Blackstone (BX): Evaluating Valuation After $1.2 Billion Wolf Summit Energy Power Plant Announcement

Blackstone Inc. BX | 113.05 | -1.12% |

Blackstone (NYSE:BX) is making waves with a $1.2 billion commitment to build the Wolf Summit Energy power facility in West Virginia. This move signals a focused push into energy infrastructure, specifically tailored for growing AI-driven demand across the region.

Blackstone’s ambitious energy bet comes after a busy few weeks, with recent headlines including a prominent European leadership hire and interest in next-generation digital infrastructure. Even so, the short-term share price return has been soft, falling nearly 19% year-to-date, and total shareholder return over the past year stands at -20%. That said, investors with a longer horizon have still seen tremendous gains, with a three-year total shareholder return of 72% and 184% over five years. This suggests there is still momentum for those looking beyond recent volatility.

If Blackstone’s infrastructure moves have you wondering what else is out there, this could be the perfect time to discover fast growing stocks with high insider ownership.

With Blackstone’s stock trading at a nearly 27% discount to consensus analyst price targets, the question for investors now is whether recent developments unlock more value or if future growth is already reflected in the price.

Most Popular Narrative: 21.3% Undervalued

Blackstone's widely followed narrative assigns a fair value notably higher than the last close of $141.44, hinting at significant upside from current levels. This sets the stage for a closer look at the logic behind this bullish assessment.

Blackstone is positioned for strong future growth with high inflows and substantial capital for opportunistic investments in undervalued assets. Strategic alliances and innovations in private credit and wealth management aim to boost revenue through expanded market reach and larger spreads.

Behind this eye-catching target are unusually optimistic assumptions for revenue expansion, earnings power, and margin gains, fueled by a playbook of diversification and capital allocation moves you will not want to miss. Find out how Blackstone’s growth ambitions and profit forecasts shape this valuation narrative.

Result: Fair Value of $179.78 (UNDERVALUED)

However, trade policy uncertainty and higher construction costs could challenge Blackstone’s real estate values and earnings outlook in the coming quarters.

Another View: High Multiples Raise Questions

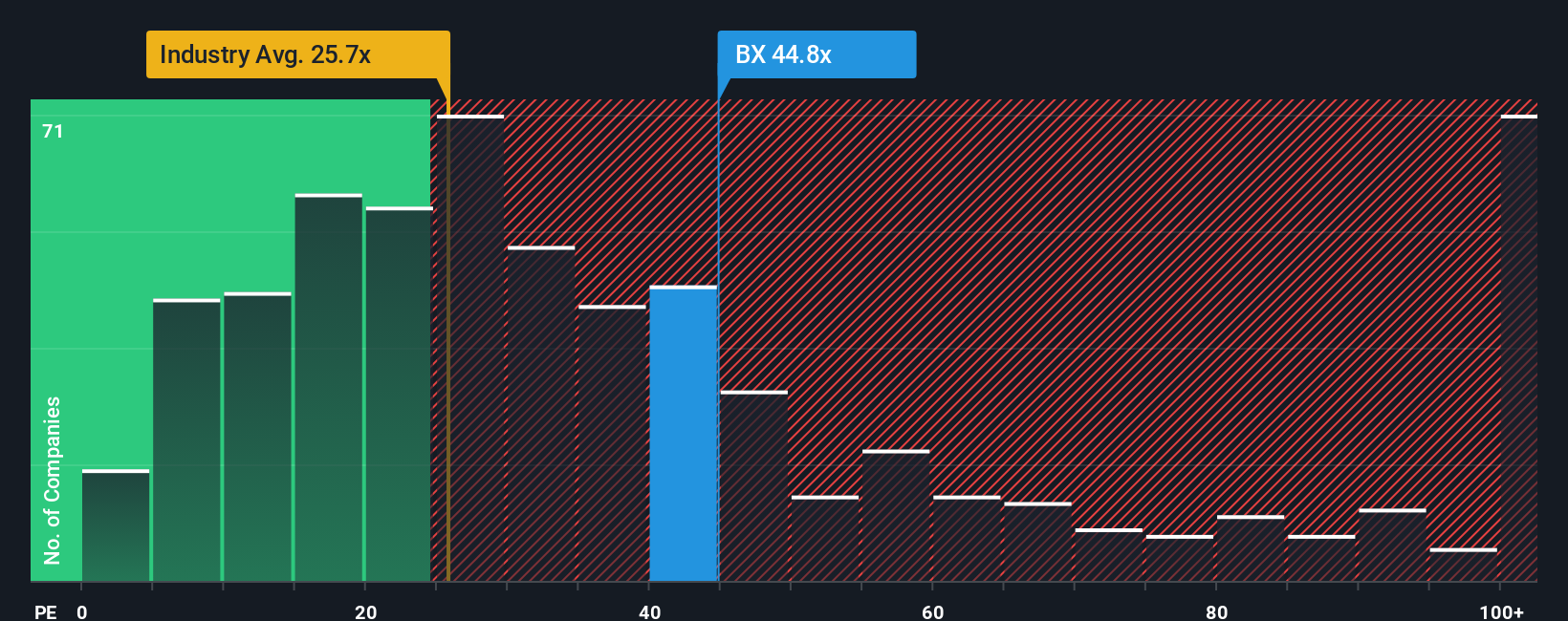

While the popular narrative sees Blackstone as undervalued, a closer look at traditional price-to-earnings ratios tells a different story. Blackstone trades at 40.9x earnings, which is not only higher than the US Capital Markets industry average of 24.9x but also above its peer group’s 35.2x and well above the fair ratio of 25.5x that the market could revert towards. This gap signals that current optimism comes with valuation risk. Could further stock gains be limited if multiples come down?

Build Your Own Blackstone Narrative

If you think there is a different story to tell or want to dig into the numbers on your own, you can build your own perspective in just a few minutes. Start with Do it your way.

A great starting point for your Blackstone research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investment opportunities do not wait around. Use these top screens to find your edge before everyone else. Your next winner could be one click away.

- Unlock the potential of forward-thinking healthcare by checking out these 31 healthcare AI stocks, where AI innovation is transforming patient outcomes and creating lasting value.

- Jump into a field where consistency and cash flow matter most, with these 16 dividend stocks with yields > 3% offering yields above 3% for reliable income growth.

- Catch trends ahead of the crowd and position yourself in tomorrow’s technology wave by bold moves in these 26 AI penny stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.