Axon Enterprise (AXON) Is Down 9.1% After Raising 2026 Revenue Outlook on Strong AI-Driven Q1

Axovant Sciences Ltd AXON | 0.00 |

- Axon Enterprise reported past first-quarter 2026 results showing revenue of US$807.35 million versus US$603.63 million a year earlier, with net income rising from US$87.98 million to US$169.31 million and diluted earnings per share from continuing operations increasing from US$1.08 to US$2.05.

- The company also lifted its full-year 2026 revenue growth outlook to a range of 30% to 32%, underscoring how its expanding AI-driven product suite is reshaping Axon’s business mix and earnings profile.

- Next, we’ll examine how Axon’s raised 2026 revenue guidance and accelerating AI adoption interact with its existing investment narrative and expectations.

Capitalize on the AI infrastructure supercycle with our selection of the 39 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Axon Enterprise Investment Narrative Recap

To own Axon Enterprise, you need to believe it can keep deepening its role as a core software and hardware platform for public safety, with AI tools making its ecosystem more valuable over time. The key near term catalyst is how fast agencies adopt Axon’s AI ERA offerings. The biggest risk remains its dependence on public budgets and shifting attitudes toward policing. The latest earnings beat and raised guidance reinforce the AI-driven catalyst, but do not remove that budget risk.

The most relevant update is Axon’s decision to lift its 2026 revenue growth outlook to 30% to 32%. This tighter, higher range supports the idea that accelerating adoption of AI products like Axon Vision and Axon Assistant is already feeding into larger contracts and stronger net revenue retention, which matters directly for the near term catalyst of AI-led upselling and for testing how resilient demand is against any future budget tightening.

Yet, while guidance is higher, the risk that tighter public safety budgets could constrain future orders is something investors should be aware of if...

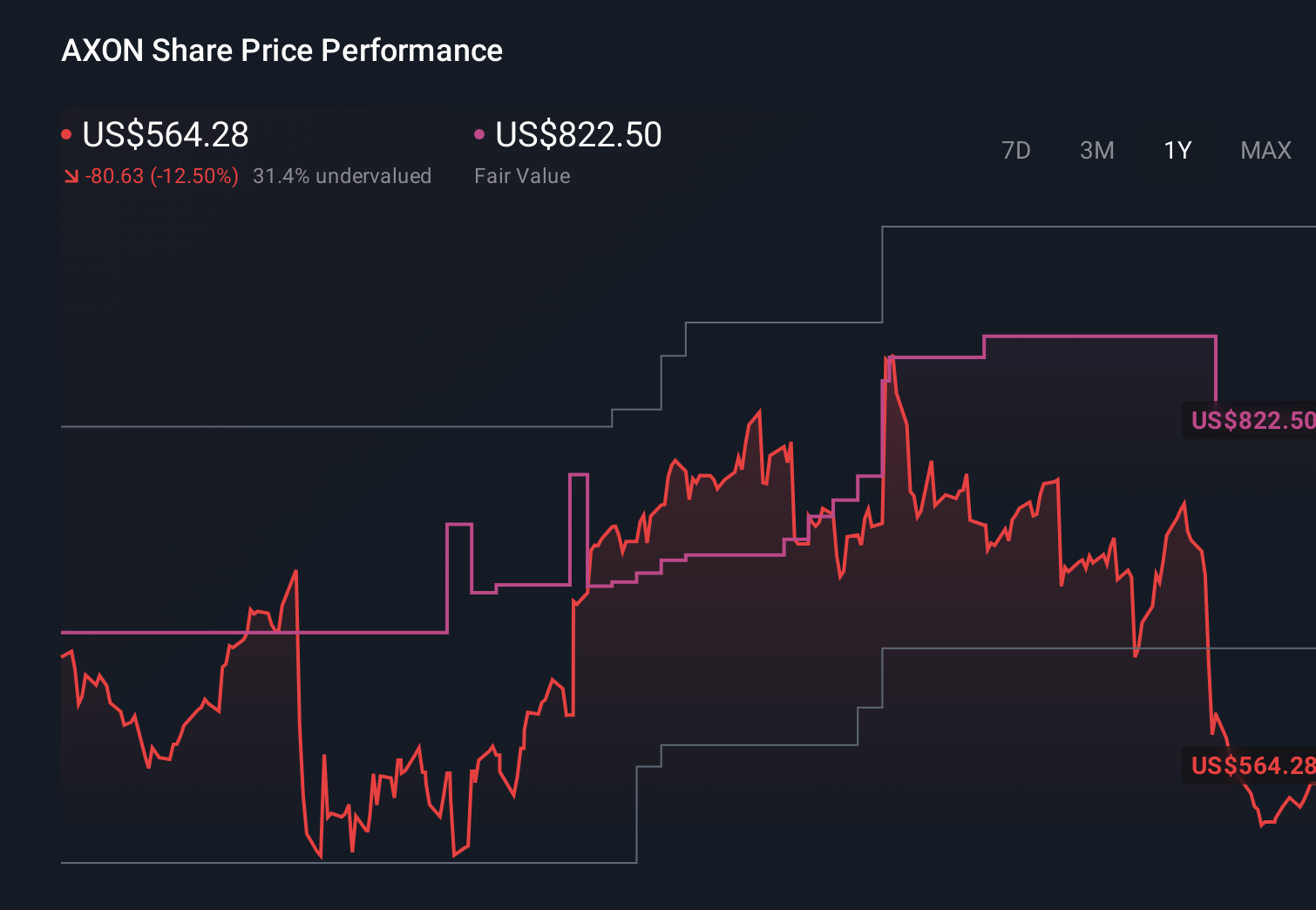

Axon Enterprise's narrative projects $6.0 billion revenue and $571.8 million earnings by 2029. This requires 29.6% yearly revenue growth and about a $447 million earnings increase from $124.7 million today.

Uncover how Axon Enterprise's forecasts yield a $707.96 fair value, a 82% upside to its current price.

Exploring Other Perspectives

While consensus sees a balanced risk and catalyst mix, the most optimistic analysts expect about US$4.5 billion revenue and US$641.9 million earnings by 2028, which shows how far views can differ and may shift again after Axon’s strong Q1 beat and higher 2026 guidance.

Explore 9 other fair value estimates on Axon Enterprise - why the stock might be worth over 2x more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Axon Enterprise research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Axon Enterprise research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Axon Enterprise's overall financial health at a glance.

Interested In Other Possibilities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

- Find 48 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.