Before Aramco's Q2 Earnings Report Tomorrow: The Key Forecasts and Analyst Ratings You Need to See — Up to 36% Upside

SAUDI ARAMCO 2222.SA | 27.40 | +0.44% |

Tadawul All Shares Index TASI.SA | 11249.54 | +0.74% |

Energy TENI.SA | 5221.89 | +0.48% |

Saudi Arabian Oil Co.(2222.SA), the world's largest integrated oil and gas company, is set to announce its second-quarter 2025 financial results tomorrow. Market consensus, based on data compiled by Bloomberg, points towards a sequential and year-over-year decline in earnings, primarily driven by softer crude oil prices during the period.

However, investors will be closely watching the performance of the downstream segment and production volumes, which are expected to provide a partial buffer against the weaker price environment.

Here is a one-glance summary of the key consensus forecasts for the upcoming Q2 results, along with analyst ratings.

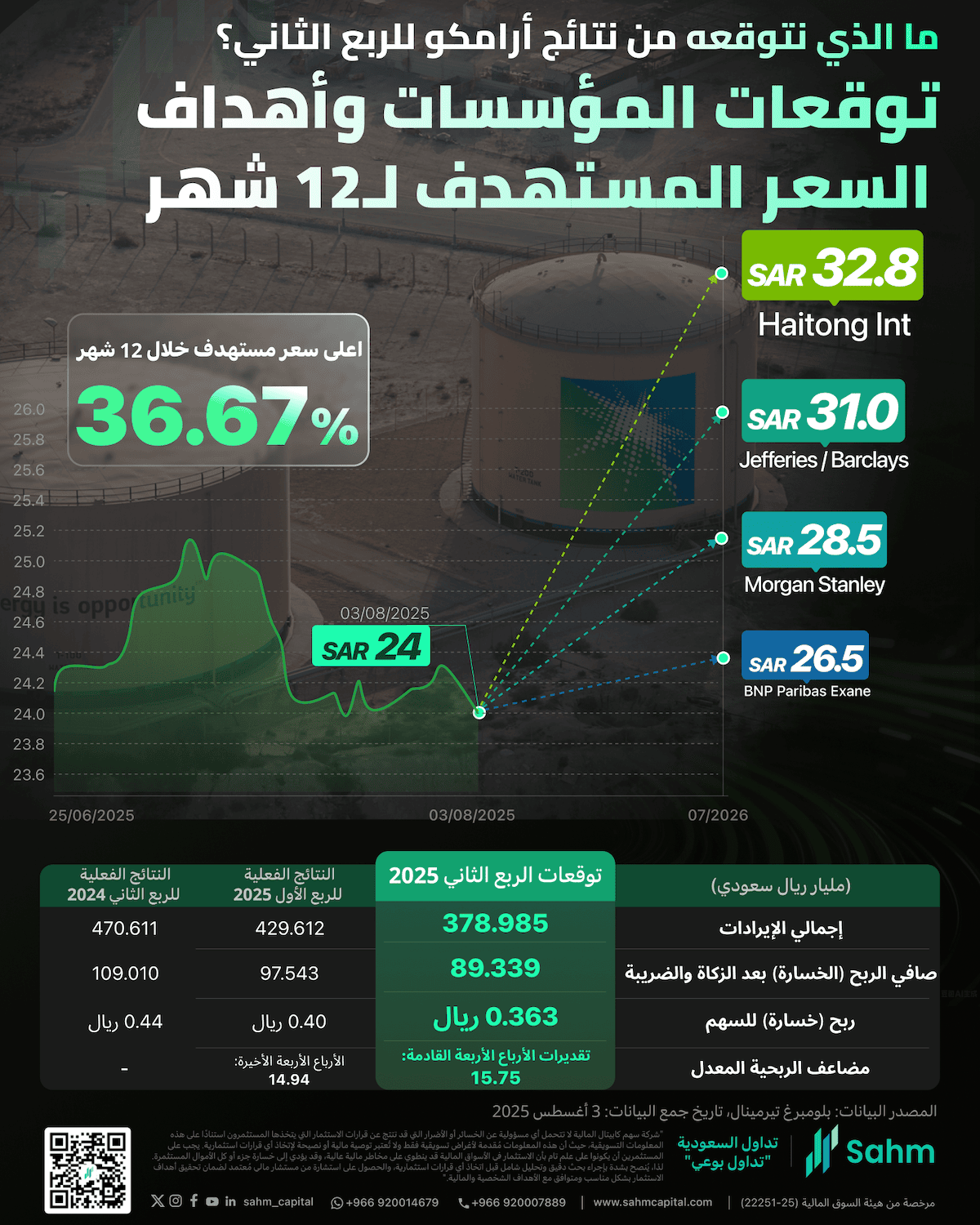

Aramco Q2 2025: At a Glance

Key Analyst Forecasts for Q2 2025 (as of 06/30/2025):

