Blackstone Mortgage Trust Q3 Revenue Rebound Challenges Bearish Narratives On Earnings Resilience

Blackstone Mortgage Trust, Inc. Class A BXMT | 0.00 |

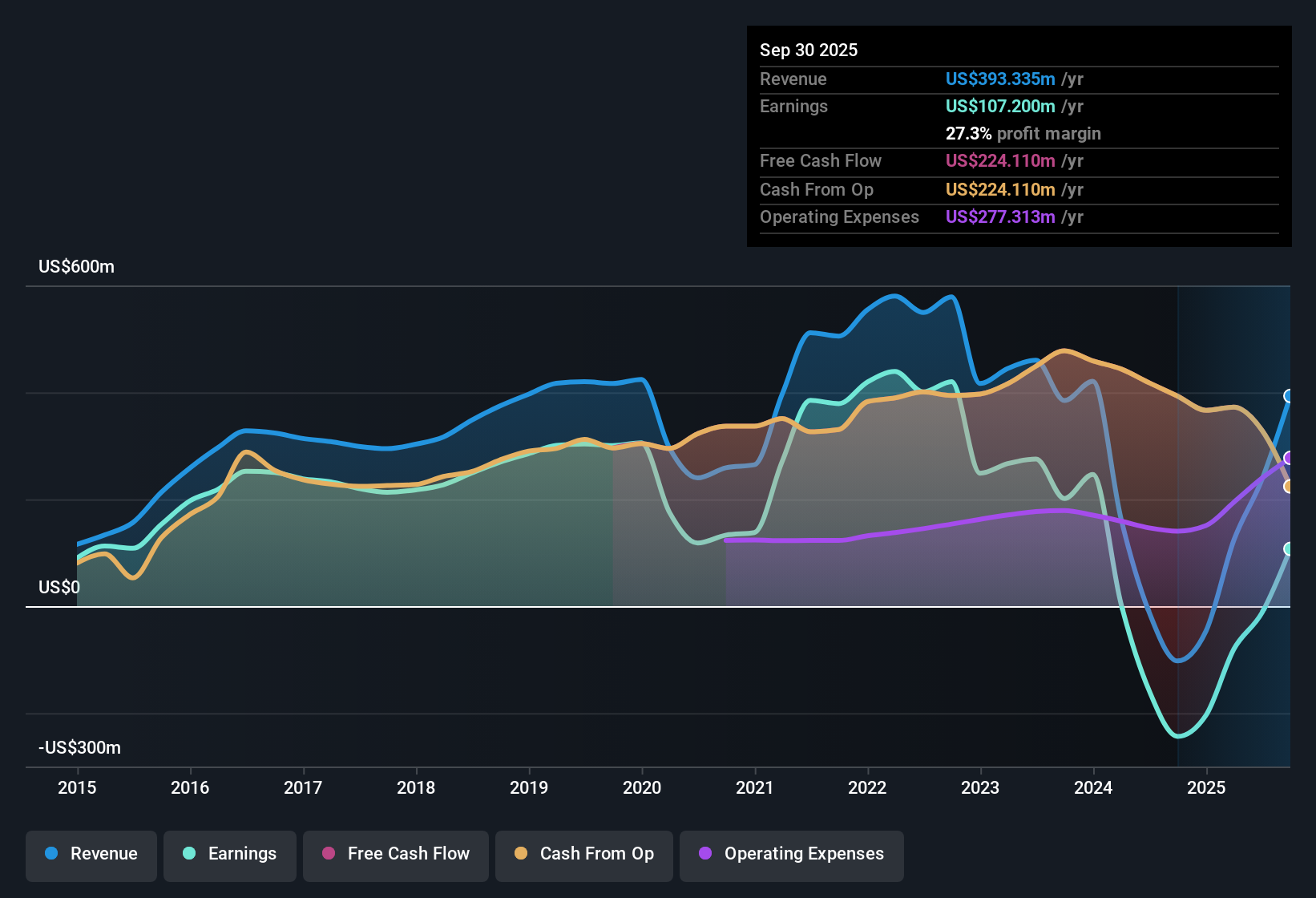

Blackstone Mortgage Trust (BXMT) just posted its latest FY 2025 numbers with Q3 revenue at US$133.6 million and basic EPS of US$0.37, setting a clearer picture of how the year is shaping up. The company has seen quarterly revenue move from US$77.4 million in Q1 2025 to US$88.0 million in Q2 and then to US$133.6 million in Q3, while EPS has shifted from US$0.00 in Q1 to US$0.04 in Q2 and then to US$0.37 in Q3. This gives investors a clean set of figures to judge the current margin profile and assess how resilient the earnings engine looks.

