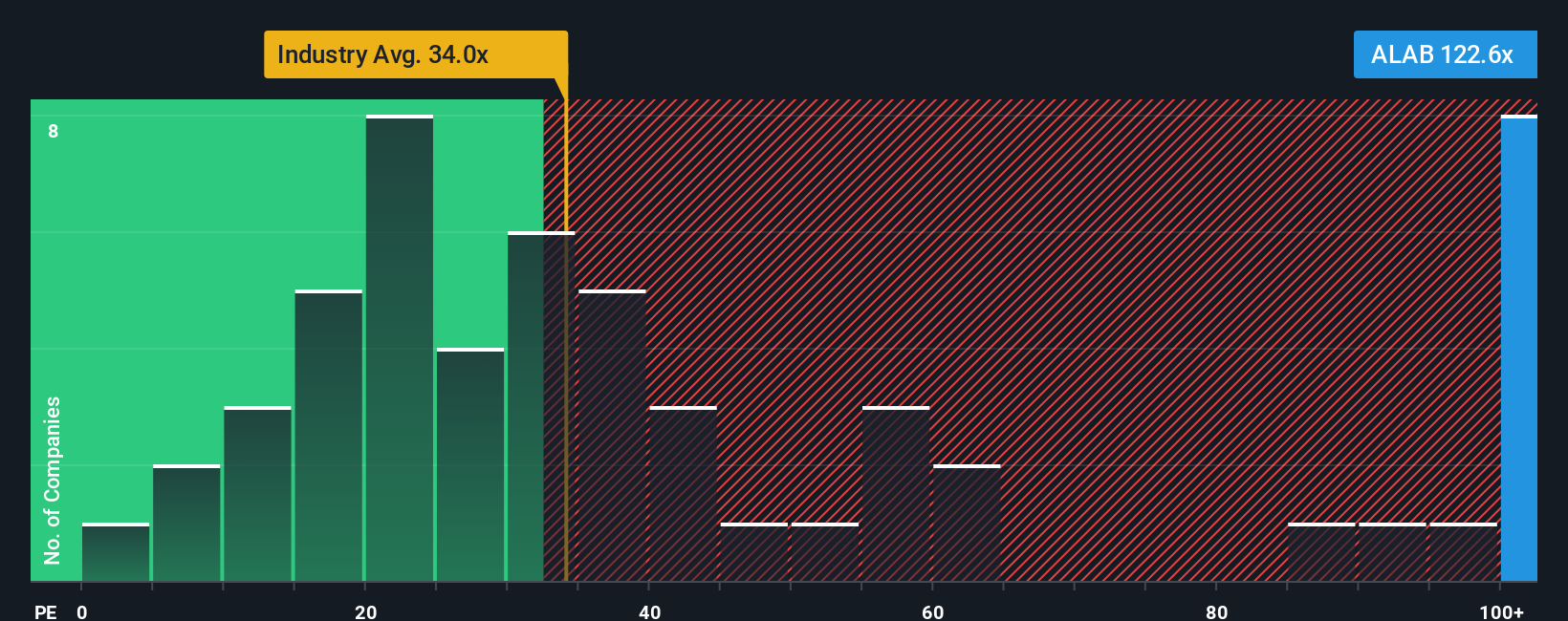

Those fair value narratives lean on optimistic growth and margin assumptions, but the market is already pricing Astera Labs on a P/E of 100.5x. That is far above the US Semiconductor industry at 43.4x, the peer average at 70.3x, and even the fair ratio estimate of 80x, which suggests limited room for disappointment. This raises a key question: is this a quality compounder in the making, or a story that leaves very little margin for error?

Build Your Own Astera Labs Narrative

If you are not fully convinced by these viewpoints or prefer to lean on your own work, you can test the same data, sketch your assumptions, and build a personalized thesis in just a few minutes: Do it your way.

A great starting point for your Astera Labs research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Astera Labs has sharpened your interest in AI and chips, do not stop here. The wider market still holds plenty of opportunities you will want to size up.

- Target value first by scanning companies that our screener tags as 53 high quality undervalued stocks, so you are not ignoring potential mispriced names.

- Prioritise resilience by checking out the 84 resilient stocks with low risk scores, especially if you want business models with steadier risk profiles on your watchlist.

- Hunt for future standouts using the screener containing 23 high quality undiscovered gems, before others start paying attention to the same quality metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.