Buffett’s OxyChem Bet Could Be a Game Changer for Olin (OLN)

Olin Corporation OLN | 27.95 | +0.68% |

- In recent days, Olin Corporation attracted renewed investor focus as Warren Buffett’s acquisition of OxyChem for about US$10 billion highlighted the cyclical turnaround potential in U.S. chlor-alkali producers.

- Olin's position as the largest domestic chlor-alkali producer and owner of Winchester, the second-largest U.S. ammunition maker, adds material diversification and fundamental appeal during periods of sector transformation.

- We'll examine how Buffett’s major OxyChem purchase and revived interest in chlor-alkali chemicals could reshape Olin’s investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 27 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Olin Investment Narrative Recap

To believe in Olin right now, investors need confidence in a cyclical recovery in global chlor-alkali markets and diversification from the Winchester ammunition segment, which supports fundamentals through industry shifts. Warren Buffett’s OxyChem acquisition spotlights possible upside for industry leaders, but does not change the fact that persistent global overcapacity and deeply depressed EDC prices remain the biggest short-term risks, while the catalyst is anticipated operational cost savings from restructuring programs. Unless market conditions materially improve, these risks remain front and center.

The most relevant recent announcement is Olin’s exit from its Blue Water Alliance JV with Mitsui, positioning the company to seek longer-term opportunities in EDC markets. As the sector garners new attention, this shift could determine how Olin captures value from structural changes in the chlor-alkali space, especially if supply-demand conditions tighten.

In contrast, investors should be aware that ongoing weakness in global construction markets could further challenge Olin’s profitability if...

Olin's outlook forecasts $7.4 billion in revenue and $375.3 million in earnings by 2028. This scenario assumes 3.6% annual revenue growth and a $389.4 million increase in earnings from the current -$14.1 million.

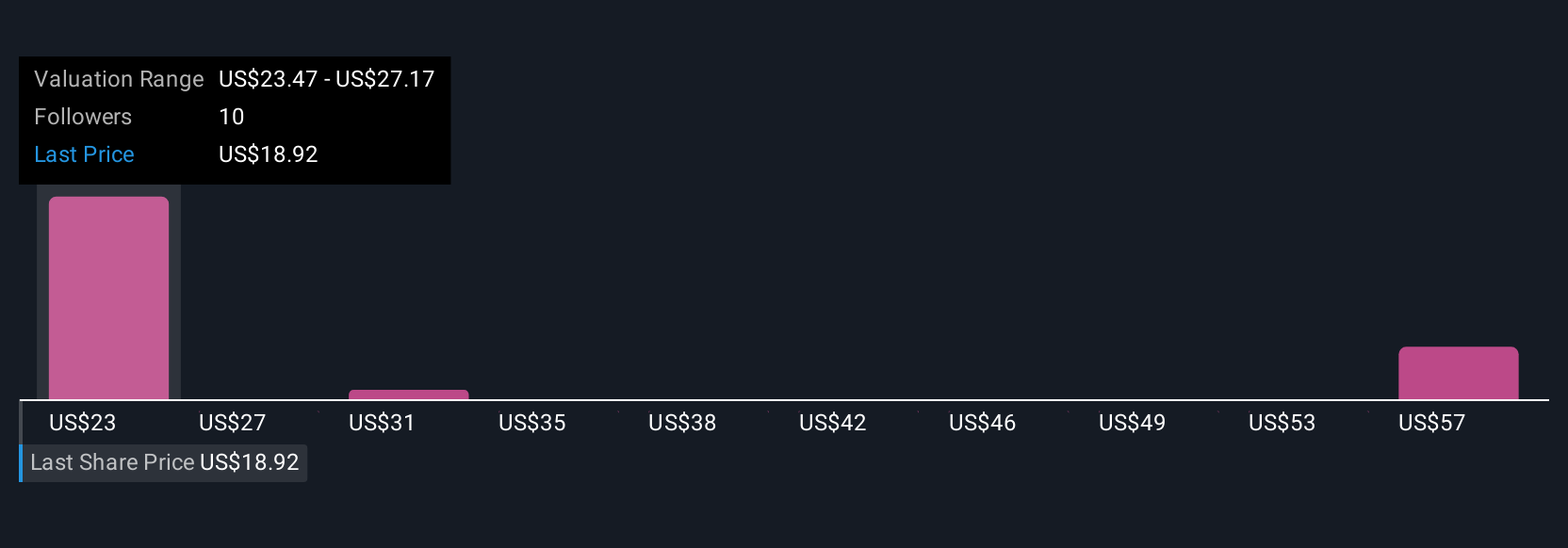

Uncover how Olin's forecasts yield a $24.73 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community estimate Olin's fair value between US$24.73 and US$63.34 per share. With opinions this broad, consider how persistent global overcapacity and low EDC prices could shape Olin’s future and look beyond your own assumptions.

Explore 5 other fair value estimates on Olin - why the stock might be worth just $24.73!

Build Your Own Olin Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Olin research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Olin research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Olin's overall financial health at a glance.

Seeking Other Investments?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find companies with promising cash flow potential yet trading below their fair value.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- The end of cancer? These 27 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.