- Total Revenue: SAR 378.98 billion

- Net Income: SAR 89.34 billion

- Earnings Per Share (EPS): SAR 0.363

Q1 2025 Actuals (for comparison):

- Total Revenue: SAR 429.61 billion

- Net Income: SAR 97.54 billion

- Earnings Per Share (EPS): SAR 0.40

Analyst Ratings

Heading into the earnings announcement, analyst sentiment on Saudi Arabian Oil Co.(2222.SA) is balanced. While many advise a neutral or "Hold" stance, reflecting caution around the current oil price environment, a significant number of firms maintain a positive outlook, pointing to the company's long-term strengths.

Here’s a snapshot of recent recommendations from key financial institutions:

- Positive Outlook (Buy/Overweight): Several major banks see upside potential.

- Barclays and Jefferies both rate the stock as 'Overweight' with a price target of SAR 31.00.

- JP Morgan also has an 'Overweight' rating, targeting SAR 28.00.

- Haitong International is among the most bullish with an 'Outperform' rating and the highest price target in this group at SAR 32.80.

- Local firm BSF Capital also maintains a 'Buy' rating with a target of SAR 30.00.

- Neutral Stance (Hold/Neutral): Another group of analysts suggests a more cautious "wait-and-see" approach.

- Citi and BNP Paribas both assign a 'Neutral' rating, with price targets of SAR 25.50 and SAR 26.50, respectively.

- Morningstar recommends 'Hold' with a target of SAR 25.00.

- Morgan Stanley advises an 'Equal-weight/Cautious' position, targeting SAR 28.50.

Key Takeaway: The range of 12-month price targets from these analysts spans from SAR 25.00 to SAR 32.80. This spread highlights the differing views on short-term headwinds versus the company's robust long-term fundamentals and operational advantages.

Analysis: A Tale of Two Segments

Upstream Facing Headwinds

The primary factor expected to weigh on Aramco's Q2 performance is the decline in average crude oil prices. Brent crude experienced downward pressure during the quarter, influenced by factors including macroeconomic uncertainty and production dynamics. This price weakness is anticipated to directly impact the profitability of Aramco's core upstream (exploration and production) business.

While lower prices present a challenge, analysts note that this could be partly offset by higher production volumes from the company during the same period.

Downstream to Provide a Buffer

In contrast to the upstream segment, Aramco's downstream business (refining and chemicals) is expected to show improved performance. Analysts anticipate that refining margins strengthened during the second quarter, which should benefit the profitability of this segment. This highlights the strategic advantage of Aramco's integrated model, where a robust downstream operation can help cushion the impact of volatility in the upstream market.

The Long-Term View

Despite the short-term pressure on earnings, some analysts maintain a constructive long-term outlook. Ahmed Hazem Maher from EFG Hermes recently commented, "Now is a good time to buy Saudi Arabian Oil Co.(2222.SA) – Gulf oil has the lowest greenhouse gas emissions, with Aramco having vast reserves and the lowest extraction costs." This perspective underscores the company's fundamental strengths and competitive advantages in the global energy landscape.

Risks to Monitor

Moving forward, investors should keep an eye on several key risks that could influence Aramco's performance:

- Oil Price Volatility: Further-than-expected declines in oil prices remain the most significant risk to earnings.

- Downstream Margins: A potential squeeze on downstream profitability if refining spreads narrow.

- Geopolitical Factors: Any geopolitical disruptions that could alter global energy supply and demand patterns.

Ultimately, the Q2 results and the accompanying management commentary will be crucial for investors to gauge the outlook for the remainder of 2025. The focus will be on how effectively the company navigates the current price environment and leverages its integrated operations.