Avista (AVA) Faces A Retirement Update But Is The Stock Already Fairly Valued

Avista Corporation AVA | 0.00 |

Avista (AVA) stock is in focus after the company announced that Jason R. Thackston, Senior Vice President of Growth, Energy Policy and External Relations, plans to retire effective January 1, 2027.

At a share price of $41.90, Avista has posted a 1.8% 1 day share price return and an 8.2% year to date share price return. Its 1 year total shareholder return of 15.8% suggests steady momentum that puts the latest leadership news into a context of gradually improving sentiment rather than a sharp re rating.

If management changes at Avista have you thinking about where else capital might work hard, this is a good moment to scan 34 power grid technology and infrastructure stocks

Avista appears to be a solid regulated utility business with electricity and gas operations across several northwestern states, and the stock has quietly moved higher. The next step is clear: are investors now paying too much for that stability?

Most Popular Narrative: 2.1% Undervalued

With Avista closing at $41.90 against a narrative fair value of $42.80, the current price sits slightly below what the most followed narrative models in.

The analysts have a consensus price target of $42.8 for Avista based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $50.0, and the most bearish reporting a price target of just $39.0.

Want to see what is sitting behind that small undervaluation gap? The narrative leans on steady revenue expansion, firmer margins, and a richer earnings multiple. Curious which assumptions really drive that $42.80 fair value and how sensitive it is to those inputs? The full narrative sets it out step by step.

Result: Fair Value of $42.80 (UNDERVALUED)

However, the Avista narrative still faces clear pressure points, including concentrated exposure to Pacific Northwest regulation and weather, as well as rising grid and wildfire mitigation costs that could strain returns.

Another View on Avista: Cash Flows Paint a Different Picture

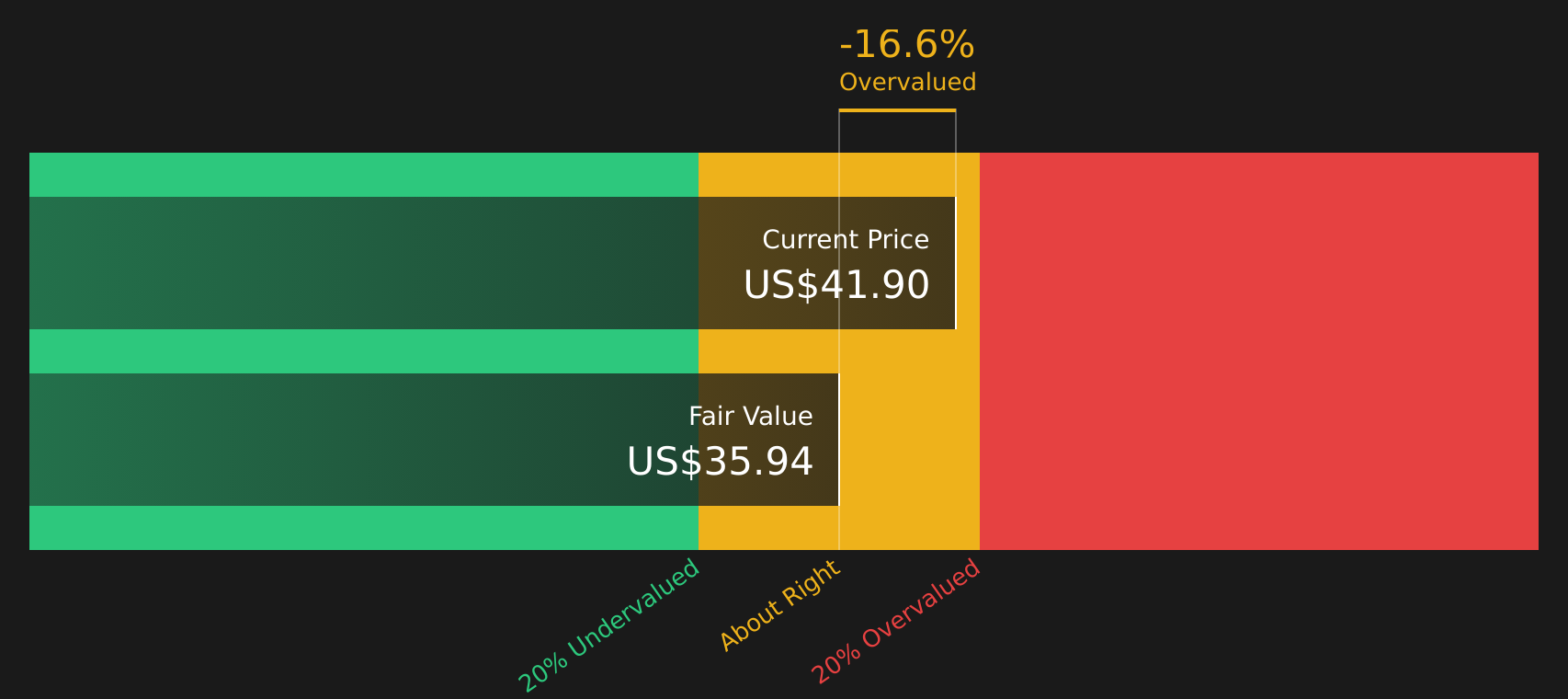

While the current Avista narrative points to a fair value of $42.80 and a small 2.1% gap to the $41.90 share price, the SWS DCF model tells a different story. On that cash flow view, Avista screens as overvalued, with an estimate of $35.94. When the signals conflict, which lens do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Avista for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals around Avista have you on the fence, this is the moment to weigh the concerns against the potential and shape your own view with 4 key rewards and 2 important warning signs

Looking for more investment ideas beyond Avista?

If Avista has sharpened your appetite for opportunities, do not leave it there. Use the Simply Wall St Screener to turn that curiosity into a list of concrete ideas.

- Target durable balance sheets by scanning companies in the solid balance sheet and fundamentals stocks screener (47 results) that may handle pressure better than most.

- Hunt for value by reviewing the 45 high quality undervalued stocks that might trade below what their fundamentals suggest.

- Focus on income by checking the 9 dividend fortresses that aim to pair higher yields with resilience.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.