Avista (AVA) Stock Could Be 4.3% Undervalued After Data Center Pause

Avista Corporation AVA | 0.00 |

Avista (AVA) recently paused new large data center energy requests, including talks on a prospective 500 MW project in Washington, after community concerns about its potential impact and the need for broader stakeholder alignment.

The pause on data center requests has coincided with a 3.42% decline in Avista's 1 day share price return to $40.98 and a softer 7 day share price return of 2.43%. However, its year to date share price return of 5.84% and 1 year total shareholder return of 16.50% indicate momentum that has built over a longer period despite recent volatility.

If the data center pause has you thinking about broader infrastructure themes, it could be worth scanning other power grid and transmission names via this 35 power grid technology and infrastructure stocks

With Avista stock returning 16.50% over the past year and now trading only about 1.7% below the average analyst price target, investors have to ask: Is potential upside already reflected, or is the data center uncertainty creating a fresh opportunity that markets are not fully pricing in?

Most Popular Narrative: 4.3% Undervalued

Against Avista's last close at $40.98, the most followed narrative points to a fair value of $42.80, leaving a modest valuation gap that hinges on long term grid investment and regulatory outcomes.

The sharp rise in large industrial and commercial load inquiries, with over 3,000 megawatts in the pipeline compared to a roughly 2,000 megawatt current peak load, signals accelerating electrification and potential for outsized rate base and revenue growth if even a fraction of these loads materialize over the next 3 to 5 years. Robust, multi-year capital investment plans approaching $3 billion (2025 to 2029), with additional potential from grid expansion projects and new generation needs tied to large load requests, position Avista to earn regulated returns and support long-term earnings expansion.

Curious what sits behind that fair value for Avista stock? The narrative focuses on measured revenue growth, firmer margins, and a future earnings multiple that is lower than the wider utilities sector. Want to see how those assumptions compare over the forecast period and what discount rate ties it all together?

Result: Fair Value of $42.80 (UNDERVALUED)

However, Avista's concentrated presence in the Pacific Northwest, along with the rising capital needs for grid modernization, wildfire mitigation, and clean tech investments, could strain earnings and balance sheet flexibility if regulatory support lags.

Another View: What The SWS DCF Model Says About Avista Stock

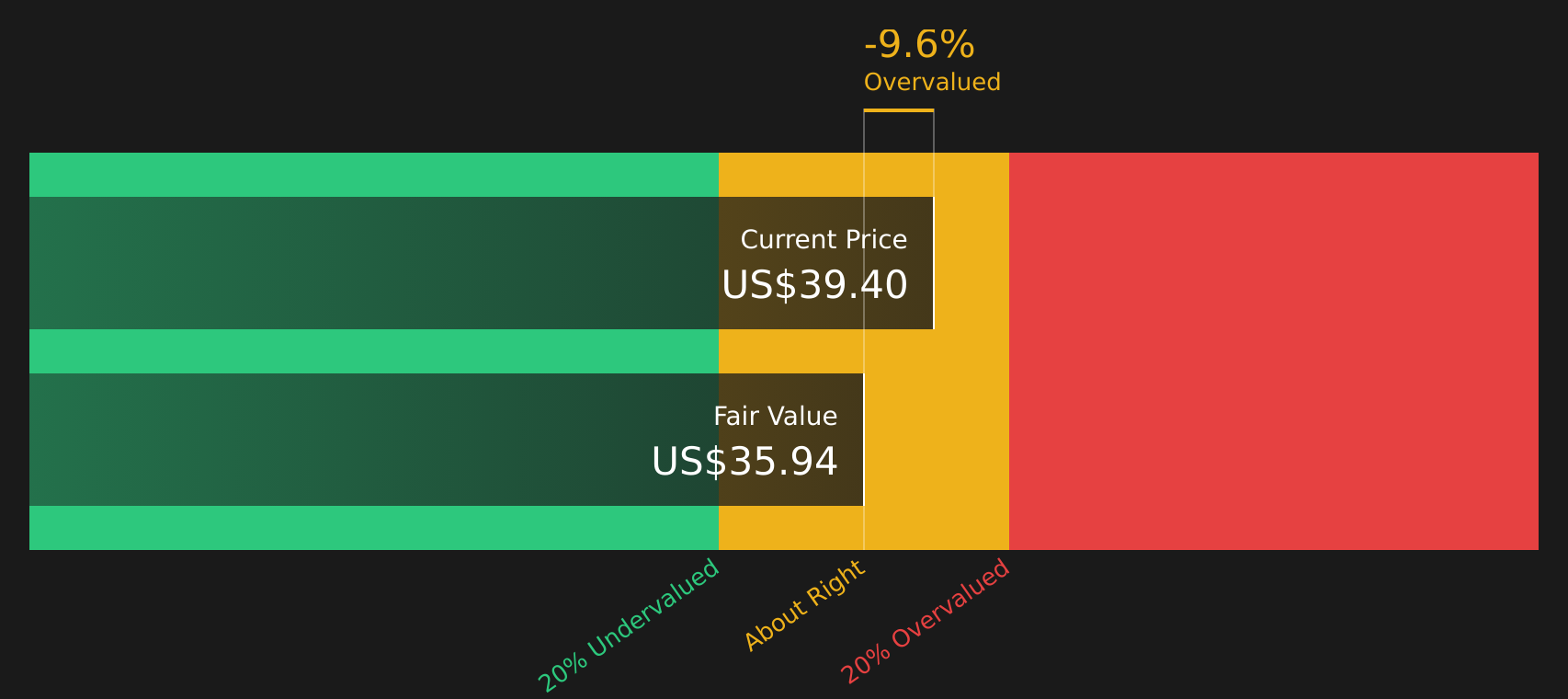

While the popular narrative points to Avista stock trading around 4.3% below a $42.80 fair value, the SWS DCF model tells a different story. On that measure, Avista at $40.98 sits above an estimated future cash flow value of $35.94, so the shares appear overvalued on that basis.

When two approaches disagree like this, it encourages investors to consider which assumptions around cash flows, growth, and required returns align best with their own thesis.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Avista for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Given the mixed signals around Avista and its data center pause, it makes sense to look at the underlying numbers and sentiment yourself. To weigh both the concerns and the potential upside, start by reviewing the 4 key rewards and 2 important warning signs

Looking for more investment ideas beyond Avista?

If Avista has sharpened your focus on where to put fresh capital, do not stop here. The next step is lining up a wider watchlist of potential candidates.

- Spot potential low-priced opportunities early by scanning through 23 elite penny stocks with strong financials that pass stricter financial quality checks.

- Target quality at a discount by reviewing the 47 high quality undervalued stocks that combine stronger fundamentals with pricing that some investors may be overlooking.

- Prioritize resilience by focusing on 68 resilient stocks with low risk scores that carry lower overall risk scores without ignoring underlying business strength.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.