Cadence Design Systems (CDNS) Nears Earnings With Valuation Questions Still In Focus

Cadence Design Systems, Inc. CDNS | 0.00 |

Why Cadence Design Systems Stock Is Back On Investors’ Radar

Cadence Design Systems (CDNS) slipped 1.63% in the latest session, trailing broad market indexes as investors look ahead to the July 27 earnings report.

At a share price of $376.8, Cadence Design Systems has seen short term share price momentum cool slightly over the past month. However, its 90 day share price return of 23.91% and 5 year total shareholder return of 169.55% still point to a stock that has rewarded patient holders. The upcoming earnings update is now a key focal point for how investors reassess growth potential and risk.

If you are looking beyond Cadence Design Systems for more ways to tap into the growth of AI in your portfolio, now could be a good time to review 63 profitable AI stocks that aren't just burning cash

After a strong 90 day run and a softer past month, Cadence Design Systems sits close to analyst targets. Does it make more sense to commit fresh capital now or wait for a clearer pullback?

Most Popular Narrative: 1.9% Undervalued

Against a last close of $376.8, the most followed narrative for Cadence Design Systems pegs fair value at about $383.94, so the gap is small but worth understanding before earnings.

The analysts have a consensus price target of $383.94 for Cadence Design Systems based on their expectations of its future earnings growth, profit margins and other risk factors.

However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $440.0, and the most bearish reporting a price target of just $275.0.

Curious what is baked into that fair value just above today’s price? Revenue compounding, margin expansion, and a rich future earnings multiple all sit at the core, but the exact mix might surprise you.

Result: Fair Value of $383.94 (UNDERVALUED)

However, the Cadence Design Systems story could be disrupted if US China tensions hit its sizeable China revenue base, or if key AI partnerships fail to deliver expected demand.

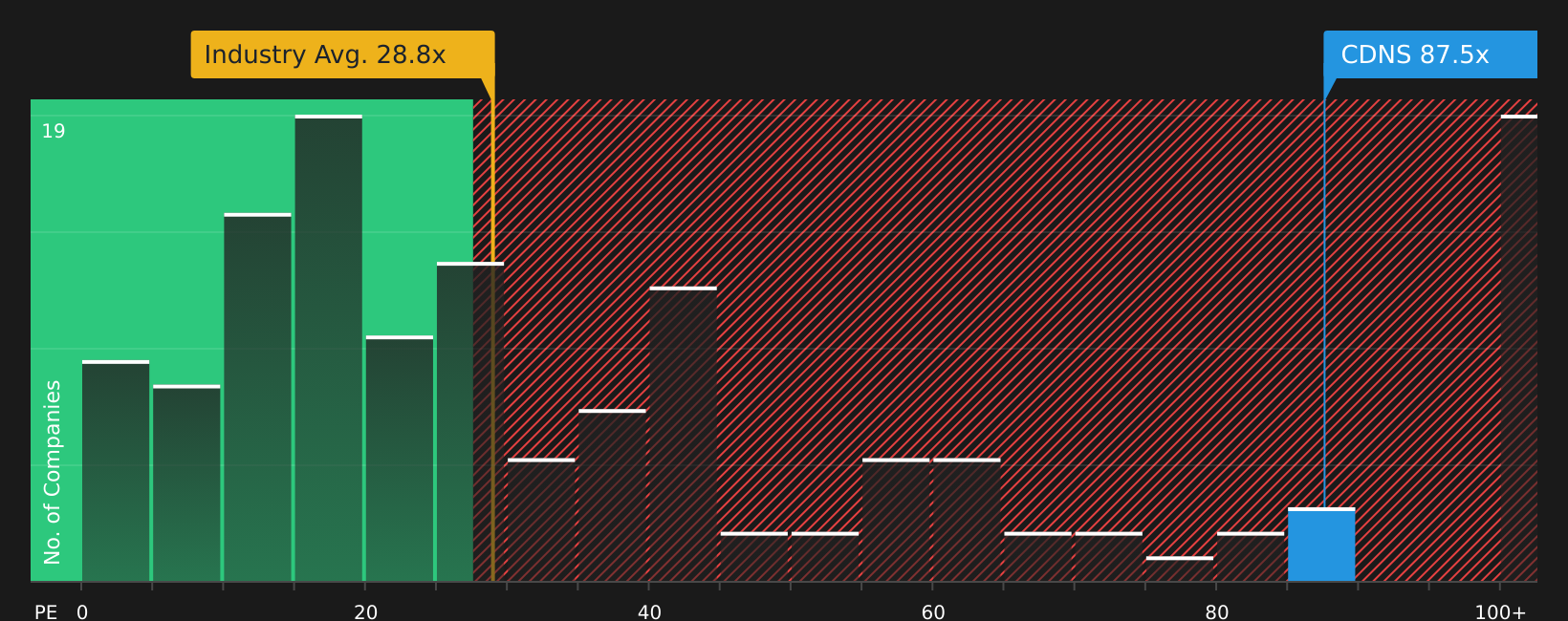

Another View: Cadence Design Systems Looks Expensive On Earnings

The analyst narrative suggests Cadence Design Systems is only 1.9% below fair value, but its P/E of 88.8x tells a tougher story. That compares with a fair ratio of 34.2x, a US Software industry average of 28.9x, and a peer average of 37.9x, which all point to richer valuation risk if sentiment cools.

So if the market eventually leans closer to that fair ratio, how comfortable are you with paying today's multiple for Cadence Design Systems?

Next Steps

If the mixed signals around Cadence Design Systems leave you on the fence, act while the data is fresh and form your own view by weighing its 2 key rewards

Looking For More Investment Ideas Beyond Cadence Design Systems?

Do not stop at Cadence Design Systems. Broaden your watchlist with fresh ideas sourced from data driven stock screens built to surface different types of opportunities.

- Spot potential underpriced opportunities early by reviewing companies in our 44 high quality undervalued stocks before the crowd focuses on them.

- Strengthen portfolio resilience by focusing on businesses highlighted in the solid balance sheet and fundamentals stocks screener (48 results) with robust financial footing.

- Aim to get ahead of the market by searching through the screener containing 20 high quality undiscovered gems that the wider investor base may be overlooking.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.