Boston Scientific (BSX) Valuation Check After Earnings Strength And Softer Electrophysiology And Watchman Trends

Boston Scientific Corporation BSX | 62.82 | +1.32% |

Earnings catalyst and shifting sentiment

Boston Scientific (BSX) is back in focus after its latest earnings report, where solid year over year growth sat alongside softer electrophysiology and Watchman trends, prompting more cautious sentiment and several analyst target cuts.

At a share price of US$76.27, Boston Scientific has seen a 30 day share price return of 21.89% and a year to date share price return decline of 19.47%. The 5 year total shareholder return of 98.67% signals longer term holders have still seen strong gains, despite recent pressure linked to 2026 guidance, electrophysiology concerns and upcoming trial milestones.

If Boston Scientific's recent volatility has you reassessing healthcare exposure, you might want to look at a different corner of the sector through our screener of 26 healthcare AI stocks.

With earnings growing, 2026 sales guidance in place and the share price pulling back, it raises a straightforward question for you: Is Boston Scientific now trading at a discount, or is the market already pricing in the next leg of growth?

Most Popular Narrative: 29.8% Undervalued

Boston Scientific's most widely followed narrative pegs fair value at $108.66 per share versus the last close of $76.27, setting up a sizeable valuation gap for you to assess.

Investment in proprietary, high margin technologies (e.g., next gen mapping, advanced diagnostic tools, differentiated urology or neuromodulation pipelines) combined with successful integration of recent acquisitions (Axonics, SoniVie, Intera, Silk Road) expands Boston Scientific's addressable market and is likely to drive margin expansion as product mix improves.

Curious how that product mix shift feeds into the valuation gap? The narrative leans heavily on compounding earnings, rising margins and a richer multiple than the wider medical equipment group. The exact growth and profitability path behind that story is where things get interesting.

Result: Fair Value of $108.66 (UNDERVALUED)

However, you also need to weigh risks like tariff headwinds and pressure on reimbursement, which could squeeze margins and challenge the high-growth narrative.

Another take: multiples are less generous

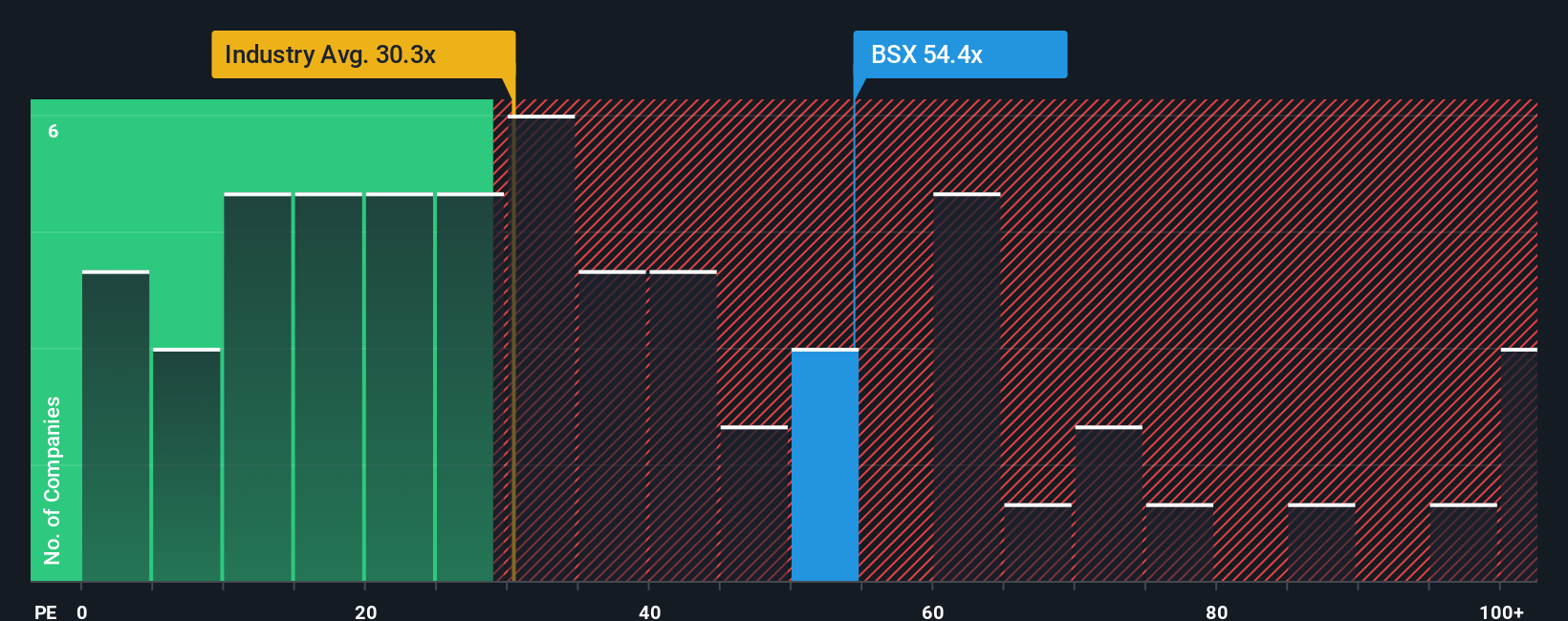

Our DCF model points to fair value of $104.71, so at $76.27 Boston Scientific screens as undervalued. On earnings multiples though, the picture is tighter, with the current P/E of 39x sitting just above the 38.8x fair ratio our work suggests and ahead of the 32.8x industry average. That leaves you asking whether the discount to fair value compensates for the richer earnings tag.

Build Your Own Boston Scientific Narrative

If you see the numbers differently or prefer to test your own assumptions, you can build a custom view of Boston Scientific in under three minutes, starting with Do it your way.

A great starting point for your Boston Scientific research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Boston Scientific has sharpened your focus, do not stop here. Broaden your watchlist with a few targeted stock ideas that fit different roles in your portfolio.

- Hunt for pricing gaps where quality and valuation meet by scanning our 52 high quality undervalued stocks, which flags companies the market may be overlooking.

- Strengthen your income stream by checking out 14 dividend fortresses, built around companies offering higher yields with a focus on resilience.

- Prioritize resilience first and potential upside second by reviewing 84 resilient stocks with low risk scores, which highlights businesses with lower risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.