BT Stock And UK Telecom Shares to Watch After Its Turnaround

BT’s rapid overhaul, from deep cost cuts and a tighter UK focus to a sharp 80% share price gain under CEO Allison Kirkby, has put the entire UK telecom sector under a spotlight. Restructuring, workforce reductions and a clearer split between domestic and international operations are reshaping expectations for free cashflow and competitive strength, while pressure from a larger Vodafone and Openreach subscriber losses adds real tension. This article breaks down three UK telecom stocks exposed to this news, including two that could benefit from the shake-up and one where the risks may be harder to ignore.

Vodafone Group (LSE:VOD)

Overview: Vodafone Group is a global telecom company that provides mobile, broadband and business connectivity, alongside digital services such as IoT platforms, cloud and edge computing, and mobile financial services like M-PESA across Europe, Turkey and Africa. It serves both consumers and organisations in sectors ranging from healthcare and finance to transport, utilities and agriculture.

Operations: Vodafone generates most of its revenue in Germany (€12.1b), the United Kingdom (€9.2b) and Africa (€8.4b), with additional contributions from Other Europe (€5.7b), Turkey (€3.4b) and Common Functions (€1.8b).

Market Cap: £22.7b

Vodafone Group sits at the centre of the UK telecom shake up, with a planned merger that has made it the largest UK mobile operator and left BT refocusing on its home market just as competition intensifies. The company is still loss making, carries high debt and relies on external funding, so execution on cost cuts, German turnaround efforts and complex restructuring remains critical. At the same time, some analysts see the stock as trading well below an estimated intrinsic value and highlight higher margin digital and B2B services plus portfolio simplification as key factors to watch. For investors monitoring BT’s overhaul, Vodafone’s mix of potential opportunities and execution risk is a notable feature in this sector reset.

Vodafone’s cost cuts, merger ambitions and digital pivot could be masking a much bigger valuation story. Before the sector reset moves further, review the DCF valuation analysis for Vodafone Group to see what the market may be missing.

Liberty Global (LBTY.A)

Overview: Liberty Global provides broadband internet, pay TV, fixed-line and mobile services to households and businesses across Europe, with products ranging from high speed WiFi and smart home solutions to cloud based TV platforms and bundled fixed mobile offers. It also sells telecom, cloud and connectivity services to companies of various sizes and to other operators on a wholesale basis.

Operations: Liberty Global reports segment revenue of about US$3.2b from Telenet, US$1.4b from All Other operations and US$0.5b from VM Ireland, alongside joint venture revenue exposures to VMO2 and VodafoneZiggo that are offset by segment adjustments and intercompany eliminations.

Market Cap: US$3.8b

Liberty Global looks intriguing on paper, with the stock trading well below some value estimates and a telecom portfolio tied to gigabit broadband, convergence and sports or media assets. However, the picture is far from straightforward. The group is still loss making with a history of rising losses, high external borrowing and interest costs that are not well covered, and management pay sitting far above peers despite this profitability record. In the UK, where BT is cutting costs aggressively and sharpening its domestic focus, Virgin Media O2 could see more pressure on margins and subscriber churn even as it invests heavily in fibre and customer service. For investors following BT’s overhaul, Liberty Global is a complex, highly financialised telecom play in which the gap between perceived asset value and execution risk is unusually wide.

Liberty Global’s widening gap between complex assets, rising losses and high executive pay raises tough questions for long term holders. Before the story tilts further, review the 2 key rewards and 2 important warning signs (1 is major!).

