BridgeBio Pharma (BBIO) Is Up 5.1% After Kidney Data Boost Attruby And Infigratinib Advances

BridgeBio Pharma BBIO | 0.00 |

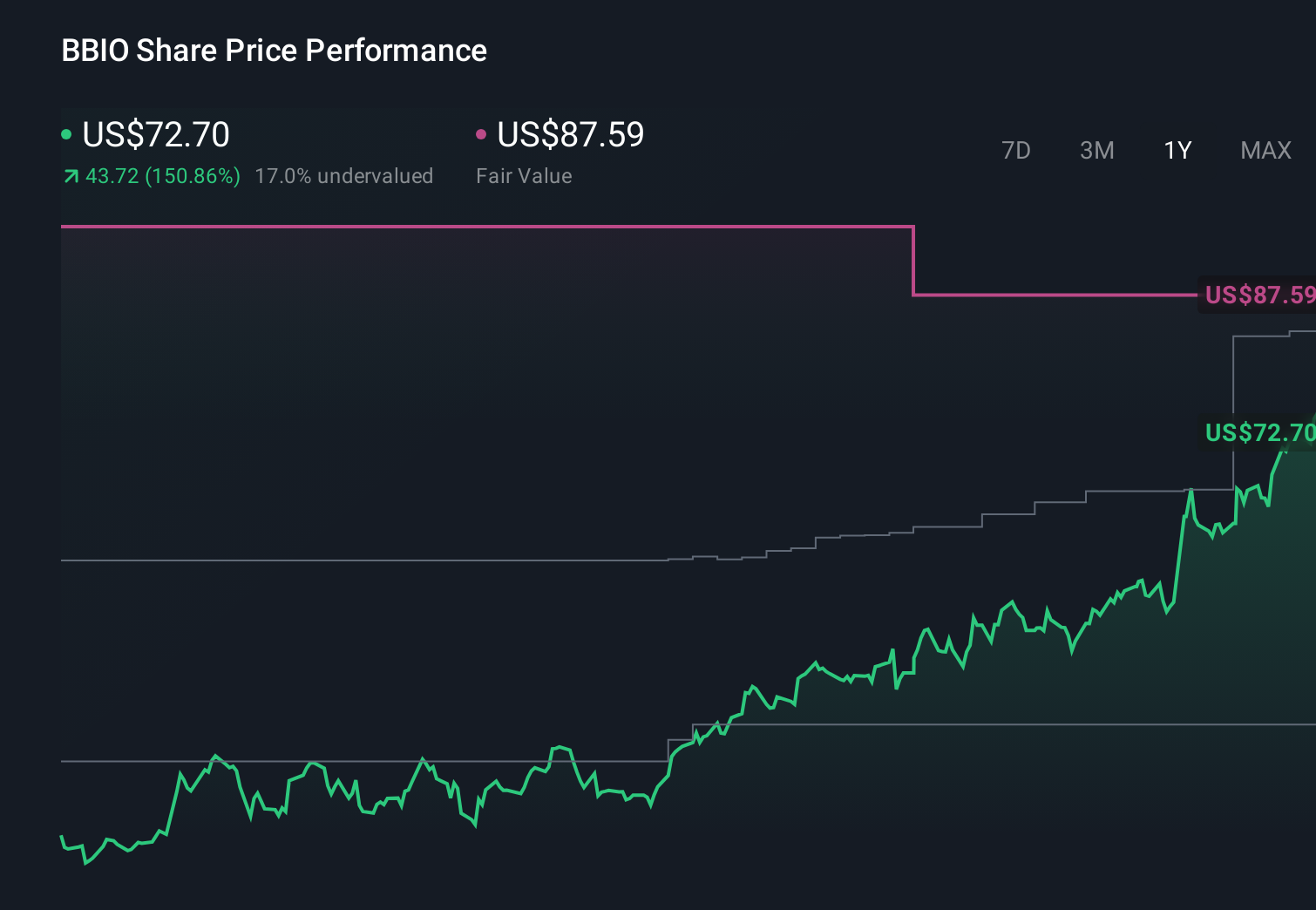

- BridgeBio Pharma recently reported positive Phase 3 data for oral infigratinib in children with achondroplasia and published new post‑hoc analyses in Circulation: Heart Failure suggesting kidney-protective effects of acoramidis (Attruby) in transthyretin amyloid cardiomyopathy, alongside securing up to US$1.00 billion in preferred equity financing and multiple index reclassifications.

- Together, these clinical, regulatory and financing developments reinforce BridgeBio’s push to expand Attruby’s real‑world profile while advancing infigratinib toward potential regulatory filings in achondroplasia and hypochondroplasia.

- We will now examine how the kidney-protective findings for Attruby may reshape BridgeBio’s investment narrative and future growth profile.

The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

BridgeBio Pharma Investment Narrative Recap

To own BridgeBio today, you need to be comfortable with a story built around Attruby’s performance in transthyretin amyloid cardiomyopathy and the company’s ability to convert its late‑stage rare disease pipeline into approved products. The new kidney‑protective data for Attruby supports the current franchise but does not change that the most important near‑term catalysts remain regulatory decisions for BBP‑418, encaleret and infigratinib, while key risks still center on concentration in Attruby and ongoing net losses.

The preferred equity financing of up to US$1.00 billion stands out as especially relevant here. It provides BridgeBio with additional capital to fund commercialization of Attruby and late‑stage trials like PROPEL 3 for infigratinib without an immediate common equity raise, which could matter if future clinical or regulatory milestones take longer or cost more than expected and the company continues to run significant operating losses.

However, while Attruby’s kidney data is encouraging, investors should still be aware that BridgeBio’s heavy reliance on this franchise means that...

BridgeBio Pharma's narrative projects $2.7 billion revenue and $895.2 million earnings by 2029.

Uncover how BridgeBio Pharma's forecasts yield a $102.71 fair value, a 31% upside to its current price.

Exploring Other Perspectives

Before this news, the most cautious analysts were assuming revenue could reach about US$2.3 billion by 2029 yet still saw earnings risk as high, reminding you that views on Attruby’s concentration and pricing exposure can differ sharply and may now shift again in light of the new data.

Explore 6 other fair value estimates on BridgeBio Pharma - why the stock might be worth over 4x more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your BridgeBio Pharma research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free BridgeBio Pharma research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate BridgeBio Pharma's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.