Bioventus (BVS) Heads To An Investor Conference, Is It Still Below Fair Value?

Bioventus, Inc. Class A BVS | 0.00 |

Bioventus (BVS) is back in the spotlight as company leaders prepare to speak at the 26th Annual New Ideas Summer Investor Conference, giving investors fresh context for the stock’s recent performance.

That upcoming conference appearance comes after a strong run in Bioventus, with the stock posting a 30 day share price return of 32.83% and a year to date share price return of 69.49%. The 3 year total shareholder return of 231.17% points to momentum that has been building over a longer horizon.

If Bioventus’s recent move has you watching the healthcare space more closely, it could be a good moment to scan other fast changing areas such as 40 healthcare AI stocks

For Bioventus, that sharp share price swing sits between two readings: one where investors are simply re-rating the story on sentiment, and another where earnings and cash flows are doing more of the heavy lifting. So how does today’s valuation stack up?

Most Popular Narrative: 17.4% Undervalued

On the most followed fair value view, Bioventus at a last close of $12.22 is priced below an implied $14.80 narrative estimate, which is built off detailed growth and margin assumptions rather than recent share price momentum alone.

The company's consistent expansion and diversification of its product portfolio, including double-digit growth in the high-margin ultrasonics surgical business and accelerated growth in Exogen restorative therapies, broadens its participation in multiple high-growth therapeutic areas, mitigating revenue concentration risk and supporting sustainable, long-term revenue and margin expansion.

Want to see what is powering that $14.80 figure for Bioventus? The core of this narrative is a carefully layered mix of revenue growth, margin uplift and a richer future earnings multiple. Curious how those moving parts fit together, and what kind of profitability path is baked into that story? The full narrative lays out the numbers behind that view in black and white.

Result: Fair Value of $14.80 (UNDERVALUED)

However, Bioventus still has a few pressure points to watch, including its reported US$341 million debt load and reliance on key products like Durolane and Exogen.

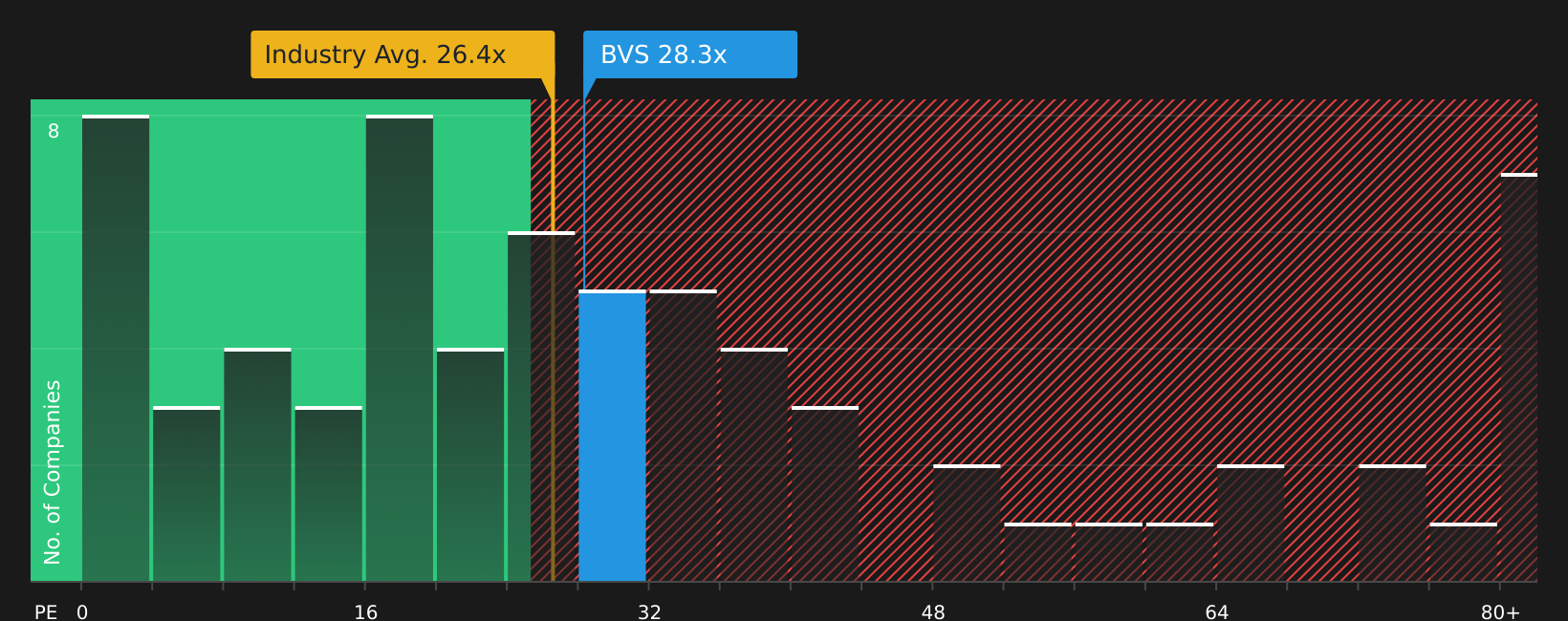

Another View: What Bioventus’s P/E Ratio Is Signaling

While the fair value narrative suggests Bioventus is 17.4% undervalued at $12.22 versus a $14.80 estimate, the current P/E of 29.1x paints a different picture. It sits above the US Medical Equipment industry at 26.3x and the fair ratio of 24.8x, which points to a valuation that already bakes in plenty of optimism. If sentiment cools, the share price could move back toward that lower fair ratio instead.

For a closer look at how this earnings multiple stacks up against peers and what that gap might mean for valuation risk, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With Bioventus presenting a mix of potential rewards and clear risks, do not just rely on headlines. Move quickly to review the figures and context, then weigh the 4 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Bioventus?

If Bioventus has sharpened your focus, do not stop here. Use Simply Wall Street’s screener to compare fresh ideas, spot patterns, and pressure test your watchlist.

- Target potential turnarounds by scanning 20 elite penny stocks with strong financials that pair lower share prices with stronger fundamentals than you might expect at first glance.

- Zero in on quality at a measured price by working through the 44 high quality undervalued stocks that balance earnings power with more conservative valuations.

- Prioritize resilience by reviewing the 73 resilient stocks with low risk scores where financial strength and steadier risk profiles take center stage.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.