See our full analysis for Blackstone Mortgage Trust.With the headline numbers on the table, the next step is to see how this earnings run lines up against the key stories investors tend to focus on for BXMT and where those narratives might need an update.

Profitability returns after deep five year slide

- On a trailing 12 month basis, BXMT moved from a loss of US$243.7 million in Q3 2024 to profit of US$107.2 million by Q3 2025, even though the same period is described as having seen earnings fall at an annualized rate of 44.7% over the past five years.

- Analysts' consensus view links this recent return to profit with portfolio turnover and balance sheet work, but also flags tension with the longer term decline in earnings:

- The consensus highlights efforts to recycle capital from impaired or repaid loans into higher quality opportunities, which lines up with the shift from multi quarter losses to positive net income in the latest trailing 12 months.

- At the same time, the five year 44.7% annualized earnings decline keeps the narrative grounded, because it shows that one year of profit does not erase the longer trend that analysts are still factoring into their expectations.

The consensus narrative notes that the recent move back into the black is only one piece of a longer story that still includes several years of earnings pressure, so it is worth reading how they connect those dots in the full write up. 📊 Read the full Blackstone Mortgage Trust Consensus Narrative.

Premium 31.6x P/E with modest growth forecasts

- BXMT trades on a trailing P/E of 31.6x compared with an industry average of about 12x and a peer average of about 15.6x, while earnings and revenue are forecast to grow by 4.4% and 1.6% per year respectively.

- What is interesting for the bearish narrative is how this high multiple sits next to the growth and risk profile analysts describe:

- Bears point out that paying 31.6x earnings for 4.4% forecast earnings growth and 1.6% forecast revenue growth leaves little room for disappointment, especially when revenue growth is below the 10.4% forecast for the wider US market.

- Critics also connect the premium P/E to balance sheet and coverage questions, arguing that a stock with debt not well covered by operating cash flow and dividends not well covered by earnings might normally trade nearer the 12x industry level rather than at roughly double that.

Skeptics warn that a 31.6x P/E and modest growth expectations set a high bar, so they pay close attention to the detailed bear case before committing fresh capital. 🐻 Blackstone Mortgage Trust Bear Case

9.4% dividend with weak coverage and impaired loans

- The stock carries a 9.4% dividend yield, yet that payout is described as not well covered by either earnings or free cash flow, and there is US$970 million of impaired loans that still incur interest expense without contributing income.

- Supporters of the more bullish elements in the consensus narrative lean on capital redeployment and a net lease strategy to offset these pressures, but the numbers show why this is a work in progress:

- The consensus text points to US$1.5 billion of impaired assets already addressed in six months and expects further resolutions to free up capital, yet the remaining US$970 million of impaired loans continues to weigh on net margins until it is worked through.

- Income focused investors might be drawn to the 9.4% yield, but the commentary that dividends and debt are not well covered by operating cash flow underlines why analysts are watching how quickly repayments and new investments can support that payout.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Blackstone Mortgage Trust on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? If this data points you in another direction, shape your own view in a few minutes and Do it your way

A great starting point for your Blackstone Mortgage Trust research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

See What Else Is Out There

BXMT carries a premium 31.6x P/E, a 9.4% yield with weak coverage, and impaired loans that keep pressure on earnings quality and balance sheet strength.

If those balance sheet questions and fragile coverage metrics make you cautious, compare this profile with solid balance sheet and fundamentals stocks screener (45 results) and see how quickly stronger names can change your watchlist priorities.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.