Beyond Meat, Inc.'s (NASDAQ:BYND) 30% Share Price Plunge Could Signal Some Risk

Beyond Meat BYND | 0.75 0.75 | +4.35% +0.15% Pre |

To the annoyance of some shareholders, Beyond Meat, Inc. (NASDAQ:BYND) shares are down a considerable 30% in the last month, which continues a horrid run for the company. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 81% loss during that time.

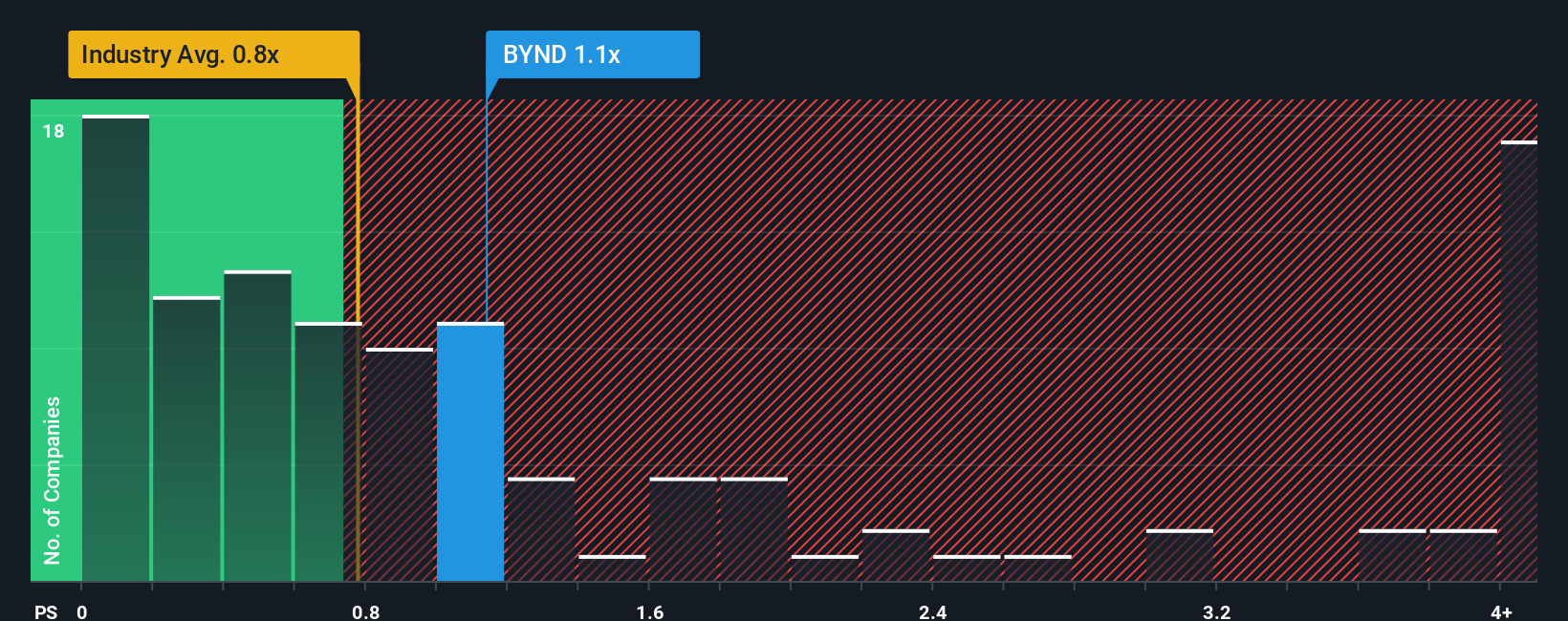

Even after such a large drop in price, it's still not a stretch to say that Beyond Meat's price-to-sales (or "P/S") ratio of 1.1x right now seems quite "middle-of-the-road" compared to the Food industry in the United States, where the median P/S ratio is around 0.8x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

What Does Beyond Meat's Recent Performance Look Like?

While the industry has experienced revenue growth lately, Beyond Meat's revenue has gone into reverse gear, which is not great. It might be that many expect the dour revenue performance to strengthen positively, which has kept the P/S from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Beyond Meat.How Is Beyond Meat's Revenue Growth Trending?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Beyond Meat's to be considered reasonable.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 10%. As a result, revenue from three years ago have also fallen 34% overall. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Turning to the outlook, the next three years should bring diminished returns, with revenue decreasing 0.8% per annum as estimated by the six analysts watching the company. Meanwhile, the broader industry is forecast to expand by 3.1% per annum, which paints a poor picture.

In light of this, it's somewhat alarming that Beyond Meat's P/S sits in line with the majority of other companies. Apparently many investors in the company reject the analyst cohort's pessimism and aren't willing to let go of their stock right now. Only the boldest would assume these prices are sustainable as these declining revenues are likely to weigh on the share price eventually.

The Bottom Line On Beyond Meat's P/S

With its share price dropping off a cliff, the P/S for Beyond Meat looks to be in line with the rest of the Food industry. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Our check of Beyond Meat's analyst forecasts revealed that its outlook for shrinking revenue isn't bringing down its P/S as much as we would have predicted. When we see a gloomy outlook like this, our immediate thoughts are that the share price is at risk of declining, negatively impacting P/S. If the poor revenue outlook tells us one thing, it's that these current price levels could be unsustainable.

Don't forget that there may be other risks.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.