Can Delta Air Lines’ (DAL) New Leadership Structure Rebalance Costs, Service Quality, and Global Ambitions?

Delta Air Lines, Inc. DAL | 66.76 | -1.24% |

- Delta Air Lines recently overhauled its leadership team, appointing longtime executive Erik Snell as Chief Financial Officer and promoting Peter Carter to President, while also naming Dan Janki Chief Operating Officer and making several other senior role changes following retirements and departures.

- These moves place finance, operations, customer experience, marketing, and international growth more tightly under CEO Ed Bastian’s direct reports, potentially reshaping how Delta balances cost control, service quality, and global expansion amid ongoing geopolitical and fuel cost pressures.

- We’ll now examine how the leadership reshuffle, particularly Snell’s appointment as CFO, could influence Delta’s existing investment narrative and outlook.

Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

Delta Air Lines Investment Narrative Recap

To own Delta today, you have to believe its focus on premium, loyalty, and international flying, along with disciplined capacity and cash flow management, still holds up against shocks like the current Middle East conflict and fuel price spikes. The leadership overhaul does not fundamentally alter that near term, but it could influence how Delta balances cost control and service reliability, while the biggest immediate risk remains geopolitical disruption feeding into higher fuel costs and route suspensions.

The most relevant recent announcement here is Erik Snell’s appointment as Chief Financial Officer, with oversight of finance, fleet, supply chain, and Monroe Energy. Given the pressure from rising oil prices and war related flight cancellations, the CFO’s role in managing fuel exposure, capex, and balance sheet risk looks more central to the story than ever, particularly as Delta works to protect margins and maintain flexibility around capacity and aircraft investment.

But against this backdrop, the risk that rising fuel and geopolitical tensions strain Delta’s margins and balance sheet is something investors should be aware of...

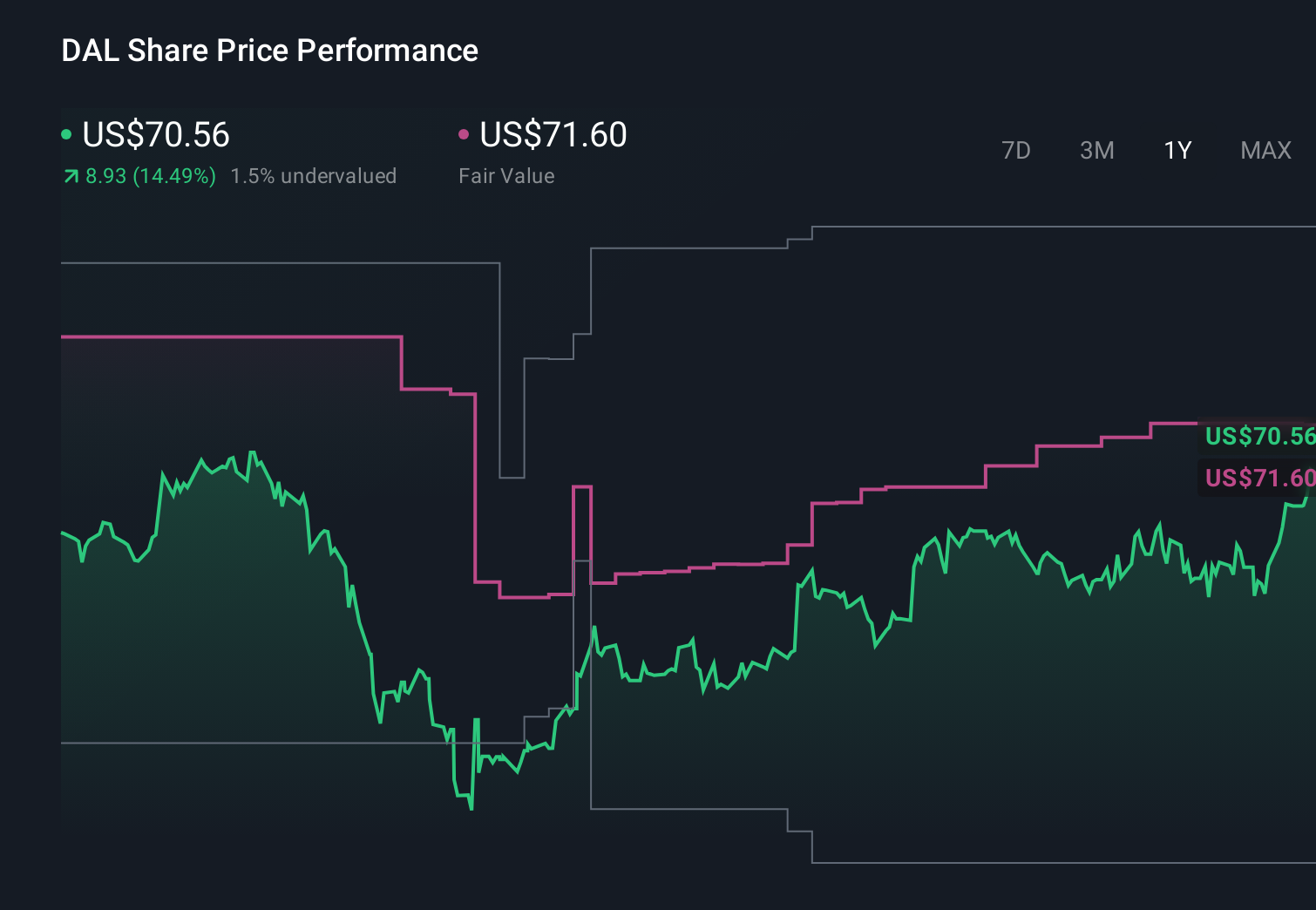

Delta Air Lines' narrative projects $68.4 billion revenue and $4.6 billion earnings by 2028. This requires 3.4% yearly revenue growth and about a $0.1 billion earnings increase from $4.5 billion today.

Uncover how Delta Air Lines' forecasts yield a $81.29 fair value, a 27% upside to its current price.

Exploring Other Perspectives

Before this conflict, the most optimistic analysts were assuming Delta could reach about US$70.6 billion in revenue and US$6.2 billion in earnings by 2028, which is far more upbeat than consensus and depends heavily on premium and international growth holding up despite risks like main cabin softness and geopolitical shocks that could now prompt those forecasts to be revisited.

Explore 10 other fair value estimates on Delta Air Lines - why the stock might be worth 18% less than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Delta Air Lines research is our analysis highlighting 4 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Delta Air Lines research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Delta Air Lines' overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- Explore 22 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.