Bristol Myers Squibb (BMY) Returns To US$7.1b Trailing Profit Challenging Bearish Narratives

Bristol-Myers Squibb Company BMY | 58.06 58.06 | -0.96% 0.00% Pre |

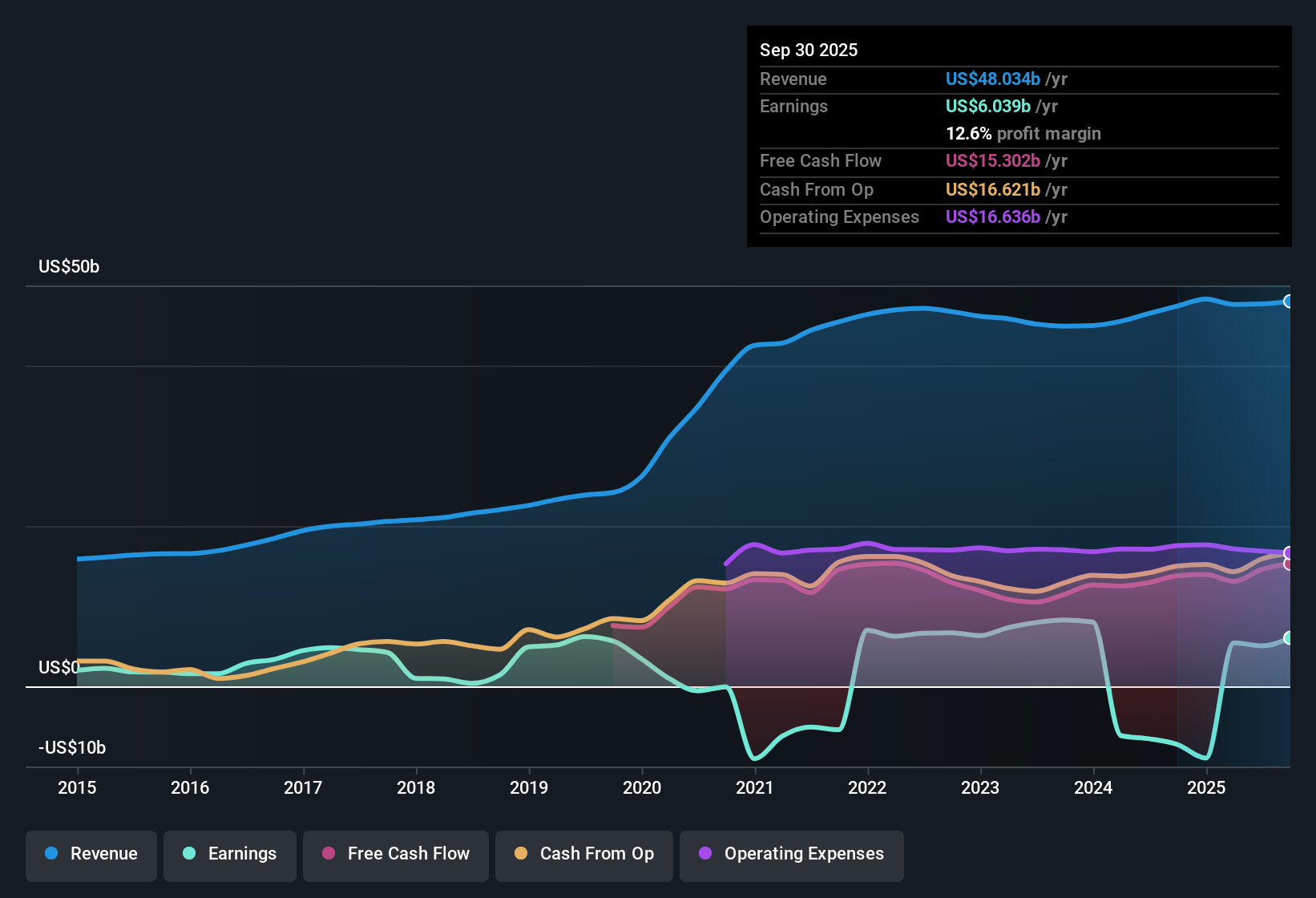

Bristol Myers Squibb (BMY) closed out FY 2025 with Q4 revenue of US$12.5 billion and basic EPS of US$0.53, alongside net income of US$1,087 million, setting the tone for how investors will read the full year. Over the past few quarters, the company has seen revenue move from US$11.2 billion in Q1 2025 to a range of about US$12.2 billion to US$12.7 billion in Q2 through Q4. Quarterly basic EPS has ranged from US$0.64 to US$1.21 across the year, giving a clearer picture of how profits track against the top line. With trailing 12 month EPS at US$3.47 on revenue of US$48.2 billion, the latest print puts the focus squarely on how efficiently Bristol Myers Squibb is converting that revenue into sustainable margins.

