Butterfly Network (BFLY) Is Up 29.1% After Midjourney Ultrasound Deal - Has The Bull Case Changed?

Butterfly Network, Inc. Class A BFLY | 0.00 |

- In June 2026, Midjourney revealed a whole-body ultrasound scanner built on Butterfly Network’s chip platform, alongside plans for global deployment and payments that could total up to US$74.00 million over five years.

- This collaboration highlights Butterfly’s potential to license its semiconductor and imaging technology beyond handheld probes, opening a new avenue for platform-led revenue.

- Now we’ll examine how the Midjourney licensing opportunity, and its focus on whole-body scanning, could reshape Butterfly Network’s investment narrative.

Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

Butterfly Network Investment Narrative Recap

To own Butterfly Network, you need to believe its ultrasound on chip platform can scale across handheld devices and new embedded uses like Midjourney’s whole body scanners, while the company moves closer to profitability. The Midjourney deal validates the technology and introduces a new licensing path, but near term the key catalyst still looks like execution on hospital and enterprise adoption, while the biggest risk remains high cash burn and the possibility of future dilution if new high margin revenue does not materialize.

Among recent announcements, the appointment of David Horsley as Senior Vice President of Innovation for Butterfly Embedded stands out alongside the Midjourney news. His remit to grow co development and licensing around Ultrasound on Chip directly ties into this new scanner partnership and underlines how embedded deals could complement, rather than replace, the handheld and software catalysts that many investors are watching most closely.

Yet against all this excitement, the risk of continued operating losses and potential dilution is something investors should be aware of if...

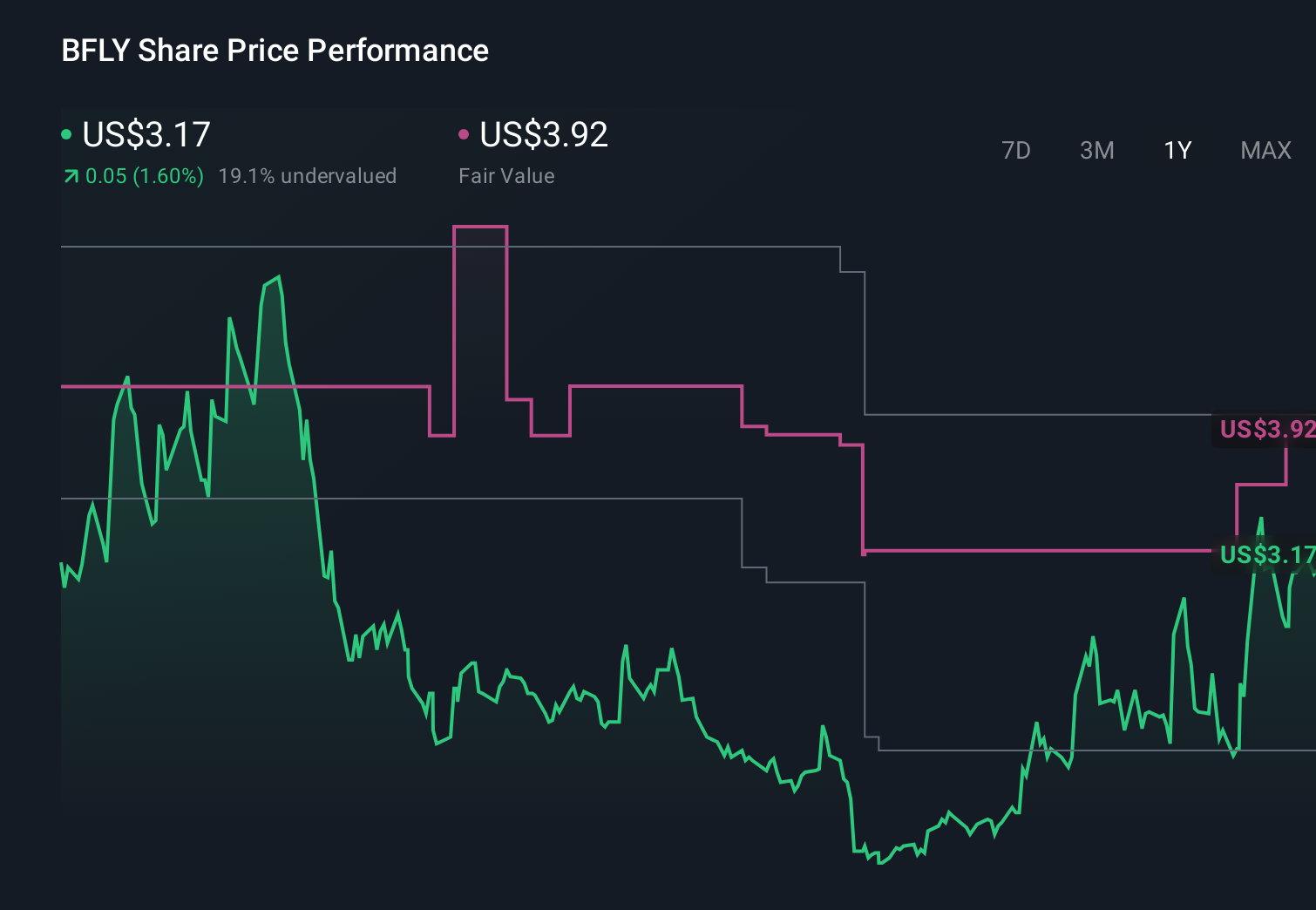

Butterfly Network's narrative projects $167.0 million revenue and $20.4 million earnings by 2029. This requires 17.5% yearly revenue growth and a $96.2 million earnings increase from -$75.8 million today.

Uncover how Butterfly Network's forecasts yield a $5.69 fair value, a 22% downside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already assuming only about 15.8% annual revenue growth and no profits within three years, so if you worry about prolonged cash burn or slower enterprise adoption, their more cautious view offers a useful counterpoint to the optimism around the Midjourney deal.

Explore 7 other fair value estimates on Butterfly Network - why the stock might be worth as much as $7.06!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Butterfly Network research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Butterfly Network research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Butterfly Network's overall financial health at a glance.

Looking For Alternative Opportunities?

Our top stock finds are flying under the radar-for now. Get in early:

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- We've uncovered the 7 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.