Bandwidth (BAND) Is Up 26.9% After AI Optimism And Insider Sales - What's Changed

Bandwidth Inc. Class A BAND | 0.00 |

- In recent months, Bandwidth Inc. has attracted strong analyst enthusiasm for its AI-powered communications push and upgraded earnings outlook, while multiple executives and directors exercised Restricted Stock Units and sold portions of their Class A holdings around US$58–US$60 per share.

- This combination of bullish earnings revisions, momentum in AI voice agents, and insider transactions offers a revealing glimpse into how management and the market are responding to Bandwidth’s evolving position in cloud communications.

- We’ll now examine how the surge in analyst optimism around Bandwidth’s AI initiatives may reshape the company’s existing investment narrative.

We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Bandwidth Investment Narrative Recap

To own Bandwidth, you need to believe its AI-powered communications platform and Maestro orchestration can translate rising usage into durable, profitable growth, despite ongoing unprofitability and a rich valuation. The short term catalyst remains execution on AI voice agents and Salesforce Agentforce integration, while the biggest risk is that CPaaS pricing pressure and commoditization limit revenue quality. Recent insider selling around US$58–US$60 looks more like a response to the share price spike than a change to these drivers.

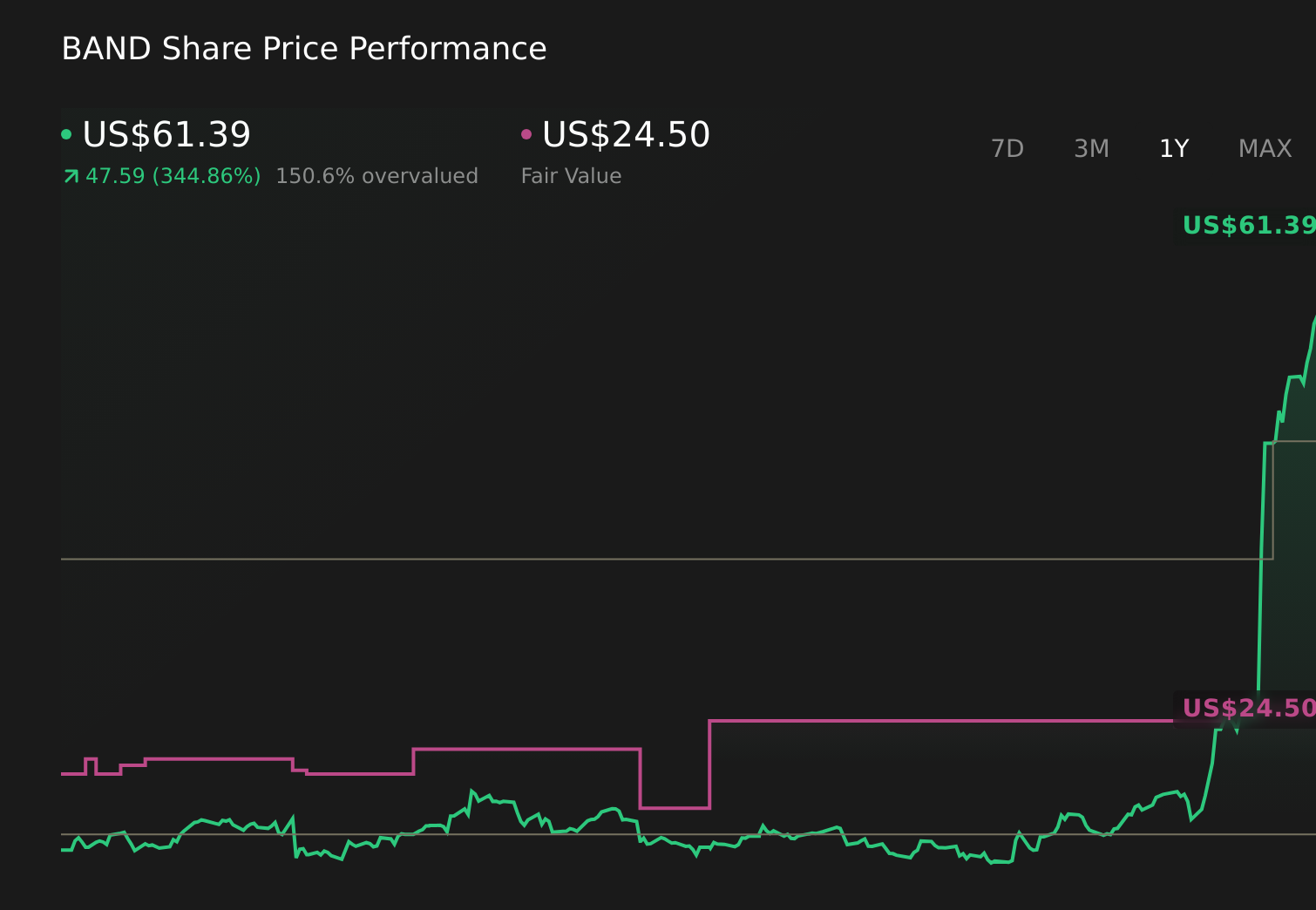

The most relevant recent development is the wave of insider equity activity following a roughly 390% one year share price surge and earnings upgrades. Executives including the CEO, CFO, COO, and other leaders exercised Restricted Stock Units and sold portions of their holdings, even as analysts gave Bandwidth an A+ EPS Revision Grade tied to its AI initiatives. For investors focused on catalysts, this pairing of bullish revisions with profit taking at multi-year highs raises important questions about...

Bandwidth’s narrative projects $987.7 million revenue and $17.8 million earnings by 2028. This requires 9.2% yearly revenue growth and a $27.8 million earnings increase from $-10.0 million today.

Uncover how Bandwidth's forecasts yield a $24.50 fair value, a 67% downside to its current price.

Exploring Other Perspectives

While consensus focuses on solid but moderate AI driven growth, the most optimistic analysts were already modelling about US$1.2 billion revenue and US$82.7 million earnings by 2029, so this new AI and insider activity could either reinforce or challenge that far more ambitious view, and it is worth considering how much confidence you personally place in such upside scenarios.

Explore 3 other fair value estimates on Bandwidth - why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Bandwidth research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Bandwidth research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bandwidth's overall financial health at a glance.

Contemplating Other Strategies?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 29 companies in the world exploring or producing it. Find the list for free.

- Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.