Can DoorDash Sustain Its Momentum After an 88% Rally into 2025?

DoorDash, Inc. Class A DASH | 150.50 | +0.23% |

Thinking about what to do with DoorDash stock right now? You are definitely not alone. Whether you have been riding the wave for the past year or are just peeking at the ticker for the first time, there is no denying that DoorDash has been on the move. In the past year, the stock has nearly doubled, delivering a massive 88% total return. The past three months alone have seen a 21% jump, which is remarkable momentum for a company that is already a household name in food delivery.

The energy isn’t just on the charts. Growth appears to be present in every corner of DoorDash’s operations, with annual revenue up over 16% and net income growth even more impressive at 34%. Markets are clearly sizing up DoorDash with fresh eyes, in part due to better profitability and changes in how investors perceive risk in delivery and logistics.

However, this recent surge comes with some complexities. Even after the gains, DoorDash still trades at about a 19% discount to the average analyst price target and a significant 33% discount compared to its calculated intrinsic value. For those who focus on value, the company’s valuation score is currently 2 out of 6, meaning it is considered undervalued according to two of the main methods analysts use.

So, what exactly goes into that valuation score? Here is a look at the standard approaches analysts use to determine whether DoorDash is a bargain, along with a perspective on how to think about stocks like this more thoughtfully.

DoorDash delivered 88.4% returns over the last year. See how this stacks up to the rest of the Hospitality industry.Approach 1: DoorDash Cash Flows

