Booz Allen Hamilton (BAH) Stock After 25% Slide What Do Valuation Models Suggest Now

Booz Allen Hamilton Holding Corporation Class A BAH | 0.00 |

- Wondering if Booz Allen Hamilton Holding stock now looks attractive on price, or if the recent weakness is a warning sign? This article focuses squarely on what the current valuation is really telling you.

- The share price last closed at US$74.55, with returns declining 5.9% over the past week, edging up 2.6% over the past month, but falling 12.2% year to date and 25.1% over the last year.

- Recent market attention on Booz Allen Hamilton Holding has been shaped by ongoing contract work with government and commercial clients and by investor reassessments of risk in the Professional Services sector. These factors help explain why the stock has seen periods of pressure alongside pockets of renewed interest.

- On Simply Wall St's valuation checks, Booz Allen Hamilton Holding has a value score of 5/6. This sets the stage for a closer look at how different valuation methods line up today and how an even richer way of thinking about valuation comes together at the end of this article.

Approach 1: Booz Allen Hamilton Holding Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what Booz Allen Hamilton Holding stock might be worth by projecting future cash flows and discounting them back to today’s dollars. It focuses on the cash the company could return to shareholders rather than short term price moves.

For Booz Allen Hamilton Holding, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections. The latest twelve month Free Cash Flow is about $956.5 million, and analysts plus Simply Wall St projections have annual Free Cash Flow figures such as $878.9 million in 2026 and $979.1 million in 2029. Longer term estimates out to 2035 are extrapolated from these inputs rather than based on formal analyst coverage.

