Camtek (CAMT) Is Up 17.7% After Landing US$105 Million In AI-Focused HBM Orders – Has The Bull Case Changed?

Camtek Ltd CAMT | 0.00 |

- Earlier this month, Camtek Ltd. reported securing over US$105,000,000 in multi-system orders tied to AI applications from a tier-1 OSAT and an HBM customer, with deliveries scheduled for 2027.

- The scale and AI focus of these Hawk system orders underline how closely Camtek’s inspection and metrology tools are now aligned with high-bandwidth memory and advanced packaging demand.

- We’ll now examine how these AI-focused multi-system orders from leading semiconductor customers may influence Camtek’s existing investment narrative and risk profile.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Camtek Investment Narrative Recap

To own Camtek today, you need to believe its inspection and metrology tools will stay central to AI-driven advanced packaging and HBM spending, despite cyclicality and intense competition. The new US$105,000,000 in Hawk system orders reinforces the near term AI packaging catalyst but also deepens reliance on a small group of HPC and HBM customers. That concentration remains the key risk, as any pullback in their CapEx or supplier choices could quickly affect Camtek’s growth and earnings stability.

The March 30, 2026 announcement of over US$90,000,000 in AI related OSAT orders is especially relevant here. Together with the latest US$105,000,000 Hawk and HBM contracts, it highlights how fast Camtek’s backlog is tilting toward AI packaging and high bandwidth memory. This strengthens the near term growth narrative around Hawk adoption, but it also ties Camtek’s fortunes more tightly to advanced packaging cycles and the investment decisions of a few large Asian customers.

Yet behind the upbeat AI backlog, investors should be aware of how concentrated Camtek’s revenue has become, especially if key HPC customers were to...

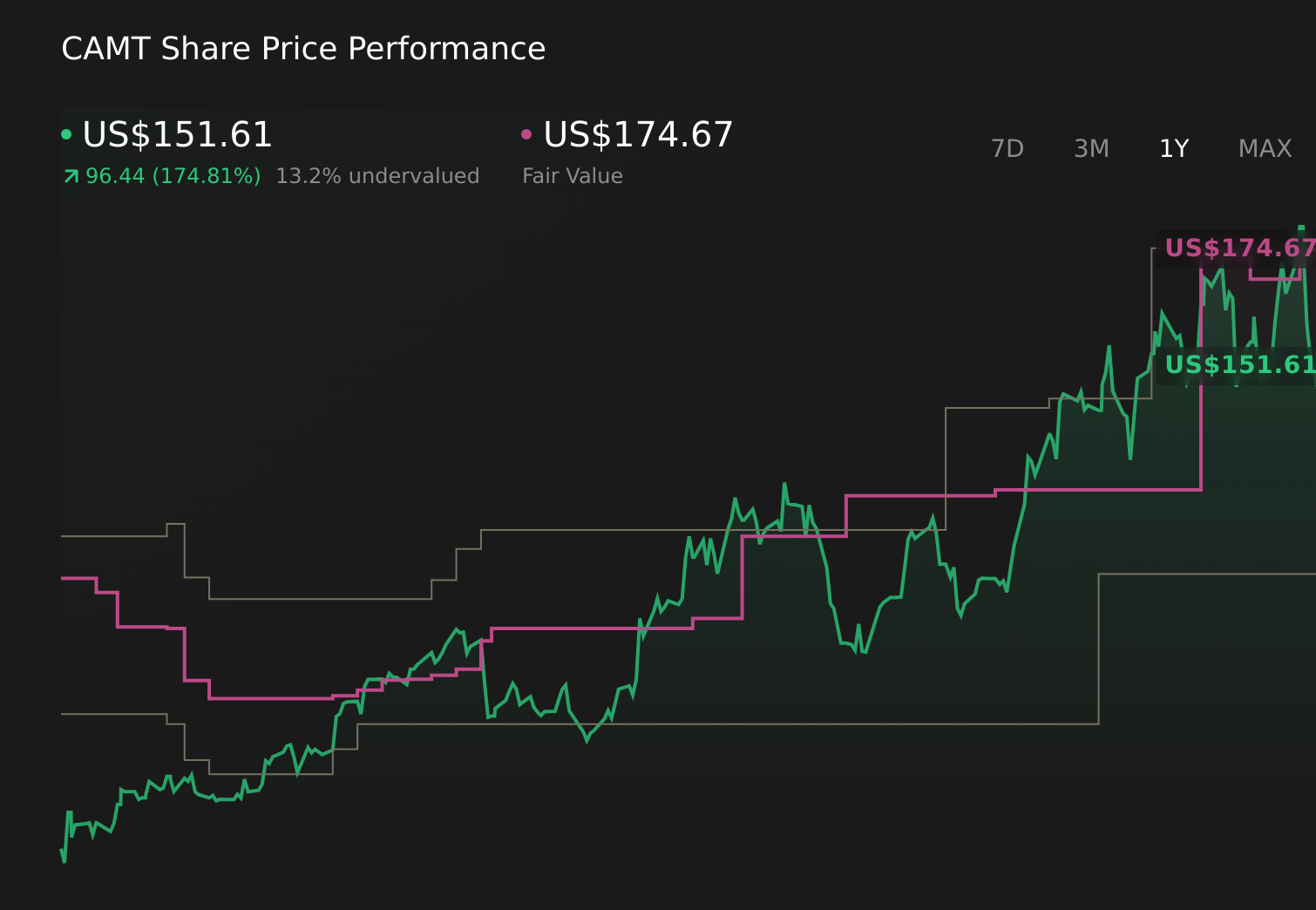

Camtek's narrative projects $786.7 million revenue and $314.9 million earnings by 2029. This requires 16.6% yearly revenue growth and about a $264.2 million earnings increase from $50.7 million today.

Uncover how Camtek's forecasts yield a $174.67 fair value, a 10% downside to its current price.

Exploring Other Perspectives

Before this AI order surge, the most optimistic analysts already assumed Camtek’s revenue could reach about US$948,300,000 and earnings US$369,400,000, which is a much more optimistic story than the baseline view and leans heavily on continued AI driven advanced packaging demand; with contracts now stretching into 2027, you can see how different your conclusions might be if you focus on that upside or on the risk that much of this growth still depends on a concentrated set of HPC and HBM customers.

Explore 3 other fair value estimates on Camtek - why the stock might be worth as much as $174.67!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Camtek research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Camtek research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Camtek's overall financial health at a glance.

Seeking Other Investments?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- This technology could replace computers: discover 29 stocks that are working to make quantum computing a reality.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.