Camtek (CAMT) Is Down 18.1% After AI-Driven Orders Fuel Bold H2 2026 Revenue Guidance – Has The Bull Case Changed?

Camtek Ltd CAMT | 0.00 |

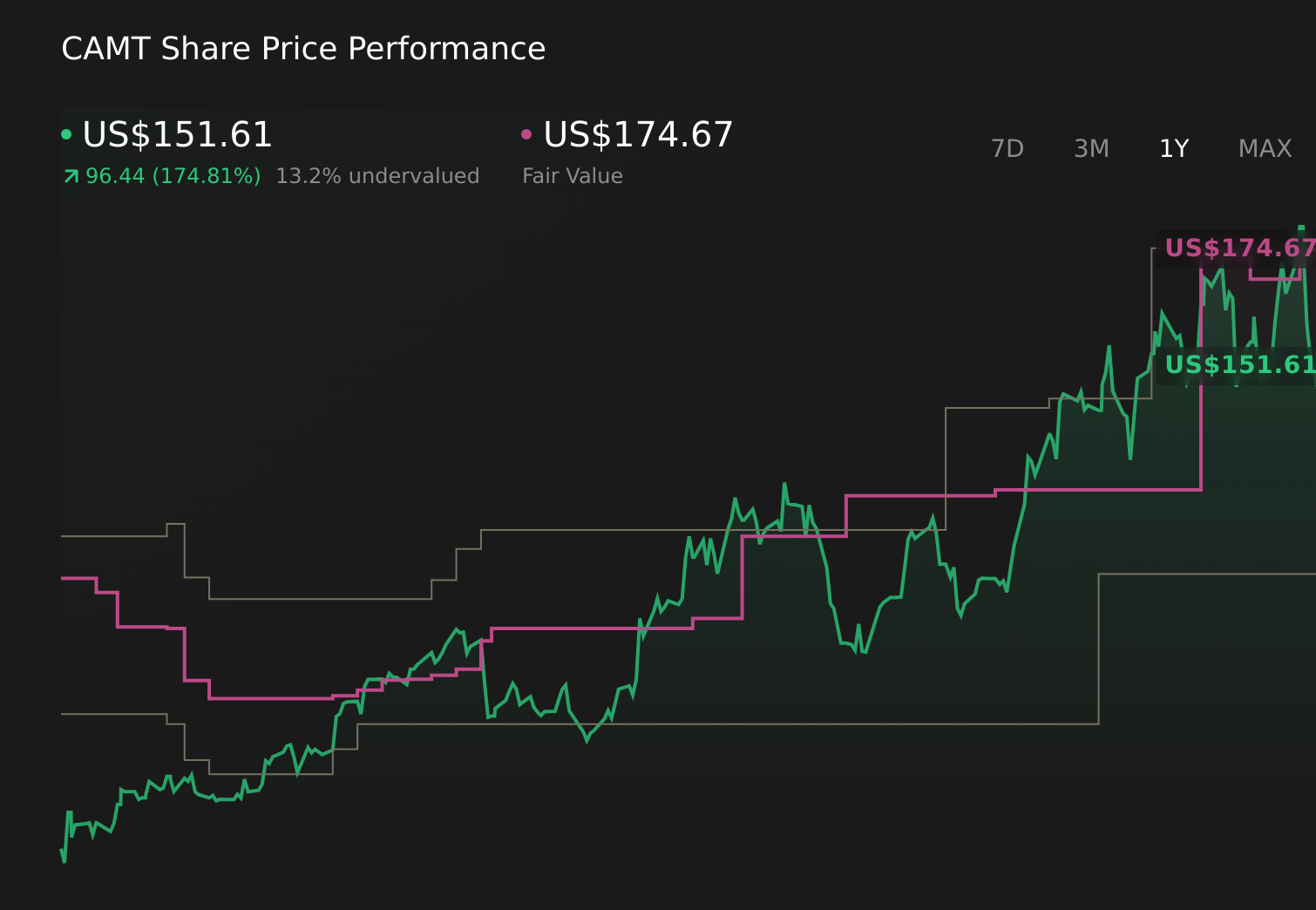

- In the past week, Camtek Ltd. reported first‑quarter 2026 results showing sales of US$121.66 million with slightly lower net income and earnings per share versus a year earlier, while issuing second‑quarter revenue guidance of US$129 million to US$131 million and signaling revenue growth of over 25% in the second half of 2026 versus the first half.

- Alongside this guidance, Camtek highlighted unprecedented AI-linked order intake and the integration of its Visual Layer acquisition, underscoring how AI-driven inspection and metrology capabilities are becoming central to its growth plans despite current profitability pressure.

- Against this backdrop of strong AI-related orders and ambitious second-half revenue guidance, we’ll explore how these updates influence Camtek’s existing investment narrative.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

Camtek Investment Narrative Recap

To own Camtek, you really need to believe that AI-driven advanced packaging will keep pulling more inspection and metrology spend toward its tools. The latest Q1 2026 report and strong second half revenue outlook reinforce that the key near term catalyst is AI related orders converting into shipments, while the biggest risk remains a mismatch between this ambitious growth path and Camtek’s current profitability and valuation profile. For now, the earnings miss on margins does not yet change that core setup.

Among recent announcements, the US$31 million multi system order from an OSAT for CoWoS like AI packaging, plus over US$90 million in OSAT orders in Q1 2026, looks most directly tied to the company’s guidance for more than 25% second half revenue growth. These wins connect the headline “unprecedented” AI order intake to concrete systems demand, but they also heighten exposure to any slowdown or CapEx shift at a relatively narrow set of advanced packaging and HPC customers.

Yet beneath the strong AI order story, investors should also be aware that...

Camtek's narrative projects $786.7 million revenue and $314.9 million earnings by 2029. This requires 16.6% yearly revenue growth and about a $264.2 million earnings increase from $50.7 million today.

Uncover how Camtek's forecasts yield a $174.67 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Some analysts project an aggressive path to about US$942 million of revenue and US$362 million of earnings by 2029, a far more optimistic view that could be tested by how today’s AI driven orders and Camtek’s dependence on advanced packaging actually play out, so it is worth comparing these bullish assumptions with more cautious scenarios before deciding where you stand.

Explore 3 other fair value estimates on Camtek - why the stock might be worth as much as $174.67!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Camtek research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Camtek research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Camtek's overall financial health at a glance.

No Opportunity In Camtek?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Capitalize on the AI infrastructure supercycle with our selection of the 42 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.