Ball (BALL) Could Be 15% Undervalued After Fresh Earnings Optimism

Ball Corporation BALL | 0.00 |

Recent commentary around Ball (BALL) focuses on its pattern of earnings surprises and a positive Earnings ESP, which has raised expectations for the upcoming report and drawn fresh attention to the stock.

Ball’s share price has eased in the very short term, with a 1-day share price return of 1.37% lower and a 7-day return of 3.51% lower. However, the 30-day share price return of 6.11% and year to date share price return of 13.33% suggest momentum has been building, even as the 1-year total shareholder return of 6.5% contrasts with a 5-year total shareholder return that is 23.53% lower.

If you are weighing Ball’s recent earnings interest against other opportunities, it could be a good moment to scan the market using our screener for 18 top founder-led companies

After Ball’s share price recovery and renewed interest around its earnings surprises, the real test now is whether the current valuation still offers enough upside for the risk being taken as a holder or new buyer.

Most Popular Narrative: 14.6% Undervalued

Ball's most followed narrative puts fair value at $70.79 versus the recent $60.46 share price, framing the current earnings interest inside a wider valuation gap.

The analysts have a consensus price target of $70.79 for Ball based on their expectations of its future earnings growth, profit margins and other risk factors.

However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $77.0, and the most bearish reporting a price target of just $60.0.

Read the complete narrative. Read the complete narrative.

The fair value hinges on steady revenue expansion, firmer margins, and a richer future earnings multiple. One core question sits underneath it all: how confidently do those assumptions stack up over time?

Result: Fair Value of $70.79 (UNDERVALUED)

However, there are still real swing factors for Ball, including customer concentration in South America and ongoing input cost volatility that could put pressure on margins and cash generation.

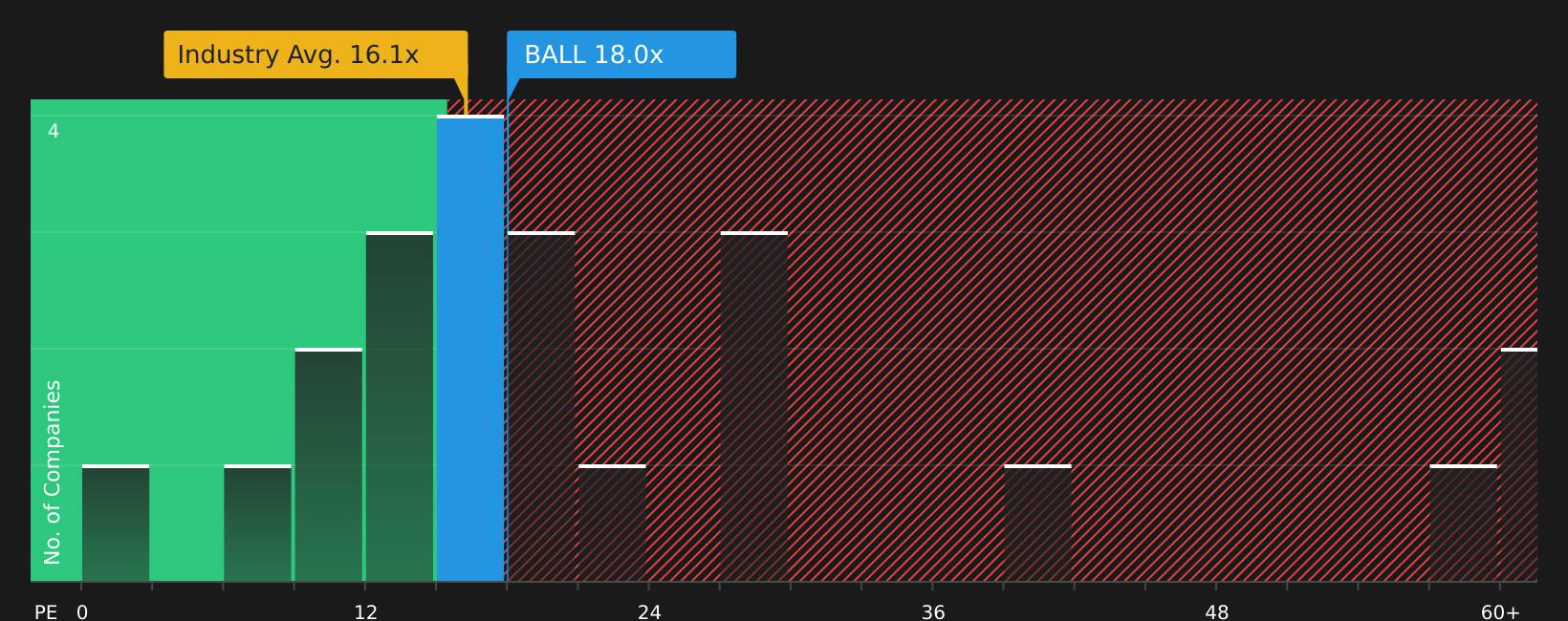

Another View: What Ball’s P/E Ratio Is Telling You

While the analyst fair value for Ball points to upside, the current P/E of 17.2x paints a more mixed picture. It sits above the global packaging industry at 15.6x, but below peers at 18.2x and the fair ratio estimate of 19.8x. This suggests some valuation tension rather than a clear bargain.

If you lean more on market based comparisons than cash flow models, it may be worth testing how comfortable you are with Ball trading between its industry multiple and that higher fair ratio. It may also be useful to consider what that gap could mean if sentiment shifts quickly for the stock. See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With mixed signals around Ball’s earnings momentum and valuation, now is a good time to look through the data yourself and decide how the risk and reward profile fits your portfolio. To see both the positives and the concerns flagged by our models, start with the 3 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Ball?

If Ball has your attention, do not stop there. Widening your watchlist with a few targeted stock ideas can sharpen your overall portfolio decisions.

- Spot potential mispricing early by scanning 44 high quality undervalued stocks that combine solid fundamentals with prices that may not fully reflect their underlying businesses.

- Strengthen your income stream by reviewing 8 dividend fortresses that offer higher yields while still aiming for resilience.

- Dial down portfolio stress by focusing on 79 resilient stocks with low risk scores that score well on financial stability and lower risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.