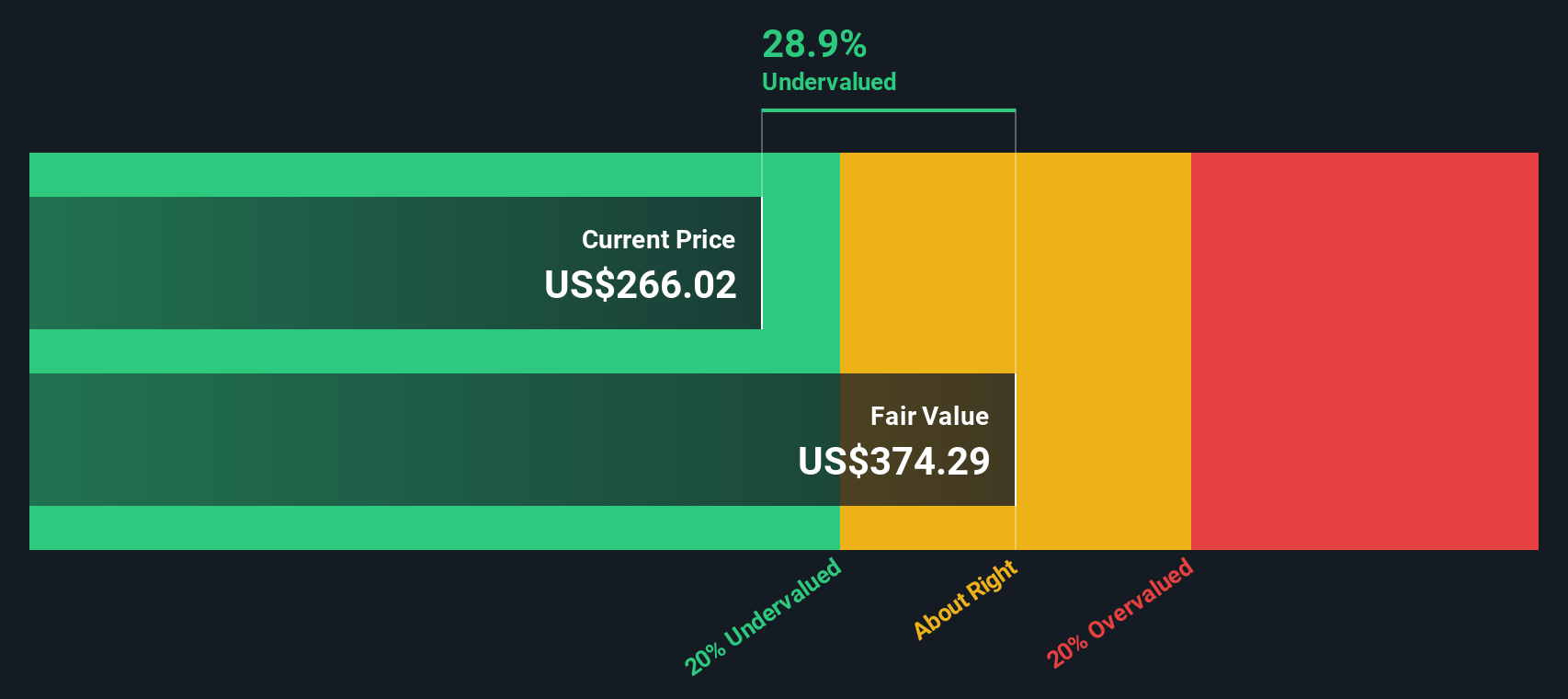

A Discounted Cash Flow (DCF) model estimates what a company is really worth by projecting its future cash flows and discounting them back to today’s dollars. This approach gives investors a sense of the business's intrinsic value.

DoorDash’s current Free Cash Flow stands at $1.72 billion, reflecting strong growth in recent years. Looking forward, analysts expect continued expansion, projecting Free Cash Flow to reach $7.46 billion by the end of 2029. Forecasts for the next decade suggest a robust trajectory in DoorDash’s ability to generate cash, with discounted 10-year projections consistently remaining above $5 billion.

According to this outlook, the DCF model values DoorDash stock at about $365 per share. Compared to the current share price, this calculation indicates that DoorDash is approximately 33.2% undervalued at present.

In summary, for those focused on future cash flow potential, DoorDash appears to offer significant upside based on intrinsic value.

Result: UNDERVALUED

Approach 2: DoorDash Price vs Earnings

For profitable companies like DoorDash, the Price-to-Earnings (PE) ratio is a widely trusted metric that gives investors an easy way to see how much they are paying for each dollar of earnings. It is especially useful here because DoorDash has moved into consistent profitability, making the PE ratio more meaningful than sales or book value alone.

A company's "normal" or "fair" PE ratio is shaped by expectations for its future growth, the stability of its earnings, and the risk of holding the stock. Higher growth and lower risk tend to support higher PE multiples, while lower growth or greater uncertainty can push the fair multiple down.

At the moment, DoorDash trades at approximately 133x earnings, which is well above both the hospitality industry average of 23.5x and the peer group average of 32.9x. However, Simply Wall St’s proprietary Fair Ratio for DoorDash is set at 50.6x, taking into account its rapid earnings growth, competitive position, and risk factors unique to the business.

Comparing DoorDash’s current PE multiple to the Fair Ratio, the stock appears significantly overvalued using this analysis. While the company's growth prospects are strong, the actual multiple investors are paying appears far out of sync with what would be considered fair for a company with DoorDash’s attributes today.

Result: OVERVALUED

Upgrade Your Decision Making: Choose your DoorDash Narrative

A Narrative is a story you create about a company’s future, connecting what you believe will happen next with concrete forecasts for things like revenue, earnings, and profit margins, and then translating that story into a fair value estimate for the stock.

Instead of relying solely on numbers and ratios, Narratives help you tie the bigger picture to the financial model and ultimately to your investment decisions. They are simple to build and use, especially within the Simply Wall St platform where millions of investors share, follow, and update Narratives every day.

By comparing the fair value from your Narrative to today’s price, you get clear guidance on whether it is time to buy, hold, or sell. Your Narrative also updates automatically as new news or earnings come in.

For instance, one DoorDash Narrative focuses on breakthrough automation and expanding international markets and expects a fair value of $360 per share. A more cautious outlook sees $190, highlighting how different stories can lead investors to very different conclusions.

Do you think there's more to the story for DoorDash? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.