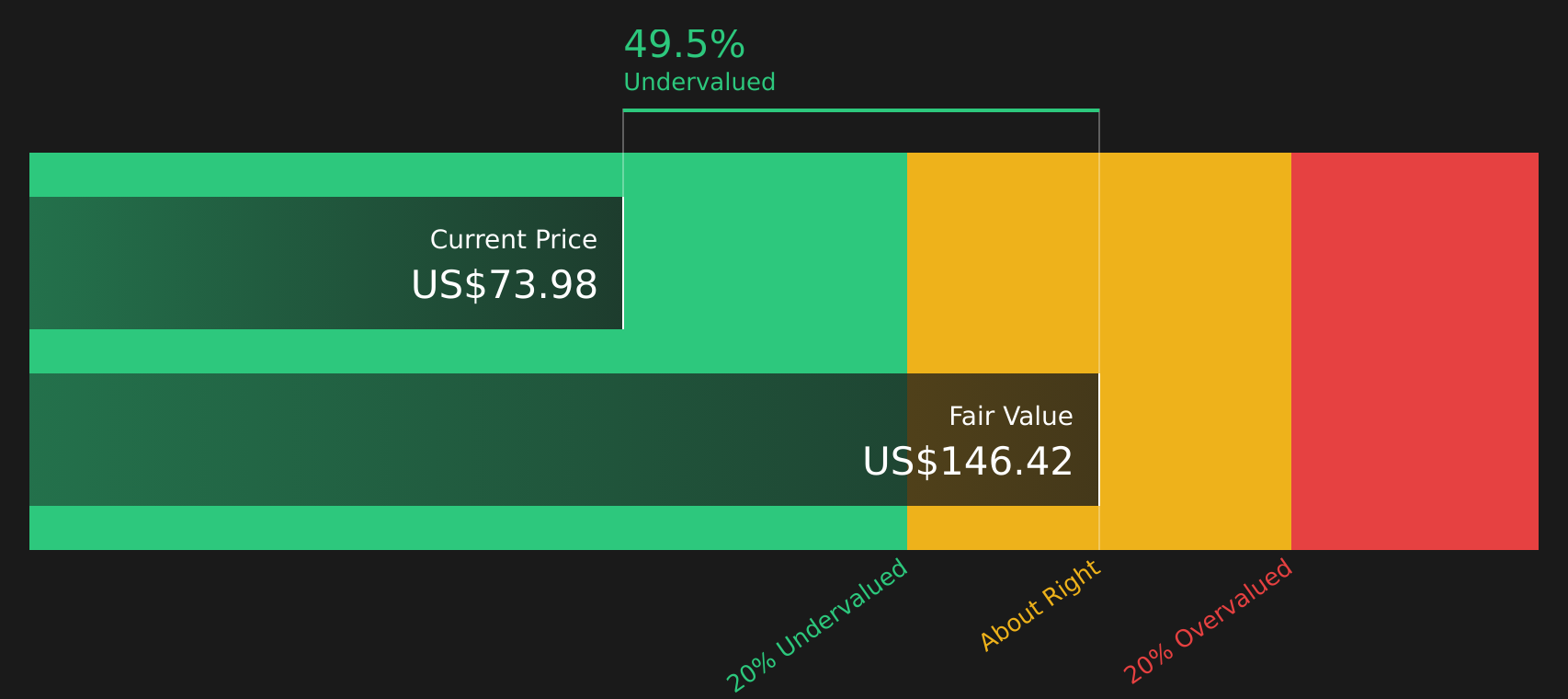

On this basis, the DCF model produces an estimated intrinsic value of $147.56 per share. Compared with the recent share price of $74.55, the implied discount is about 49.5%, which indicates Booz Allen Hamilton Holding is trading well below this DCF estimate.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Booz Allen Hamilton Holding is undervalued by 49.5%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Approach 2: Booz Allen Hamilton Holding Price vs Earnings