See our full analysis for Bristol-Myers Squibb.With the headline numbers on the table, the next step is to see how these results line up against the prevailing Bristol Myers Squibb narratives that investors follow and where the data pushes back on those stories.

US$7.1b trailing profit after last year’s loss

- On a trailing 12 month basis, Bristol Myers Squibb reported net income of US$7.1b and basic EPS of US$3.47, compared with a loss of US$8.9b and EPS of US$4.41 loss in the prior year’s trailing numbers, where results were affected by a US$6.3b one off loss.

- What stands out for a more bullish take is that this move from a trailing loss to a US$7.1b profit sits alongside a 5 year earnings growth rate of 13.6% per year. Yet forecasts in the dataset still call for earnings to decline by 1.3% per year over the next three years, which creates a tension between the historical growth profile and the more cautious forward view.

- Supporters of the bullish angle can point to the current trailing profitability and the US$48.2b of trailing revenue as evidence that the business is earning meaningful cash today rather than only relying on future hopes.

- At the same time, those earnings forecasts ask you to think about how durable that US$7.1b profit is if the top line is expected to shrink, so it is worth checking which parts of the portfolio are driving the recent trailing rebound compared with the period that included the large one off loss.

Bulls argue the latest shift back to profit could matter more than the backward looking one off loss, and that is exactly where the long term narrative on BMY starts to get interesting. 📊 Read the full Bristol-Myers Squibb Consensus Narrative.

Revenue near US$48b as forecasts flag a 6.4% annual decline

- Trailing 12 month revenue sits at US$48.2b, while the forecasts in the data point to revenue declining by about 6.4% per year over the next three years, so the key question is how much of that US$48.2b can be maintained as older drugs mature.

- Critics focusing on the bearish angles highlight that a revenue decline at 6.4% per year and an earnings decline at 1.3% per year would pressure how much profit can be supported on that US$48.2b base. Yet the recent quarterly pattern, with revenue between US$11.2b and US$12.7b through FY 2025, shows a relatively tight range that does not on its own confirm the projected drop.

- The Q4 2025 print of US$12.5b in revenue compares with US$12.3b in Q4 2024, which means the forecasted decline is not yet visible in these specific period to period figures, so the bearish view is leaning more on forward expectations than on the latest trailing trend.

- For a beginner investor, this split between current trailing stability around roughly US$12b per quarter and projected future declines is the core tension to keep in mind when thinking about how resilient BMY’s revenue engine might be.

P/E of 17.9x with DCF fair value at US$138.94

- Bristol Myers Squibb is trading on a P/E of 17.9x, compared with 21.2x for the US Pharmaceuticals industry and 21.5x for peers, while the DCF fair value in the dataset is US$138.94 against a current share price of US$61.99.

- What is interesting for a bullish valuation story is that the shares sit below both peer and industry P/E levels and at a large discount to the DCF fair value. Yet the same dataset also flags a high debt load and those 3 year revenue and earnings decline forecasts, which keeps the valuation gap from being a simple “cheap is good” conclusion.

- On one side, the lower 17.9x P/E relative to the 21.2x and 21.5x benchmarks, together with a reported 4.07% dividend yield, supports the idea that investors are being paid a bit more income while paying a lower multiple than the average pharma name.

- On the other side, the combination of high debt and projected declines in both revenue and earnings gives a bearish counterpoint that the discount and the DCF fair value gap could be reflecting these risks

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Bristol-Myers Squibb's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Projected revenue and earnings declines, alongside a high debt load and a discount valuation, suggest that BMY’s balance sheet and future cash support may be under pressure.

If that mix of weak forward expectations and leverage feels uncomfortable, you might want to quickly scan our solid balance sheet and fundamentals stocks screener (45 results) for companies where financial strength is front and center.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.