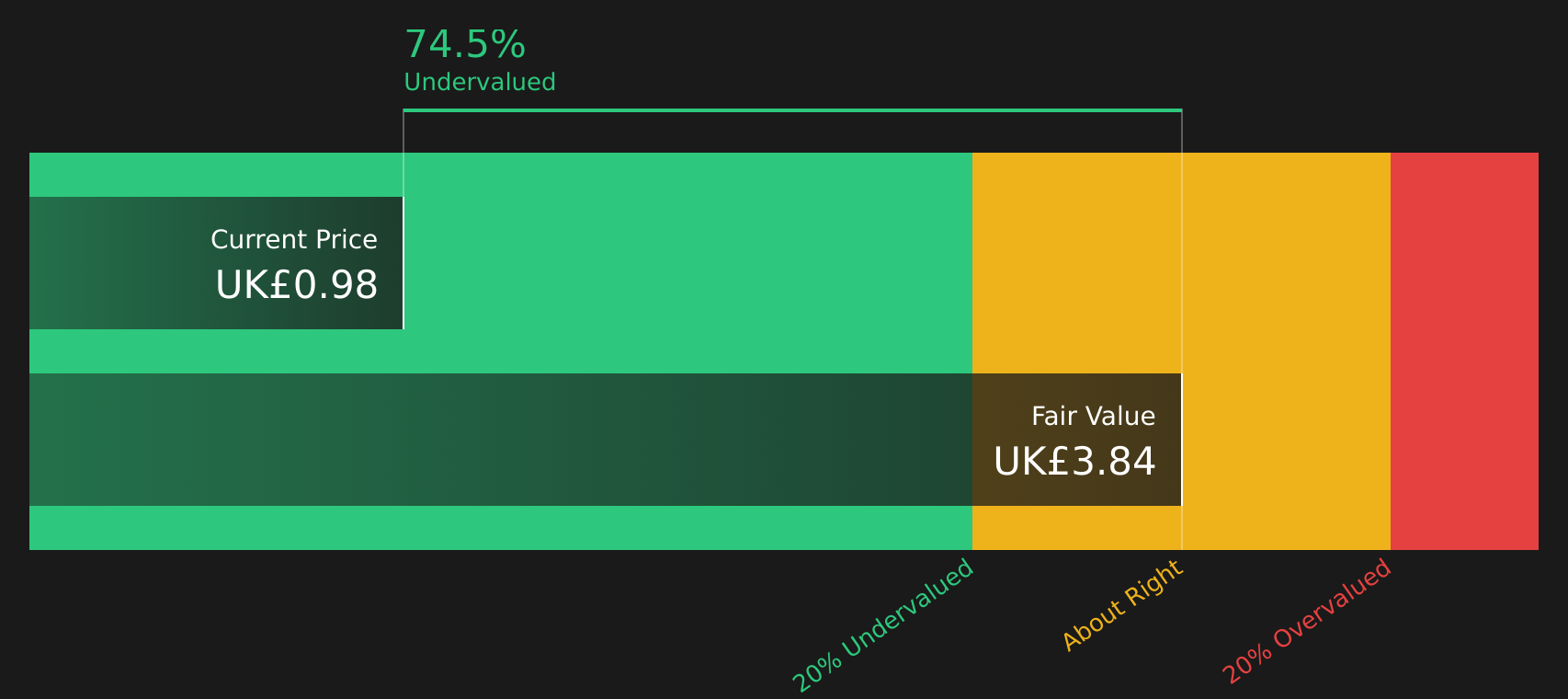

BT Group (LSE:BT.A)

Overview: BT Group is a UK headquartered telecom company that runs fixed and mobile networks, selling broadband, mobile, TV and landline services to households, and connectivity, cloud, cybersecurity and managed network solutions to businesses and public sector customers worldwide under the BT, EE, Plusnet and Openreach brands.

Operations: BT Group generates most of its £19.6b revenue from Consumer (£9.5b), Openreach (£6.2b) and Business (£5.3b), with smaller contributions from International (£2.1b) and Other items, largely anchored in the UK.

Market Cap: £18.6b

BT Group has quickly become one of the most closely watched UK telecom stocks, with an 80% share price rise under CEO Allison Kirkby, aggressive cost cuts, and a sharper UK focus turning a slow moving incumbent into a high profile restructuring story. The plan to reduce the workforce by around 40% and target £3.7b in savings, while pushing fibre and 5G build and tightening the international footprint, is already feeding through to higher free cashflow and better margins, even as revenue edges down and Openreach faces subscriber losses and tougher competition from Vodafone and alternative networks. In addition, there is a wide gap between BT’s market value and some estimates for Openreach alone, together with a growing but still modest dividend. As a result, investors are left with a turnaround that mixes appealing valuation, material debt and funding risk, and unresolved questions about how far the transformation can really go.

BT’s accelerating turnaround, with deep cost cuts and a sharper UK focus, is only half the story. The real question is what the market is still pricing in, so review the 4 key rewards and 3 important warning signs

Take Control of Your Investment Journey

If BT Group or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Momentum Takes Off?

Fresh stock ideas are already building quiet breakout potential while most investors stay caught on yesterday’s moves. Before the best entry points start dropping out of reach, consider researching opportunities that may fit your strategy.

- Spot resilient cash generators early and review a curated list of solid balance sheet and fundamentals (19 results) that could help you stay focused on businesses built to handle pressure while others stall.

- Ride structural demand trends and scan a hand picked set of 35 power grid technology and infrastructure stocks positioned around critical infrastructure upgrades that many investors are still overlooking.

- Get ahead of AI’s real-world rollout and assess carefully filtered 53 AI infrastructure stocks powering data centers and connectivity while they remain under the radar for now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.