Bank First (BFC) Looks Fully Valued After Recent Gains And A 22x P E Multiple

Bank First Corp BFC | 0.00 |

Bank First stock reacts to recent performance trends

Bank First (BFC) has drawn attention after a recent pullback of around 1% in the latest session, even as the stock shows gains over the past week, month, and past 3 months.

The recent 1 day share price decline of 1.05% sits against a stronger backdrop, with the year to date share price return at 20.12% and the 1 year total shareholder return at 26.21%, suggesting momentum has been building rather than fading.

If you are comparing Bank First with other financial opportunities, it can help to widen the lens and scan 20 top founder-led companies

With Bank First reporting annual revenue of $193.62 million and net income of $72.903 million, alongside double digit revenue and earnings growth rates, the key question is whether the current share price still leaves room for value or if the market is already pricing in future growth.

Price-to-Earnings of 22.2x: Is it justified?

On current numbers, Bank First trades on a P/E of 22.2x at a last close of $144.90, which places the stock at a premium to several benchmarks.

The P/E ratio compares the current share price with the company’s earnings per share, so a higher P/E often reflects stronger growth expectations or a perception of quality. For a bank like Bank First, this ratio gives you a quick sense of how much investors are paying for each dollar of earnings compared with other banks.

Here, the 22.2x P/E stands well above the US Banks industry average of 12.2x, signaling that the market is paying materially more for Bank First’s earnings than for the sector as a whole. It also sits higher than a peer group average P/E of 15.5x and above an estimated fair P/E of 19.7x, a level the market could potentially move toward if expectations and pricing eventually align.

Result: Price-to-Earnings of 22.2x (OVERVALUED)

However, Bank First’s premium 22.2x P/E could come under pressure if revenue or net income growth slows, or if sentiment toward US regional banks weakens.

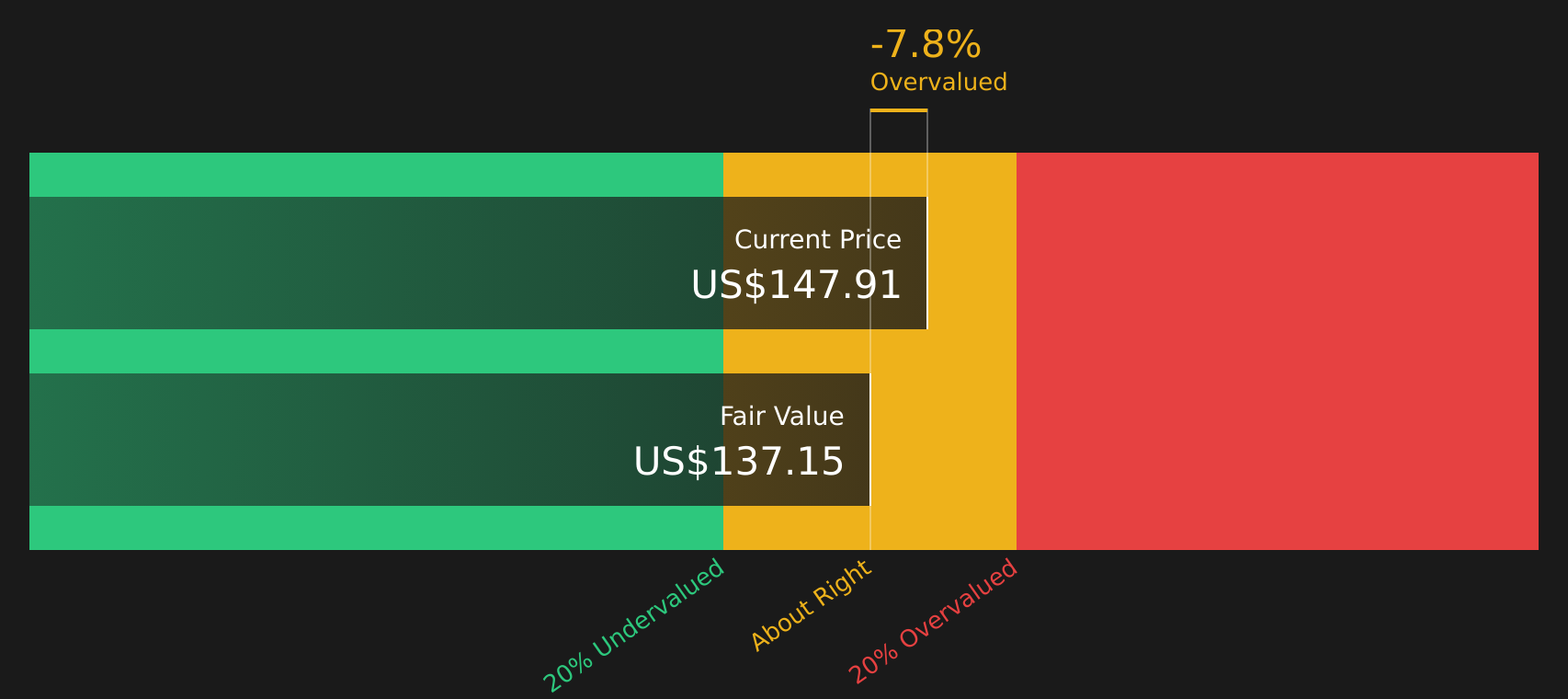

Another view on Bank First’s value

While the current 22.2x P/E suggests Bank First trades at a premium, the SWS DCF model points to a value of $137.15 per share, which is below the recent price of $144.90. On this measure, the stock screens as overvalued. Which signal should you pay more attention to?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Bank First for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 43 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Given the mixed signals on Bank First’s valuation, it helps to look past the headline ratios and inspect the details yourself. Our work highlights that the company has 1 or more potential rewards that investors are watching, so take a moment to review the 3 key rewards.

Looking for more investment ideas beyond Bank First?

If you are weighing Bank First against other opportunities, it makes sense to line it up against a few focused stock lists and see what stands out.

- Target steady potential by reviewing companies with strong payouts and resilient cash flows using the 9 dividend fortresses.

- Seek value by scanning for quality stocks that trade below what their fundamentals might justify through the 43 high quality undervalued stocks.

- Prioritize resilience by checking companies with robust finances and solid fundamentals via the solid balance sheet and fundamentals stocks screener (48 results).

Skip waiting for the next headline and start comparing these curated stock ideas now so you do not miss opportunities that fit your goals and risk comfort.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.