Bank Of America (BAC) Launches New Premium Card With Alaska Airlines' Loyalty Program

Bank of America Corp BAC | 49.38 | +0.22% |

Alaska Airlines recently launched its enhanced Atmos Rewards loyalty program, co-branded with Bank of America (BAC), reflecting a strong partnership aimed at enticing global travelers. Over the last quarter, Bank of America's share price appreciated by 12%, aligned with a positive earnings report that showed increased net interest income and net income. Additionally, the bank's announcement of an increased dividend and a sizeable buyback program supported investor confidence. Even as the broader S&P 500 experienced declines during Powell's anticipated speech, BAC's actions during this period provided stability, bolstering its price performance.

Alaska Airlines' new Atmos Rewards program, in collaboration with Bank of America, is expected to enhance customer acquisition, potentially boosting both companies' revenue streams. For Bank of America, this partnership might strengthen digital engagement efforts, aligning with its strategic focus on AI-driven efficiencies and a diversified credit portfolio. Over the past five years, Bank of America's total return, including share price and dividends, was 113.96%. This reflects substantial growth, particularly compared to the broader market, which returned 14.4% over the past year. Notably, the US Banks industry saw a similar performance of 24.4% over the same period.

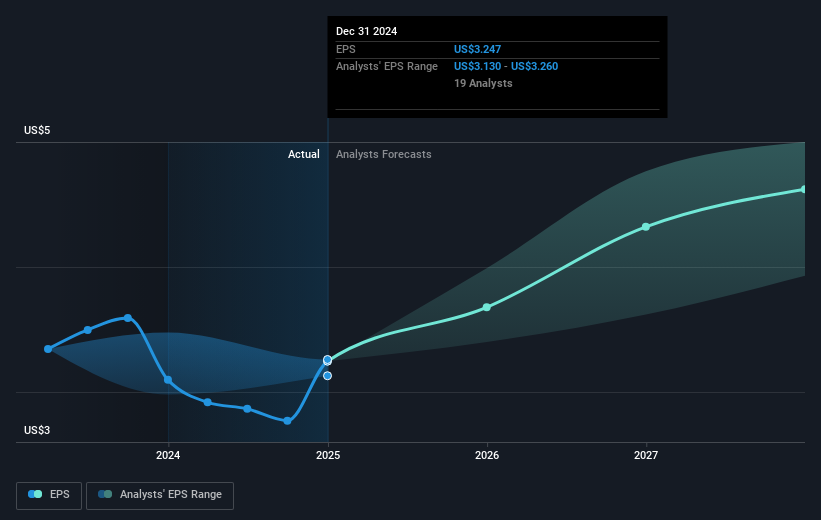

The recent news ties into forecasted revenue enhancements, with analysts predicting growth of 7.5% per year as the company leverages digital and AI investments. Earnings are expected to rise from US$26.59 billion to around US$32.9 billion by 2028. These projections support a consensus price target of US$53.08, currently about 9.79% higher than the present share price of US$48.35. The proactive steps to engage customers through high-value programs like Atmos Rewards could contribute positively to hitting these targets, aligning with expected earnings per share growth of US$4.73.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.