Astronics (ATRO) Valuation Check After Reaffirmed 2025 Results And Strong 2026 Revenue Outlook

Astronics Corporation ATRO | 76.26 76.65 | +0.26% +0.51% Pre |

Why Astronics is on investors’ radar right now

Astronics (ATRO) is back in focus after announcing preliminary, unaudited fourth quarter and full year 2025 results, while reiterating its 2026 revenue outlook of US$950 million to US$990 million.

The reaffirmed guidance, which implies projected revenue growth of about 10% to 15% over 2025, gives investors a clearer anchor for evaluating the company’s order trends and end market demand.

The reaffirmed 2026 revenue outlook and upcoming TD Cowen aerospace and defense conference appearance have coincided with strong momentum, reflected in a 15.77% 1-month share price return at US$76.58 and a very large 1-year total shareholder return. This suggests investors are reassessing both growth prospects and risk.

If Astronics’ recent move has you looking beyond a single name, this can be a moment to broaden your watchlist with our 24 power grid technology and infrastructure stocks tied to critical infrastructure themes.

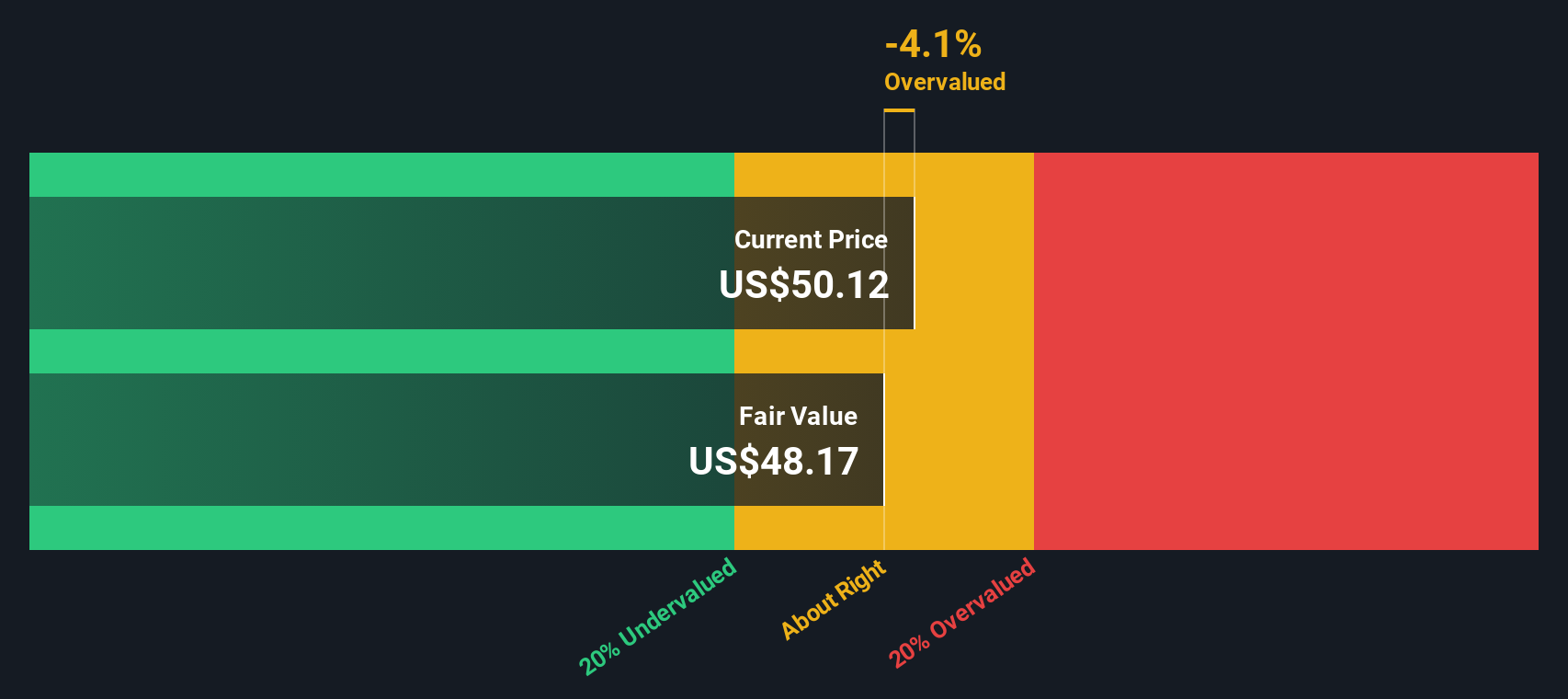

With Astronics reporting revenue of US$830.601 million, guiding to higher 2026 sales and trading just below its average analyst target, the key consideration is whether there is still an opportunity for investors or if the market is already pricing in that anticipated growth.

Most Popular Narrative: 25.2% Overvalued

Simply Wall St’s most followed narrative puts Astronics’ fair value at $61.18, well below the recent $76.58 close, and builds a detailed case around growth, margins, and required returns.

Fair Value: edged down from $62.75 to approximately $61.18, reflecting modestly lower long term assumptions.

Discount Rate: risen slightly from about 7.90% to roughly 7.94%, indicating a marginally higher required return.

Want to see what kind of revenue path and margin profile are baked into that fair value, and which future earnings multiple ties it all together? The full narrative lays out the growth curve and profitability assumptions step by step so you can judge whether this pricing gap feels justified or stretched.

Result: Fair Value of $61.18 (OVERVALUED)

However, that story can change quickly if new tariffs lift costs faster than pricing, or if Test segment execution issues resurface and pressure margins again.

Another Angle on Astronics’ valuation

Our DCF model puts Astronics’ value at $73.63 per share, slightly below the recent $76.58 price. This points to a modestly overvalued signal rather than the larger gap implied by the $61.18 fair value narrative. If both models are right, how much margin of safety do you really have?

Build Your Own Astronics Narrative

If you see the numbers differently or want to stress test your own assumptions, you can pull the same data, weigh the trade offs, and Do it your way in just a few minutes.

A great starting point for your Astronics research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Astronics has sparked your curiosity, do not stop here. Widen your opportunity set with a few focused stock ideas that could support your portfolio thinking.

- Target potential mispricing by scanning 52 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect their underlying business strength.

- Strengthen your income stream by checking out 14 dividend fortresses designed to surface companies offering higher yields backed by resilient cash flows.

- Sleep easier at night by reviewing 82 resilient stocks with low risk scores that score well on financial stability and overall risk factors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.