Babcock & Wilcox (BW) Stock Valuation After TerraSpark Energy Campus Collaboration News

Babcock & Wilcox Enterprises Inc BW | 0.00 |

Babcock & Wilcox Enterprises (BW) is back in focus after announcing a planned collaboration with TerraSpark on the TerraSpark Energy Campus in West Virginia, a 1.6-gigawatt coal power and industrial project supported by a US$18.5 million federal grant.

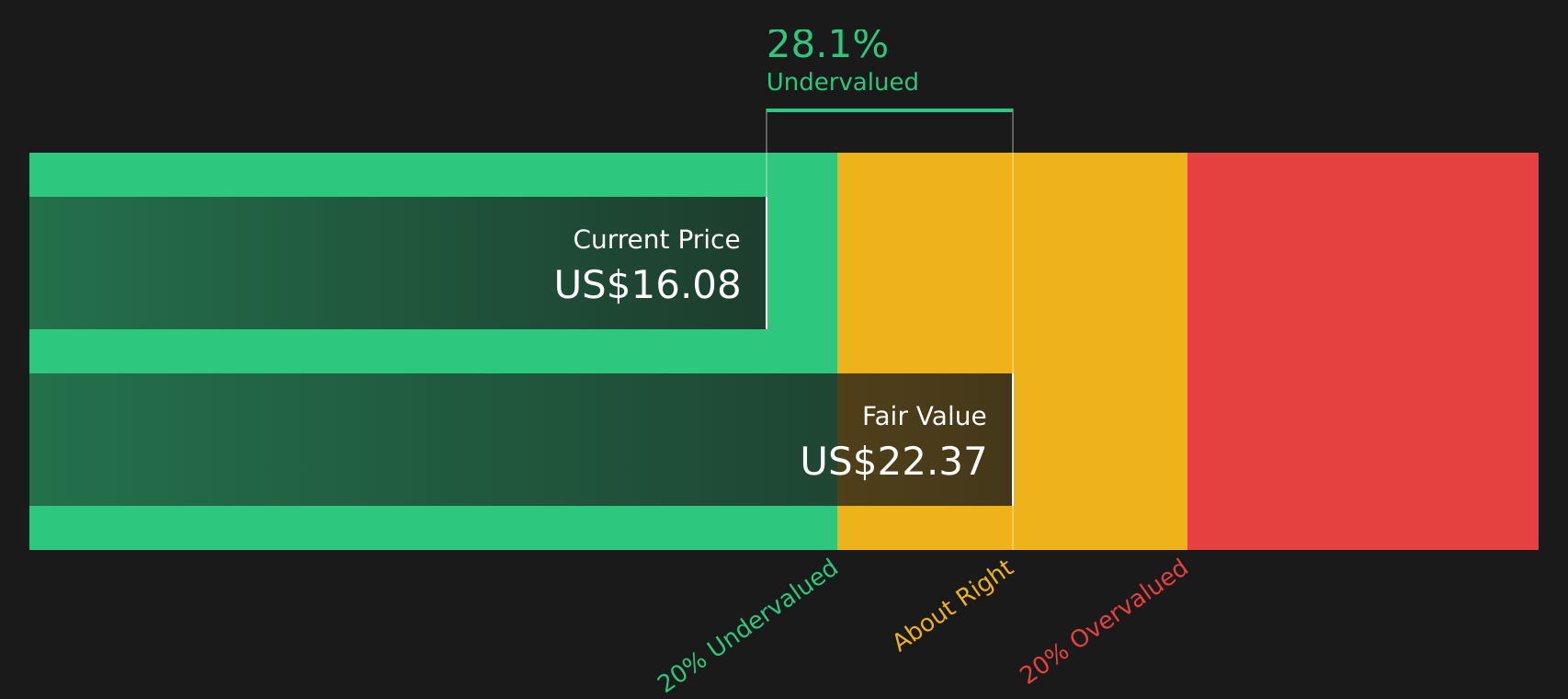

At a share price of US$16.08, BW has a 1-day share price return of 1.39%, after a 30-day share price decline of 16.90%. However, the 90-day share price return of 53.00% and a very large 1-year total shareholder return hint that momentum has been building over a longer horizon as investors weigh the TerraSpark collaboration and the recently declared preferred dividend.

If you are curious what other energy infrastructure stories are taking shape, this is a good time to scan 88 nuclear energy infrastructure stocks

With the stock up 53.00% over 90 days but still trading below one analyst price target and an estimated intrinsic value, the key question is whether this reflects a current mispricing or whether the market is already factoring in future growth.

Most Popular Narrative: 93% Overvalued

Against the narrative fair value of $8.33, the last close at $16.08 sits well above that estimate. This is where the story really starts.

The analysts have a consensus price target of $8.33 for Babcock & Wilcox Enterprises based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $10.0, and the most bearish reporting a price target of just $6.0.

Read the complete narrative. Read the complete narrative.

Want to know what is driving such a stretched valuation gap? The narrative leans on steady revenue growth, a sharp earnings swing and a premium profit multiple. Curious which assumptions have to line up to support that outcome? The full breakdown brings those pieces together.

Result: Fair Value of $8.33 (OVERVALUED)

However, there is still plenty that could trip this story up, from AI related power demand falling short to large projects slipping or landing on tougher terms.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View: Cash Flows Tell a Different Story

Analysts using multiples see BW as expensive, with a P/S of 3.7x versus 2.5x for the US Electrical industry. Yet our DCF model points the other way, with a future cash flow value of $22.42 per share versus today’s $16.08. Which lens do you trust more when growth and risk are both in play?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Babcock & Wilcox Enterprises for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such mixed signals on value, risk and reward, it makes sense to look under the hood yourself and move before sentiment shifts. To weigh the concerns against the potential upside in a structured way, start with the 3 key rewards and 3 important warning signs

Looking for more investment ideas?

If BW has your attention, do not stop here. The same tools can help you spot other opportunities before they hit everyone’s radar.

- Target stocks with strong fundamentals by scanning the solid balance sheet and fundamentals stocks screener (48 results), where balance sheets and core metrics are front and center.

- Hunt for potential mispricing by reviewing the 44 high quality undervalued stocks, which highlights companies with quality financials at comparatively modest prices.

- Focus on income potential by checking the 8 dividend fortresses, featuring companies with dividend yields from 5% and higher.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.