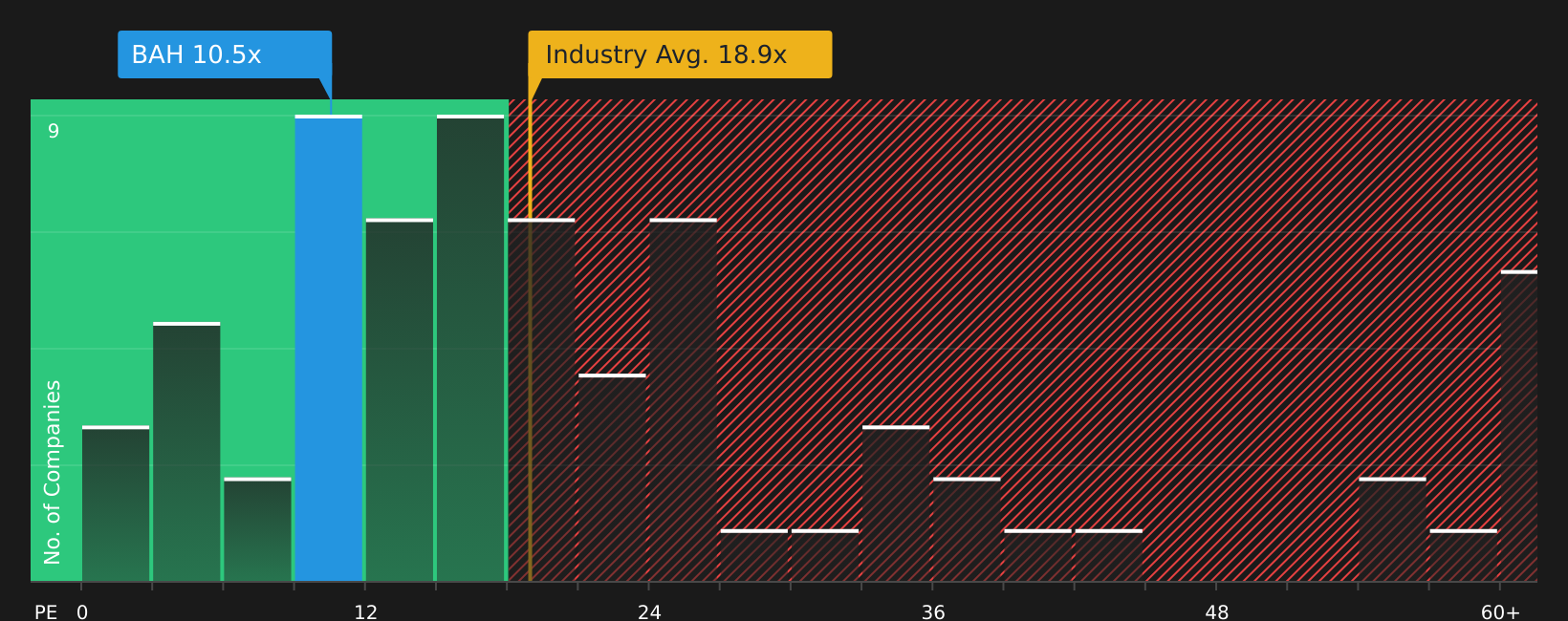

For a profitable company like Booz Allen Hamilton Holding, the P/E ratio is a useful yardstick because it directly links what you pay for the stock to the earnings it currently generates. Investors usually accept a higher or lower P/E depending on what they expect for future earnings growth and how risky those earnings appear to be, so there is no single “right” number that fits every company.

Booz Allen Hamilton Holding currently trades on a P/E of 10.56x. This is below the Professional Services industry average P/E of 19.96x and also below the peer average of 18.89x. To refine that comparison, Simply Wall St calculates a proprietary “Fair Ratio” for the stock of 15.98x.

The Fair Ratio is designed to be more tailored than a simple peer or industry comparison because it incorporates factors such as earnings growth, profit margins, the company’s industry and market capitalization, as well as key risk measures. By comparing the current P/E of 10.56x with the Fair Ratio of 15.98x, the stock appears to trade at a discount to this customized benchmark.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Booz Allen Hamilton Holding Narrative

Earlier the article mentioned that there is an even better way to understand valuation. This is where Narratives come in, giving you a simple way to write your own story for Booz Allen Hamilton Holding by linking your assumptions about future revenue, earnings and margins to a forecast and a fair value, then comparing that fair value with today’s price to decide whether the stock looks attractive or stretched.

On Simply Wall St’s Community page, Narratives are available as an easy tool that lets you plug in your view and see it quantified. They update automatically as new information such as earnings or news is added so your Booz Allen Hamilton Holding view does not stay frozen in time.

For example, one investor might build a Booz Allen Hamilton Holding Narrative around the higher analyst fair value of about US$140.29, reflecting assumptions similar to the more optimistic cohort. Another might align with the lower fair value of about US$74, closer to the cautious view. By comparing each Narrative’s fair value with the current share price, both investors can see whether their own story points toward the stock being cheap, expensive or roughly fairly priced right now.

For Booz Allen Hamilton Holding however we'll make it really easy for you with previews of two leading Booz Allen Hamilton Holding Narratives:

Fair value: US$93.77 per share

Implied discount to this fair value versus the last close of US$74.55: about 20.5% undervalued

Revenue growth assumption: 3.04% per year

- Focuses on federal digital, AI and cybersecurity demand supporting Booz Allen Hamilton Holding's contract pipeline and long term backlog.

- Assumes outcome based and tech enabled contracts can support margins, backed by investments in proprietary offerings and a larger venture arm.

- Highlights risks from government funding delays, contract concentration, execution on complex fixed price work and competition affecting profitability.

Fair value: US$74.00 per share

Implied premium to this fair value versus the last close of US$74.55: about 0.7% overvalued

Revenue growth assumption: 2.07% per year

- Emphasizes pressure on Booz Allen Hamilton Holding's traditional consulting model as automation and AI adoption change how governments buy services.

- Assumes tighter federal budgets and a shift to outcome based, fixed price contracts keep margins under pressure and increase earnings volatility.

- Accepts that AI, cyber and defense work and partnerships offer opportunities, but frames them within a cautious view on contract risk and valuation.

If you want to see how these previews compare with the full range of community views and valuation work on Booz Allen Hamilton Holding, See what the community is saying about Booz Allen Hamilton Holding.

Do you think there's more to the story for Booz Allen Hamilton Holding? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.