Can Alignment Healthcare’s (ALHC) 4-Star Medicare Advantage Streak Sustain Its Quality-Driven Investment Narrative?

Alignment Healthcare, Inc. ALHC | 0.00 |

- Alignment Healthcare recently released its 2025 Impact Report, highlighting that its proactive, technology-enabled care model has been associated with fewer emergency room visits, hospitalizations, and post-acute stays versus traditional Medicare benchmarks.

- The report also confirms that, for the second consecutive year, 100% of Alignment’s members are enrolled in Medicare Advantage plans rated 4 Stars or higher by the Centers for Medicare & Medicaid Services, reinforcing the quality metrics underpinning its business model.

- Now we’ll examine how the sustained 4-Star-plus CMS ratings might influence Alignment Healthcare’s investment narrative after this latest update.

We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Alignment Healthcare Investment Narrative Recap

To own Alignment Healthcare, you need to believe its tech-enabled Medicare Advantage model can keep converting strong clinical quality into durable margins, even as regulation tightens. The latest Impact Report reinforces that quality story, but the short term catalyst is still whether high Star Ratings translate into sustained reimbursement strength and member retention. The biggest risk remains potential Medicare Advantage policy and rate pressure, and this update does not materially change that regulatory overhang.

The most relevant recent development is Alignment’s confirmation that 100% of members are again in 4 Star or higher plans for the 2026 payment year, supporting higher benchmark payments and better retention economics. Paired with its addition to the S&P 600 Health Care index, this quality signal feeds directly into the core catalyst of scaling a profitable, high rated platform while offsetting rising medical and operating costs.

Yet despite these quality scores, investors should be aware that...

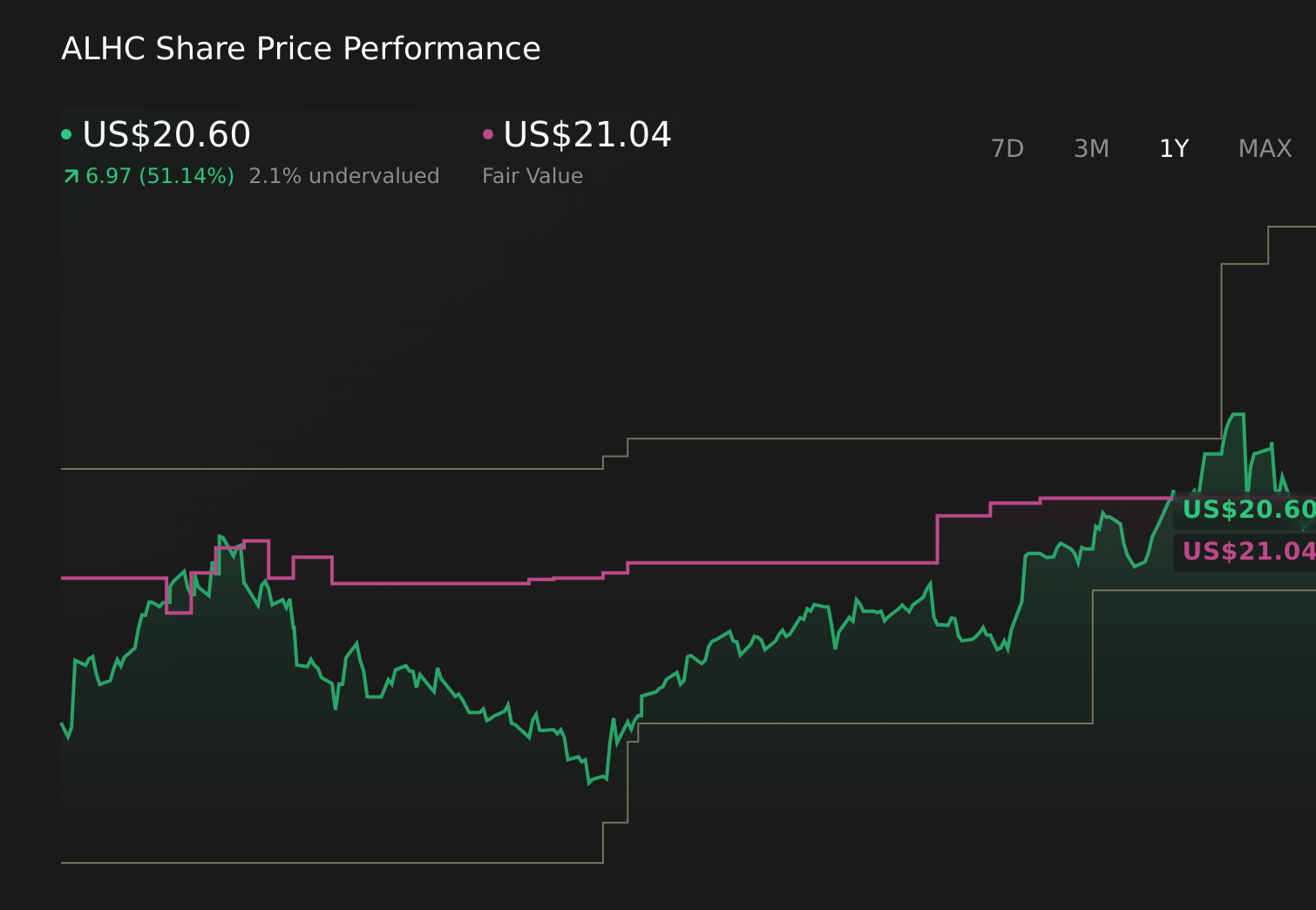

Alignment Healthcare's narrative projects $8.7 billion revenue and $197.2 million earnings by 2029. This requires 27.0% yearly revenue growth and about a $177.4 million earnings increase from $19.8 million today.

Uncover how Alignment Healthcare's forecasts yield a $24.92 fair value, a 83% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts saw a path to about US$9.2 billion in revenue and US$195.2 million in earnings by 2029, but compared with the baseline view this is a far more aggressive bet on Stars driven market share gains that the new Impact Report may or may not ultimately support, so it is worth weighing both narratives before you decide how you feel about Alignment’s long term potential.

Explore 2 other fair value estimates on Alignment Healthcare - why the stock might be worth over 3x more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Alignment Healthcare research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Alignment Healthcare research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Alignment Healthcare's overall financial health at a glance.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

- Capitalize on the AI infrastructure supercycle with our selection of the 47 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.