BancFirst (BANF) Gets A Zacks Upgrade, Is The Upside Already Priced In?

BancFirst Corporation BANF | 0.00 |

BancFirst (BANF) drew fresh investor attention after being upgraded to a Zacks Rank #2. This move is tied to higher earnings estimates that can quickly influence sentiment and short term trading interest.

At a latest share price of $114.96, BancFirst has delivered a 7.97% year to date share price return, while the 1-year total shareholder return is down 9.92%, set against a 3-year total shareholder return of 28.70% and a 5-year total shareholder return of 112.91%. This points to longer term gains but softer recent momentum as investors weigh the Zacks upgrade alongside earlier insider selling.

If this earnings driven move at BancFirst has your attention, it could be a good moment to broaden your search with a curated list of 19 top founder-led companies

BancFirst now sits closer to analysts’ targets after the Zacks upgrade and a solid long term return record. While recent insider selling lingers in the background, the key question is whether the current valuation still leaves enough upside for buyers?

Preferred P/E of 15.6x: Is it justified?

The latest data suggests BancFirst is priced on a P/E of 15.6x, which leaves the stock looking expensive compared to both its peers and the wider US banks sector.

The P/E multiple compares BancFirst's current share price with its earnings per share, giving a snapshot of how much investors are paying for each dollar of profit. For banks, it is a commonly used yardstick because earnings quality and return on equity often sit at the center of the investment case.

In this context, BancFirst combines some supportive fundamentals with a richer valuation. Earnings have grown 10.4% per year over the past 5 years, with the latest year at 11.4%, and net profit margins are reported at 35.4%, slightly higher than last year. The company is also described as having high quality earnings and a seasoned management team, alongside a 1.71% dividend yield and forecast earnings growth of 3.5% per year.

However, the current P/E of 15.6x stands above the estimated fair P/E of 12x, and above both the peer average multiple of 13.9x and the US banks industry average of 12.2x. That places BancFirst on a premium valuation compared to similar stocks, even though its 1 year share price performance has lagged both the broader US market and the banks sector.

Result: Price-to-earnings of 15.6x (OVERVALUED)

However, BancFirst's richer P/E and the question of whether recent insider selling signals caution could challenge the case for further upside if sentiment turns.

Another view on BancFirst’s value

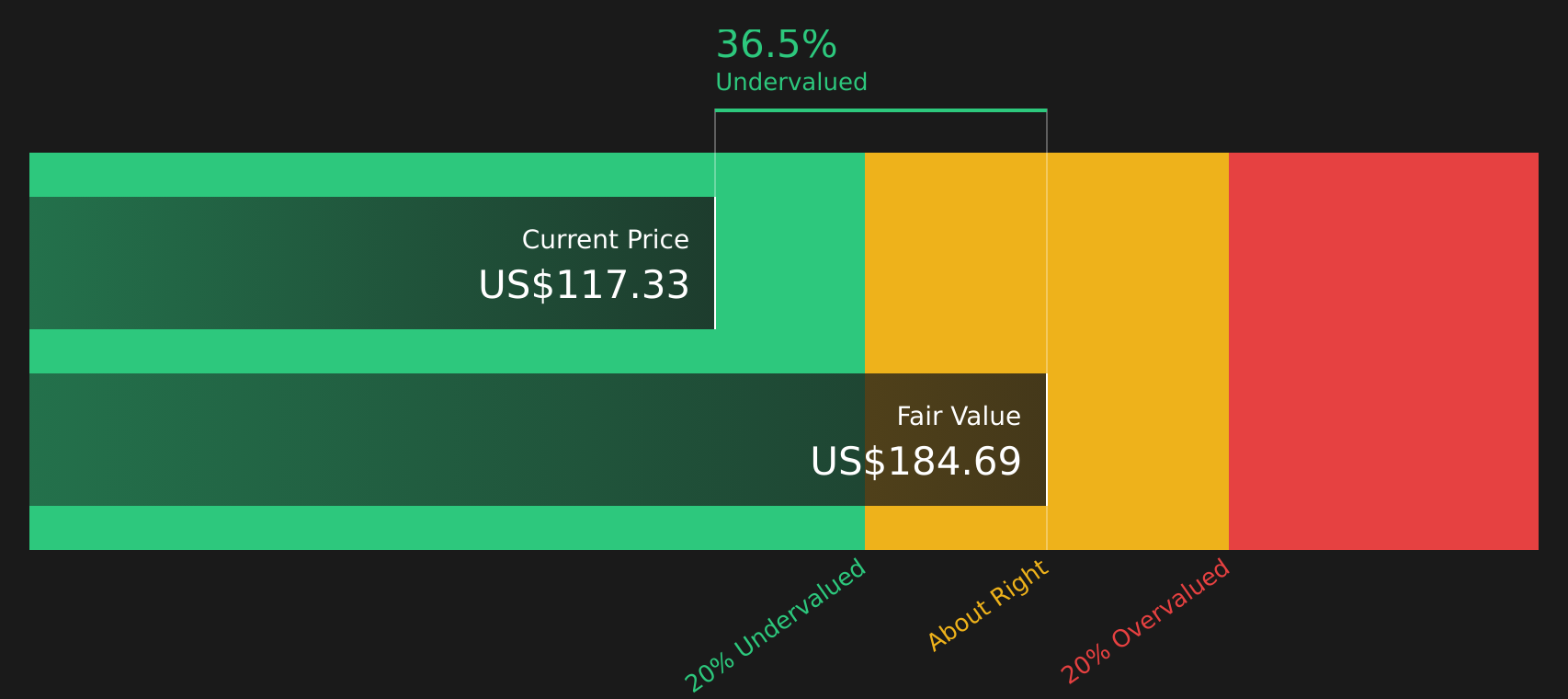

While the P/E ratio makes BancFirst look expensive, the SWS DCF model points the other way. With the stock at $114.96 and an estimated future cash flow value of $184.69, it is framed as trading about 38% below that fair value. Which signal should carry more weight for you?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out BancFirst for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Given the mixed signals around BancFirst's valuation, earnings, and recent returns, it makes sense to move quickly, review the underlying data, and judge the balance of risks and rewards for yourself. Start with the 4 key rewards and 1 important warning sign

Looking for more investment ideas beyond BancFirst?

If BancFirst has sharpened your focus on valuation and quality, do not stop here. Use structured screeners to spot other opportunities before the crowd.

- Target potential mispricings by scanning for companies that combine quality fundamentals with attractive valuations using the 45 high quality undervalued stocks.

- Strengthen your income stream by reviewing companies that offer higher yields and resilient payouts through the 9 dividend fortresses.

- Prioritize resilience and sleep a little easier at night by filtering for companies with sturdier finances via the solid balance sheet and fundamentals stocks screener (47 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.